Income Statement And Balance Sheet Approaches To Estimating Bad Debts

Https Egrove Olemiss Edu Cgi Viewcontent Cgi Article 1575 Context Hon Thesis

Account For Uncollectible Accounts Using The Balance Sheet And Income Statement Approaches Principles Of Accounting Volume 1 Financial Accounting

General Ledger Accounting Play General Ledger General Ledger Example Good Essay

Income Statements Explained Accountingcoach

7 4 Estimating The Amount Of Uncollectible Accounts Financial Accounting

Forecasting Income Statement Interest Expense Wall Street Prep

The first is an income statement approach that measures bad debt as a percentage of sales.

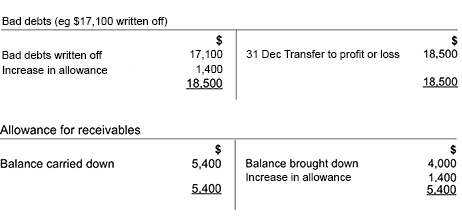

Income statement and balance sheet approaches to estimating bad debts. However the balance sheet would show 100 000 accounts receivable less a 5 300 allowance for doubtful accounts resulting in net receivables of 94 700. The direct write off method involves writing off a bad. It matches the revenue generated from credit sales with the expense incurred from them by recording a bad debt expense on the income statement. Estimating bad debts therefore serves two main purposes.

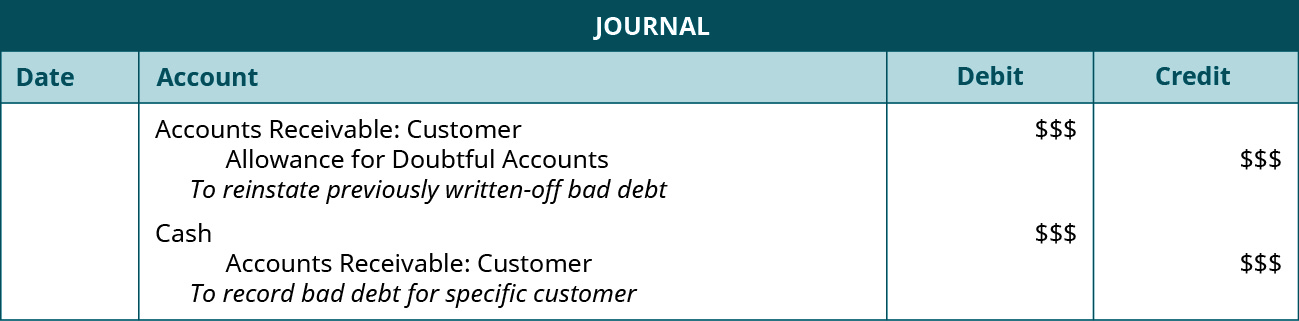

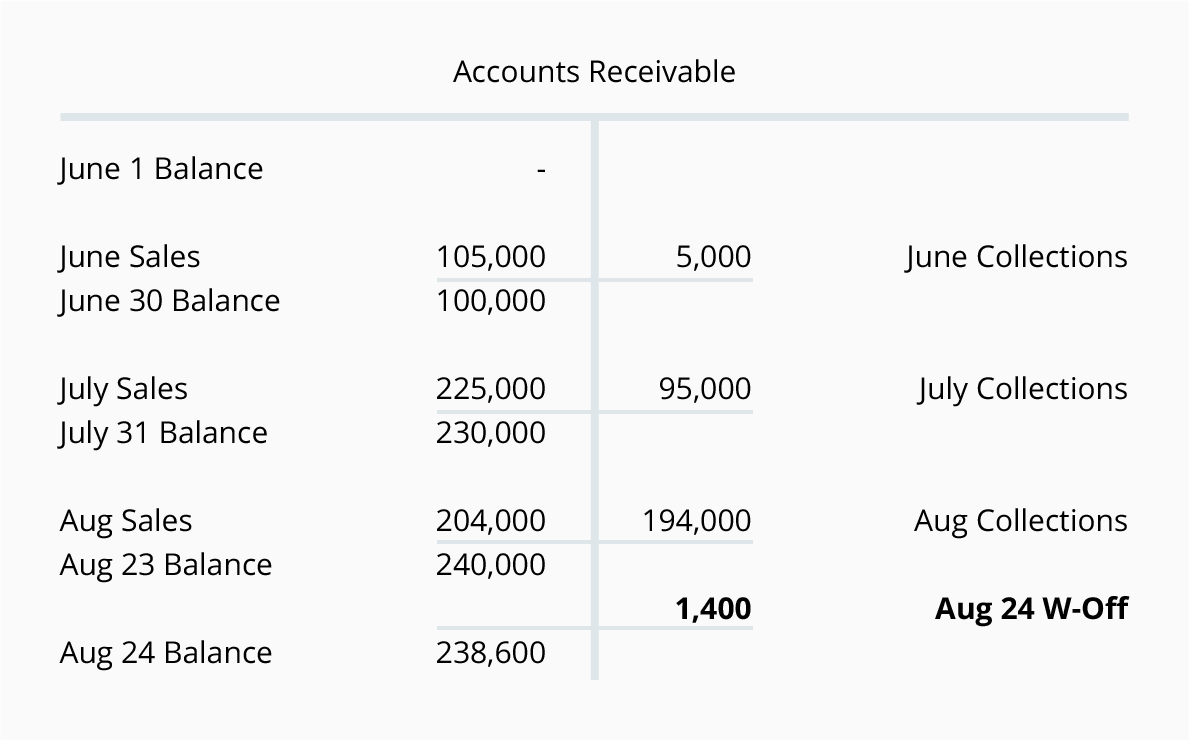

The estimate for bad debts reduces both net earnings on the income statement and the accounts receivable. Bad debt can be reported on the financial statements three financial statements the three financial statements are the income statement the balance sheet and the statement of cash flows. The adjusting entry would still be for 5 000. Record the year end adjusting entry for 2018 bad debt using the balance sheet method.

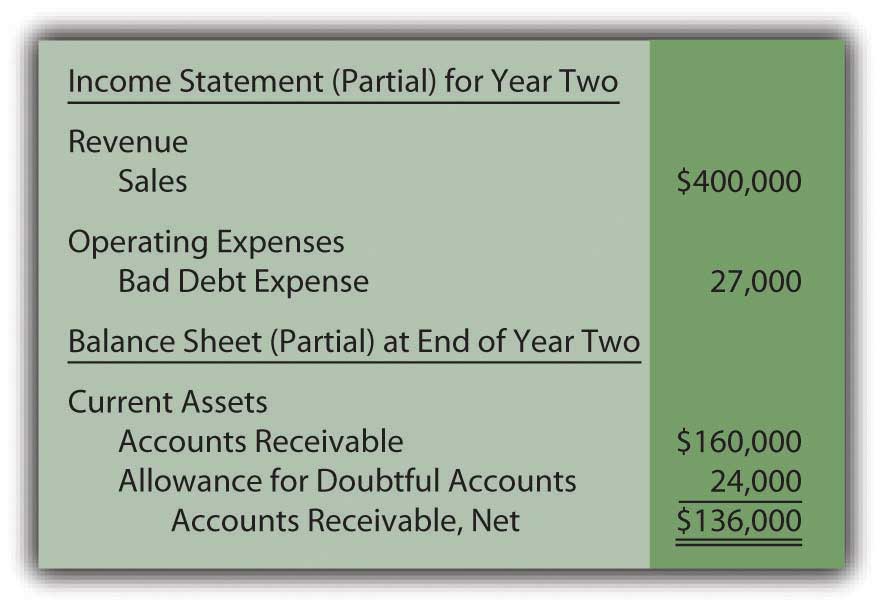

These three core statements are intricately using the direct write off method or the allowance method. There are two primary methods for estimating bad debt expense. On the income statement bad debt expense would still be 1 of total net sales or 5 000. Asset on the balance sheet.

Annual Profit Loss Free Office Form Template Document Sample Profit And Loss Statement Statement Template Income Statement

Chapter 8

Writing Off An Account Under The Allowance Method Accountingcoach

Pin By Jaimie Mcgrath On Career Stuff Journal Entries Accounting Journal

Ca Accounting Books Bad Debts And Doubtful Debts Bad Debt Accounting Books Debt

Join This Webinar To Understand The Balance Sheet Approach For Accounting For Income Taxe Loans For Bad Credit Debt Consolidation Programs Bookkeeping Services

Describe And Prepare Multi Step And Simple Income Statements For Merchandising Companies Principles Of Accounting Volume 1 Financial Accounting

Roce Formula Google Search Math Formula Net Profit

Adjustments To Financial Statements Students Acca Global Acca Global

The Common Size Analysis Of Financial Statements

Is A 10 Return Good Or Bad Investment Performance Revealed Investing Finance Investing Investing Strategy

Sales Revenue Definition Overview And Examples

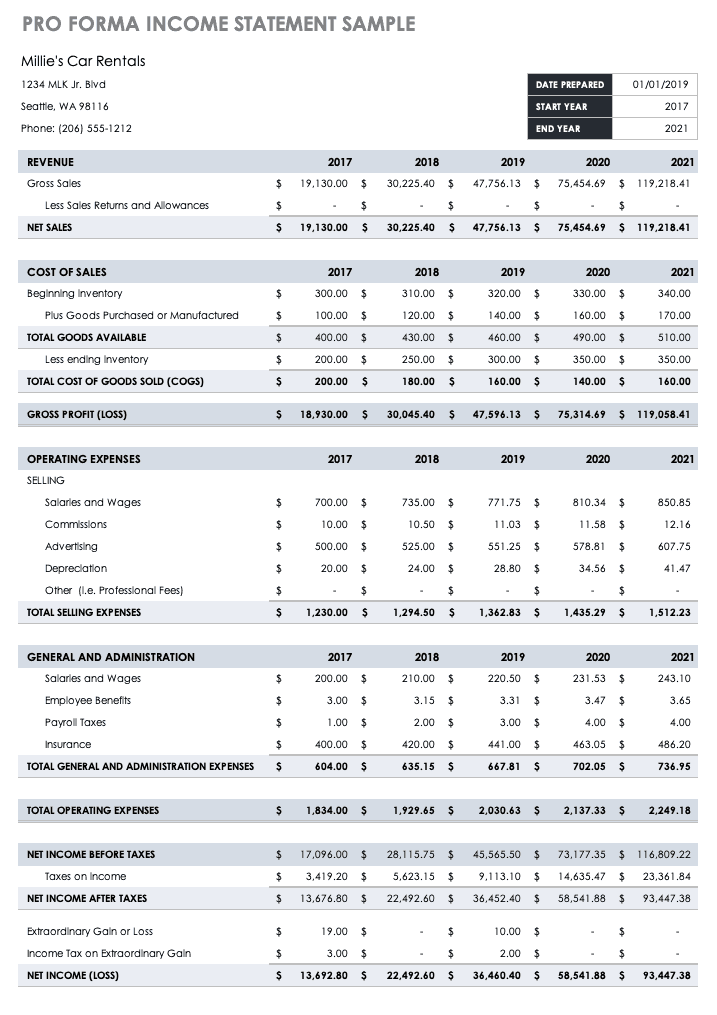

Pro Forma Financial Statements Smartsheet