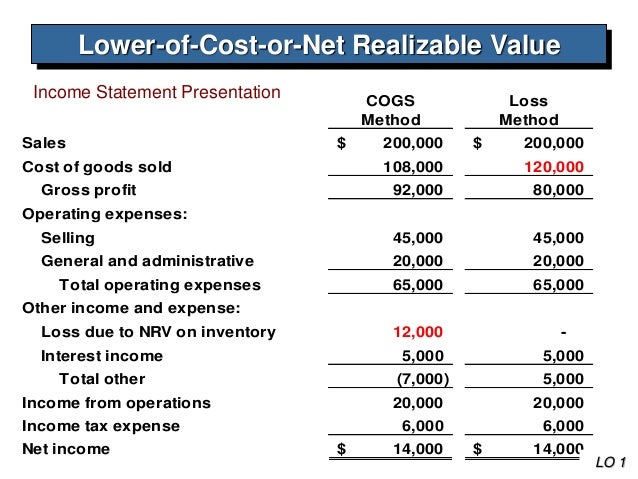

Income Statement Presentation Method

Statement Of Comprehensive Income Overview Components And Uses

Income Statement Definition Explanation And Examples

Income Statement Components Under Ias 1 Income Statement Personal Financial Statement Financial Statement

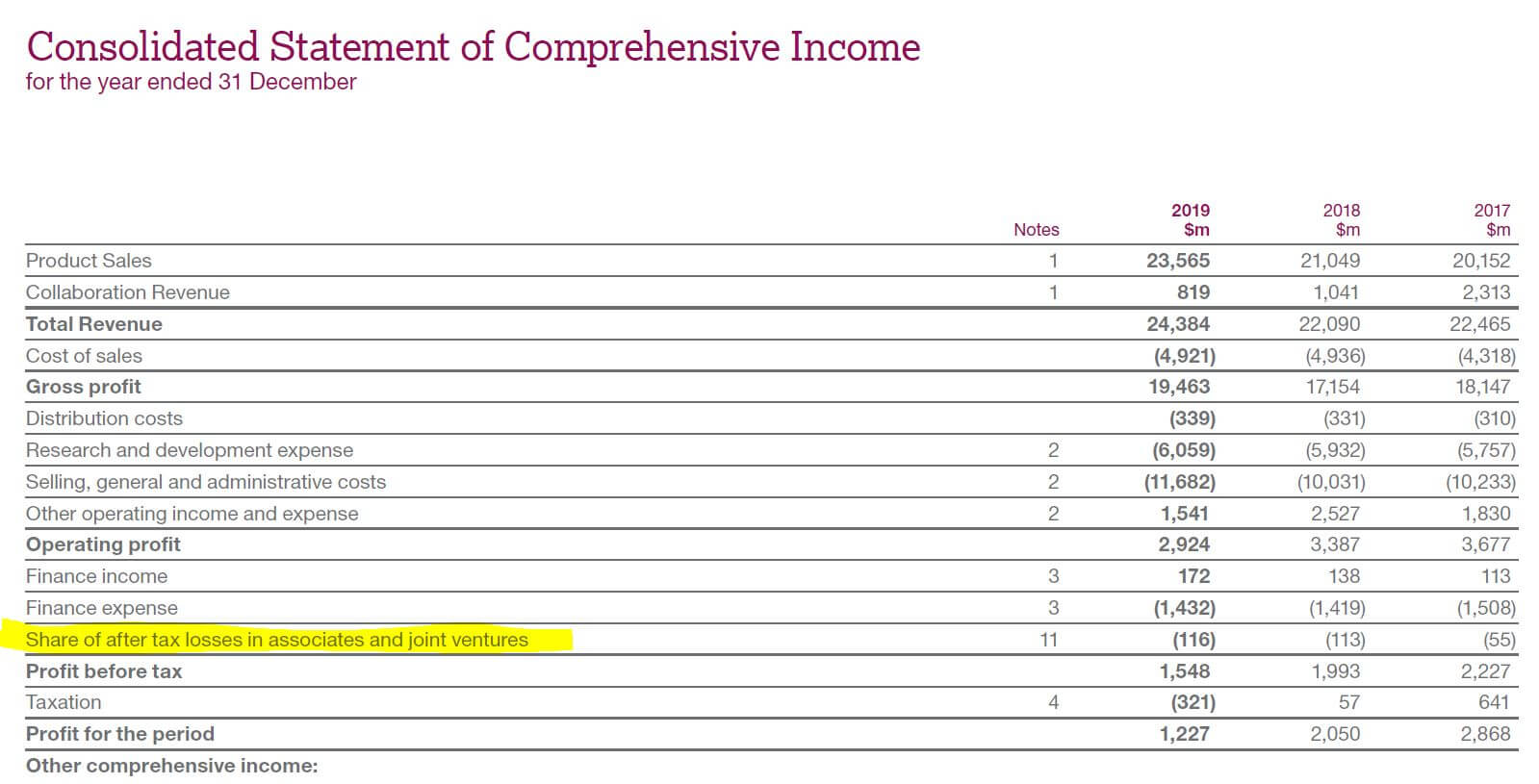

Equity Method Ifrscommunity Com

Chapter3

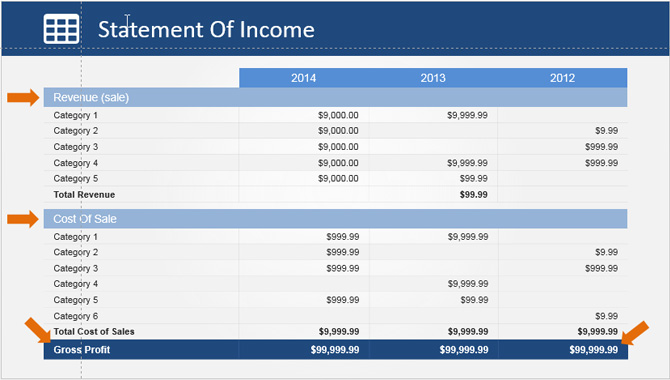

How To Create A Powerpoint Presentation Of Financial Statements Slidemodel

The multi step income statement format comprises a gross profit section where the cost of sales is deducted from sales followed by income and expenses to reach an income before tax.

Income statement presentation method. The format of the income statement or profit and loss account is. The profit or loss is determined by taking all revenues and subtracting all expenses from both operating and non operating activities this statement is one of three statements used in both corporate finance including financial modeling and accounting. The income statement is the first financial statement typically prepared during the accounting cycle because the net income or loss must be calculated and carried over to the statement of owner s equity before other financial statements can be prepared. There is no reallocation of these expenses to different functions of the entity i e.

Example 2 multi step income statement. Cost of goods sold selling costs administrative costs and other expenses. An income statement by function is the one in which expenses are disclosed according to their functions such are cost of goods sold selling expenses administrative expenses other expenses losses etc. An income statement by nature method is the one in which expenses are disclosed according to their nature such as depreciation transports costs rent expense wages and salaries etc.

The income statement is one of a company s core financial statements that shows their profit and loss over a period of time. Our financial reporting guide financial statement presentation details the financial statement presentation and disclosure requirements for common balance sheet and income statement accounts it also discusses the appropriate classification of transactions in the statement of cash flows and addresses the requirements related to the statements of stockholders equity and other comprehensive. Companies that use the direct method must provide a reconciliation of net income to net cash flow from operating activities in a separate schedule in the financial statements. The conventional method of presentation is t or account form or horizontal form.

This method allows us to calculate gross profit and operating profit within the income statement and therefore it is usually used in the multi step. In case of companies the companies act 1956 has given prescribed forms for the profit and loss account and balance sheet in part i schedule vi in horizontal forms only.

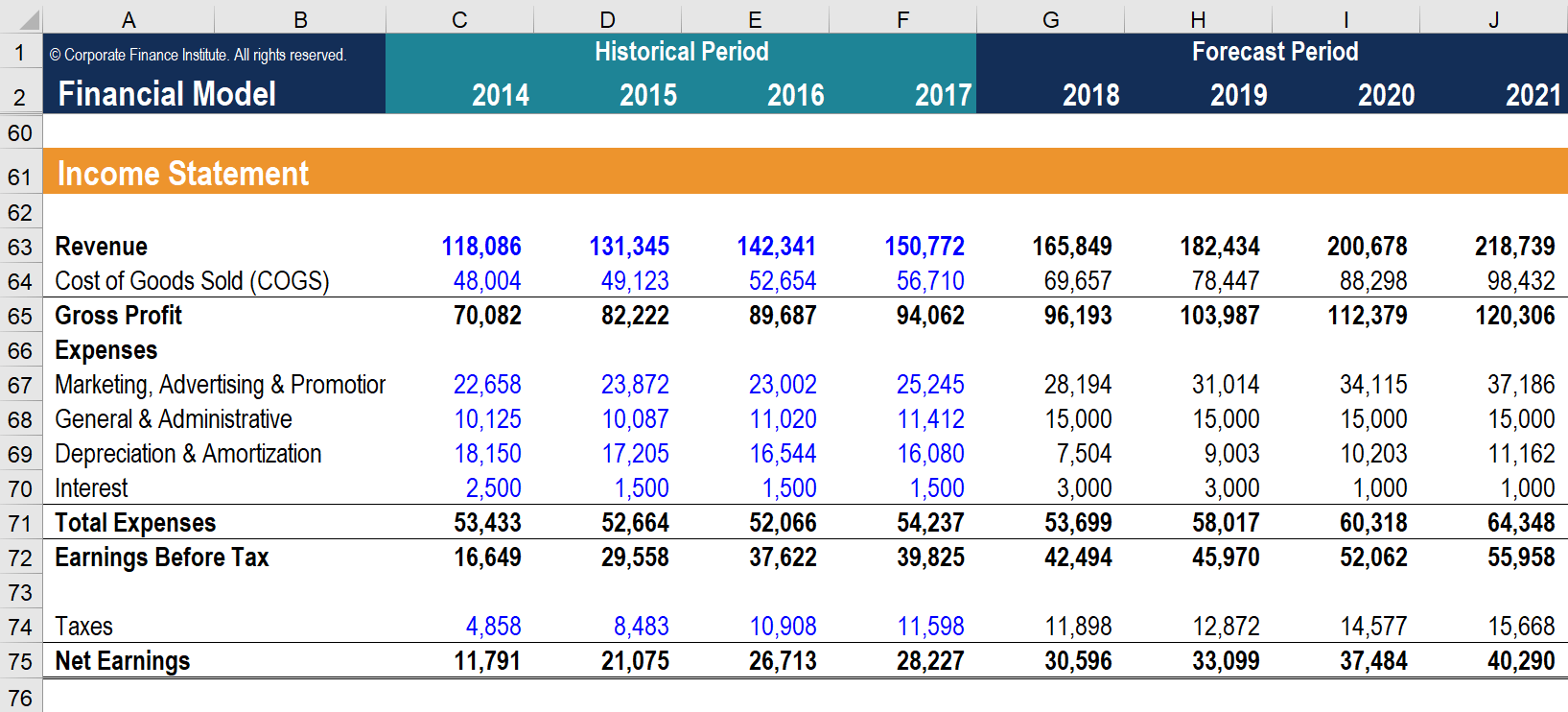

1 Income Statement

7 Best Charts For Income Statement Presentation Analysis Kamil Franek Business Analytics

Using The Indirect Method To Prepare The Statement Of Cash Flows

:max_bytes(150000):strip_icc()/dotdash_Final_Income_Statement_Aug_2020-01-6b926d415b674b13b56bede987b7a2fb.jpg)

Income Statement Definition

Practical Illustrations Of The New Leasing Standard For Lessees The Cpa Journal

Financial Analysis Powerpoint Templates Slides And Graphics

Shaking Up Financial Statement Presentation Financial Statement Cash Flow Statement Income Statement

Analysis Of Financial Statements 4 Methods Financial Management

Avoiding Missteps In The Lifo Conformity Rule

Income Statement Presentation Ifrs Compared To Us Gaap

How To Present An Income Or Profit And Loss Statement Think Outside The Slide

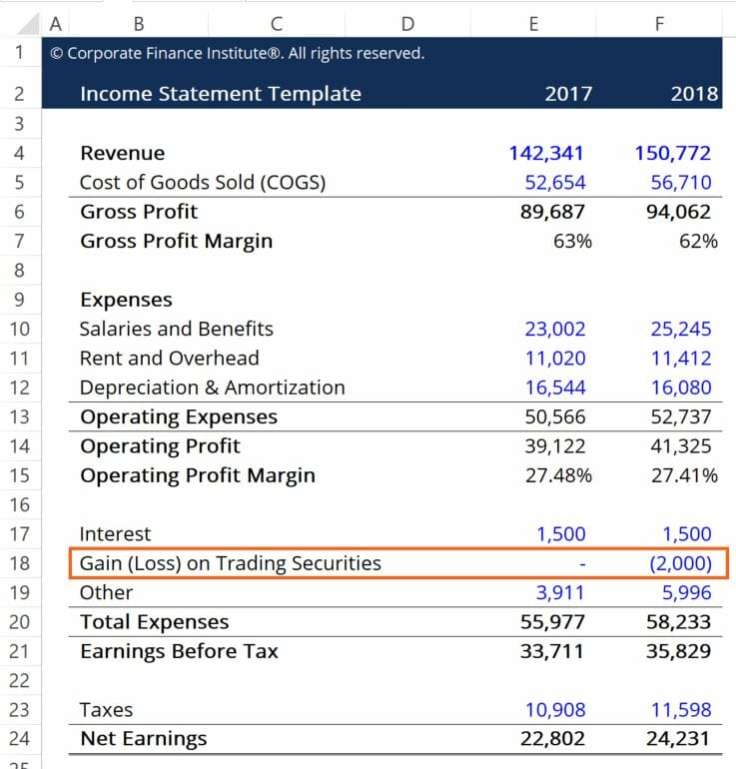

Trading Securities Learn About Accounting For Trading Securities

Standardizing Financial Statements Boundless Accounting