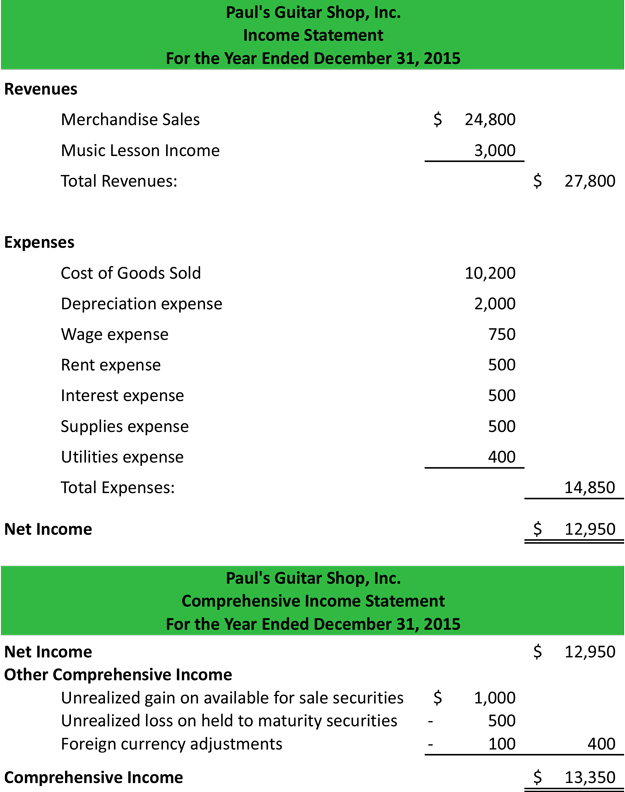

Partial Statement Of Comprehensive Income

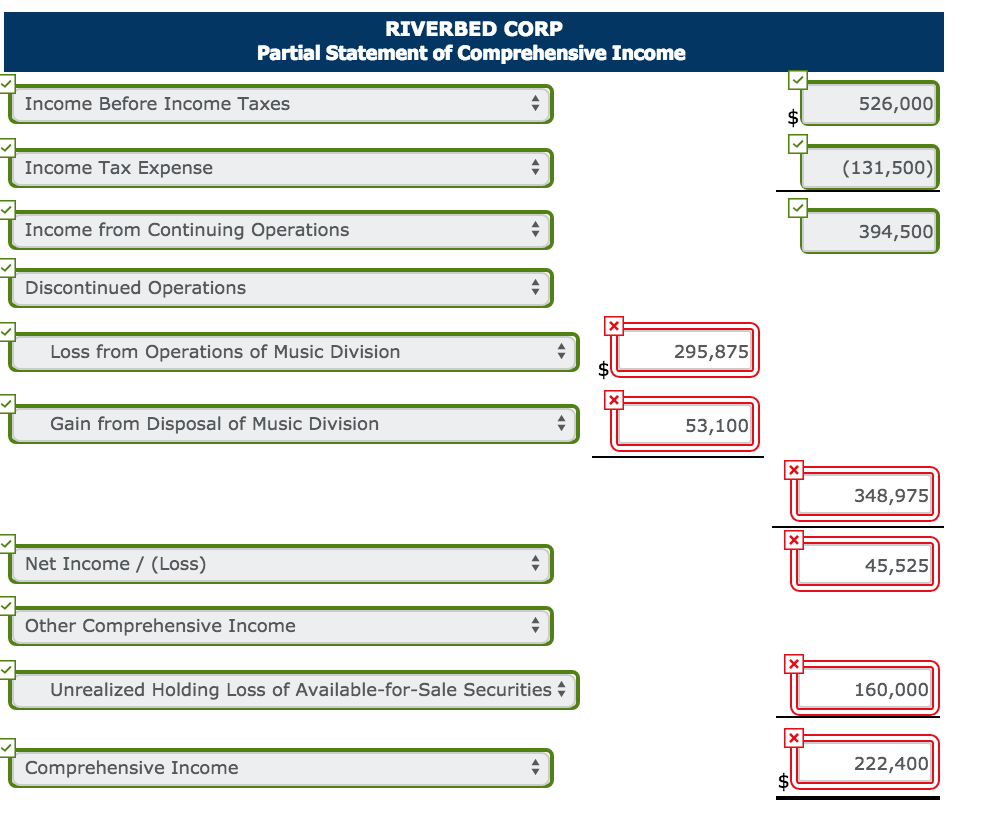

Solved In Its Proposed 2017 Income Statement Riverbed Co Chegg Com

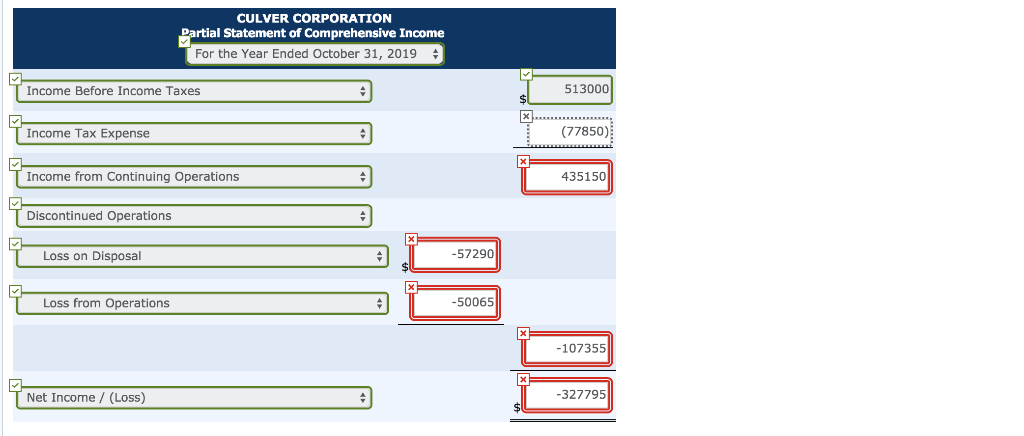

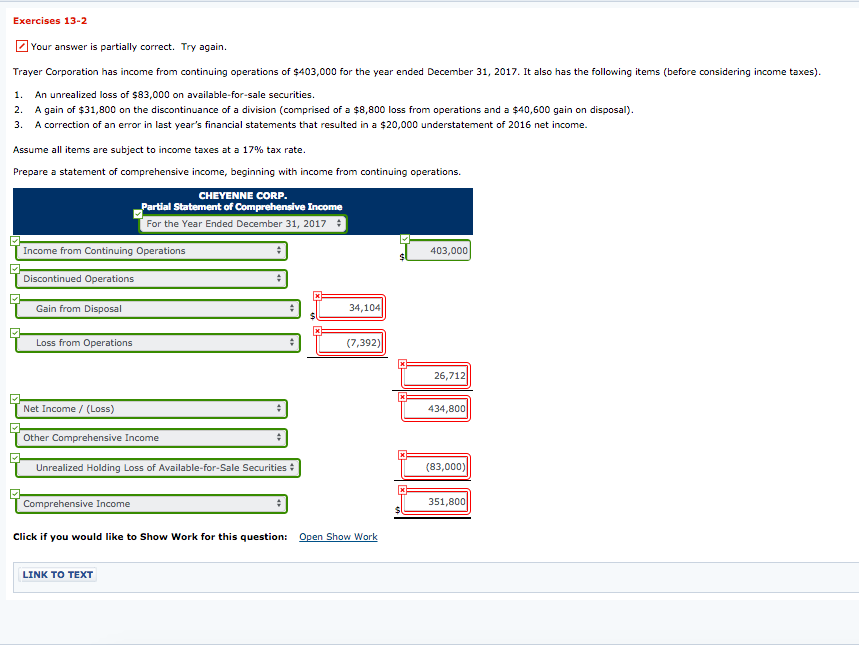

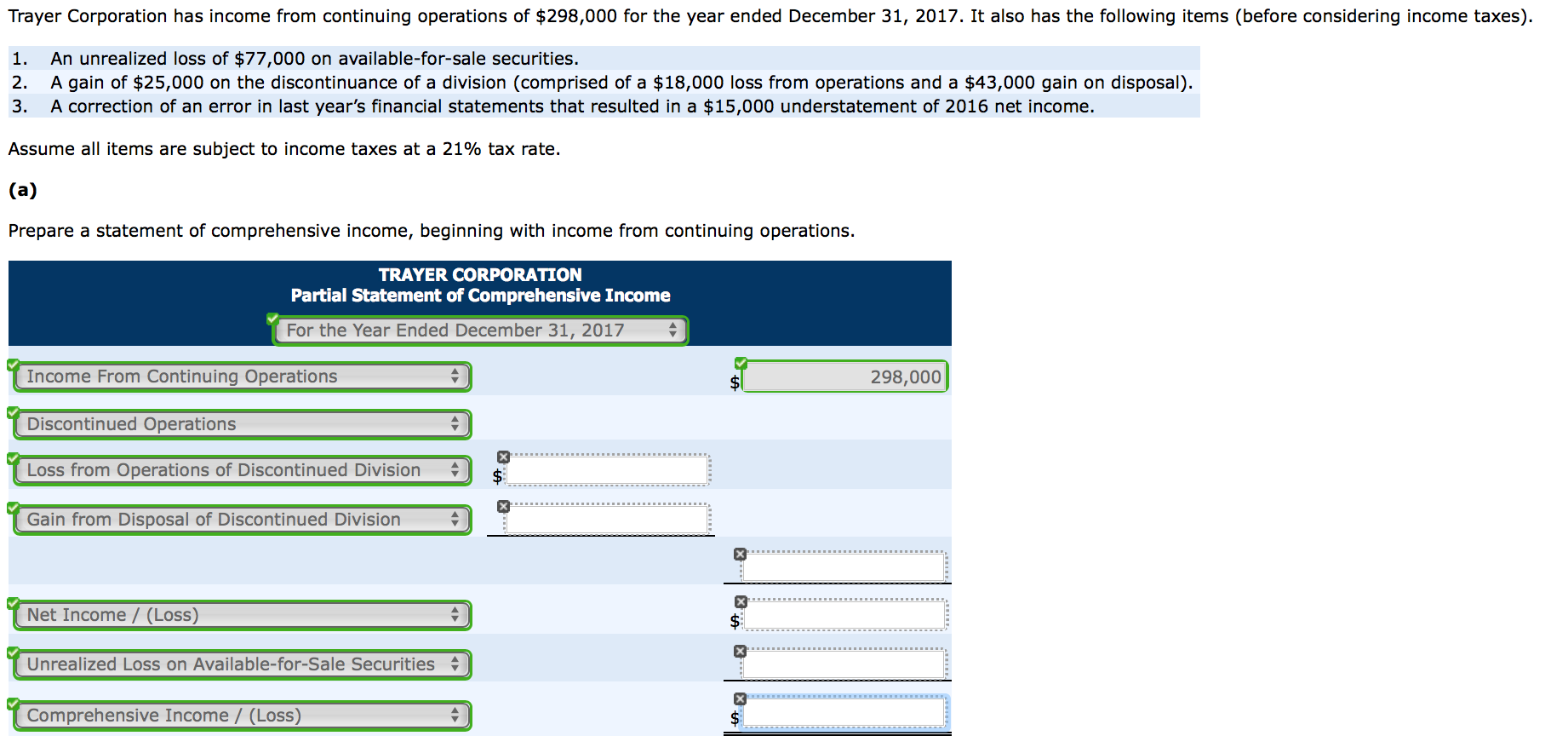

Solved Trayer Corporation Has Income From Continuing Oper Chegg Com

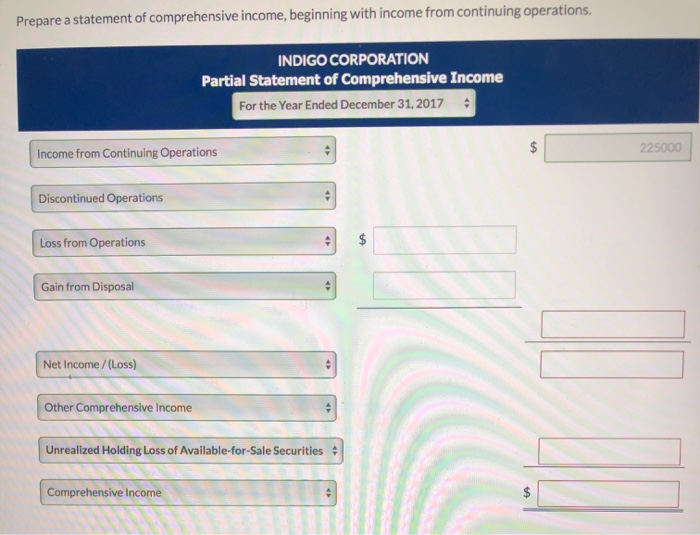

Solved Prepare A Statement Of Comprehensive Income Begin Chegg Com

Solved Exercise 13 1 Your Answer Is Partially Correct Tr Chegg Com

Solved Your Answer Is Partially Correct Try Again Traye Chegg Com

Preparing Partial Income Statement With Discontinued Operations Chance Co Youtube

But don t depend solely on it.

Partial statement of comprehensive income. Normally we prepare an income statement for a single month or for a year. However a partial income. A statement of comprehensive income that begins with profit or loss bottom line of the income statement and displays the items of other comprehensive income for the reporting period ias 1 p 81 so the statement of comprehensive income aggregates income statement profit and loss statement and other comprehensive income which isn t. Revenue 7600000 cost of goods sold 3700000 operating expenses 2100000 interest expense 1100000 income tax expense 700000 other comprehensive income fair value loss on fvtoci investments 30000 what is the times interest earned.

Although the income statement is a go to document for assessing the financial health of a company it falls short in a few aspects. Limitations of a statement of comprehensive income. The income statement encompasses both the current revenues resulting from sales and the accounts receivables which the firm is yet to be paid. A statement of comprehensive income is the overall income statement that consolidates standard income statement which gives details about the repetitive operations of the company and other comprehensive income which gives details about the non operational transactions such as the sale of assets patents etc.

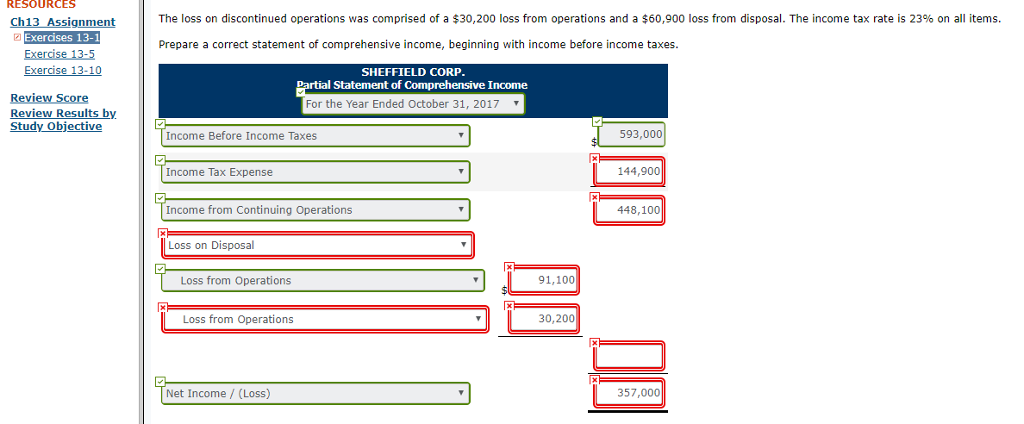

The partial statement of comprehensive income for an entity is as follows. Partial statement of comprehensive income for the year ended december 31 2014 income from continuing operations 12 600 000 discontinued operations loss from operation of discontinued restaurant division net of tax 315 000 loss from disposal of restaurant division net of tax 89 000 404 000 net income 12 196 000 other comprehensive income items that may be reclassified subsequently to net.

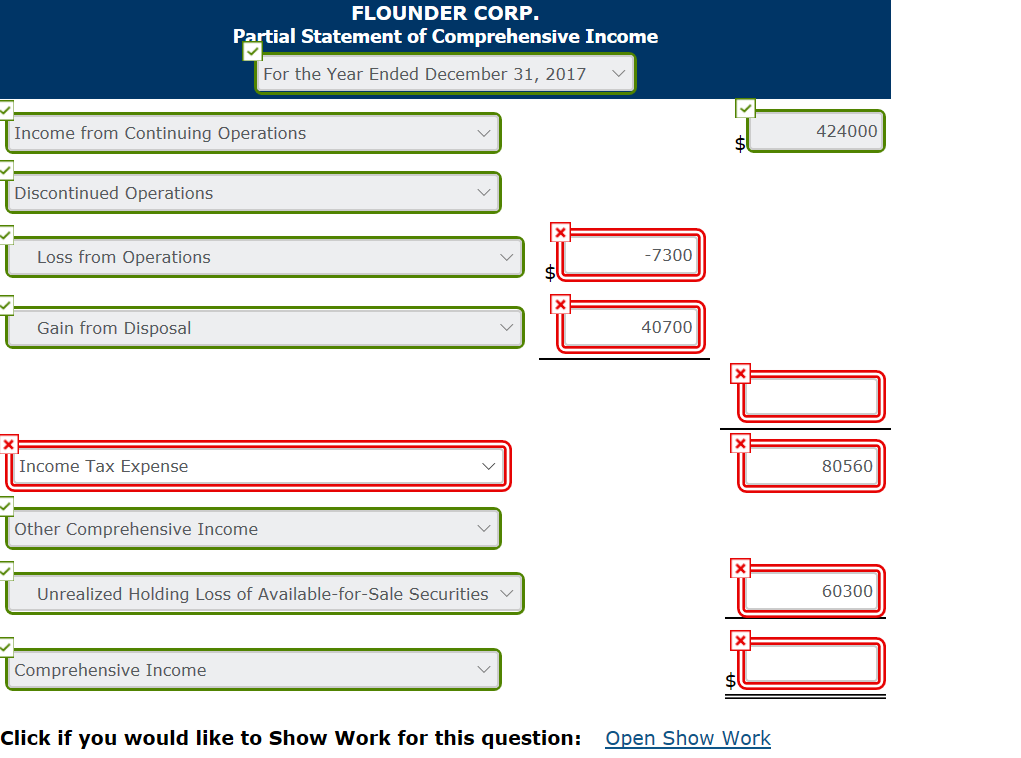

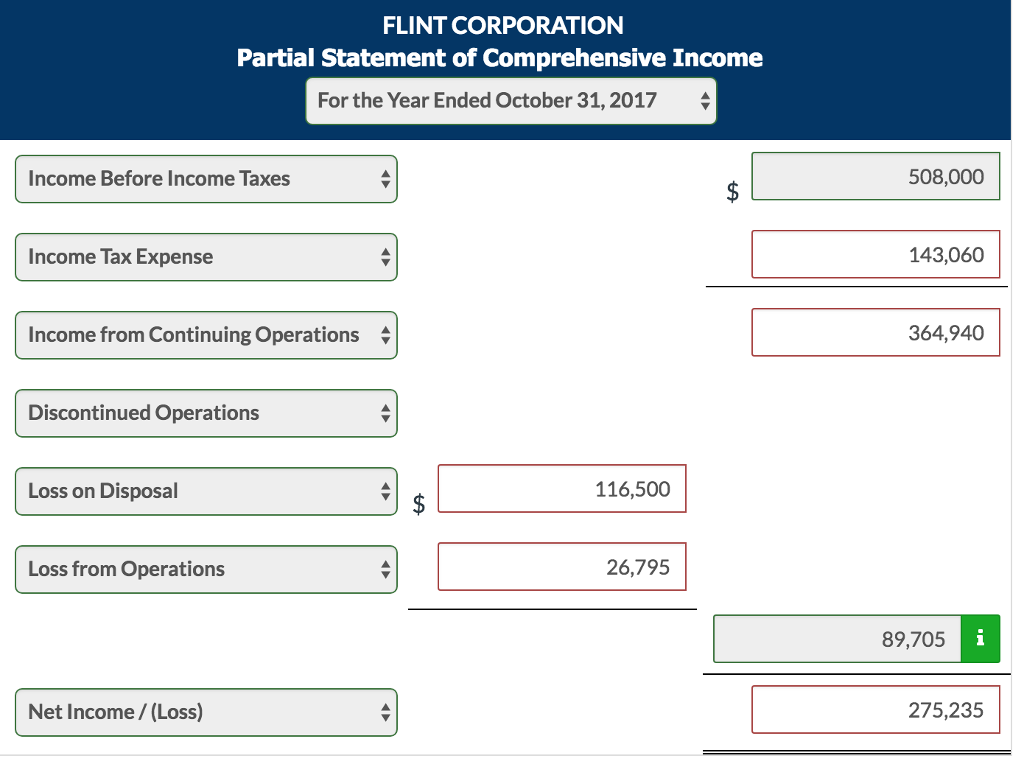

Solved For Its Fiscal Year Ending October 31 2017 Flint Chegg Com

Solved Exercise 13 1 For Its Fiscal Year Ending October 3 Chegg Com

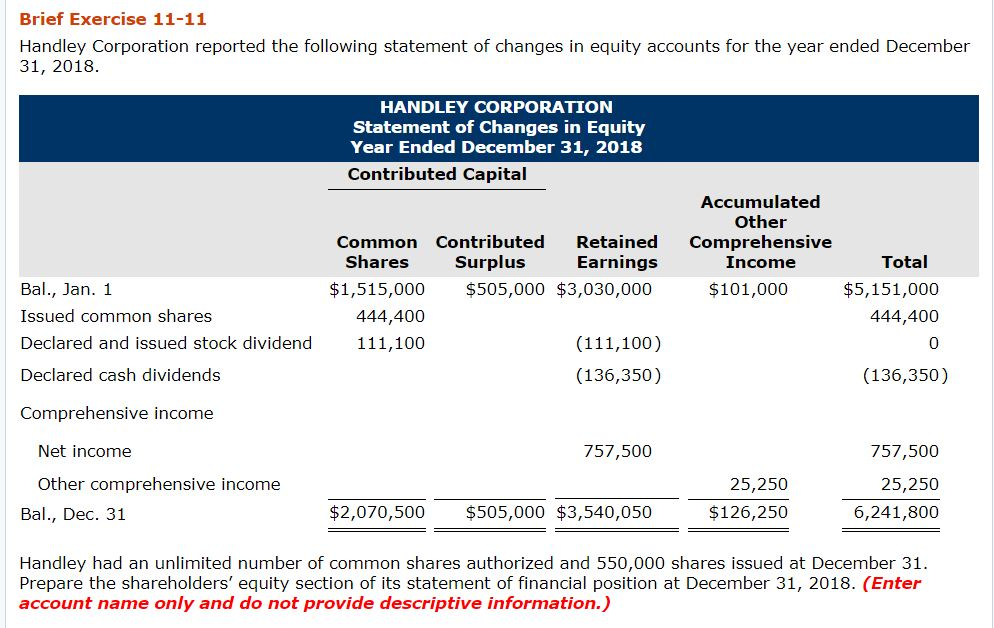

Solved Complete The Statement Of Financial Position Part Chegg Com

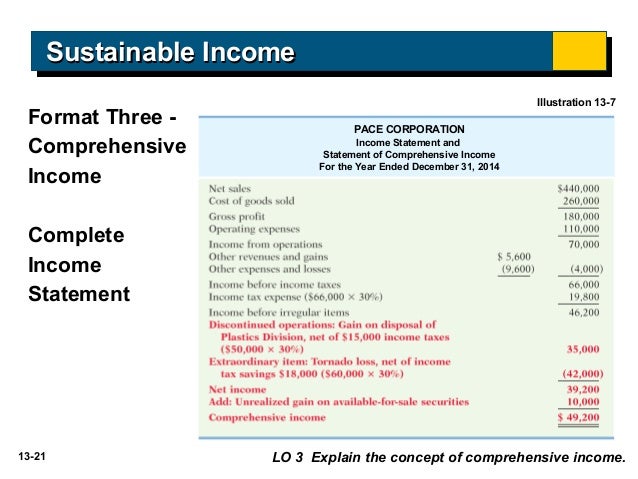

Acc102 Chap13 Publisher Power Point

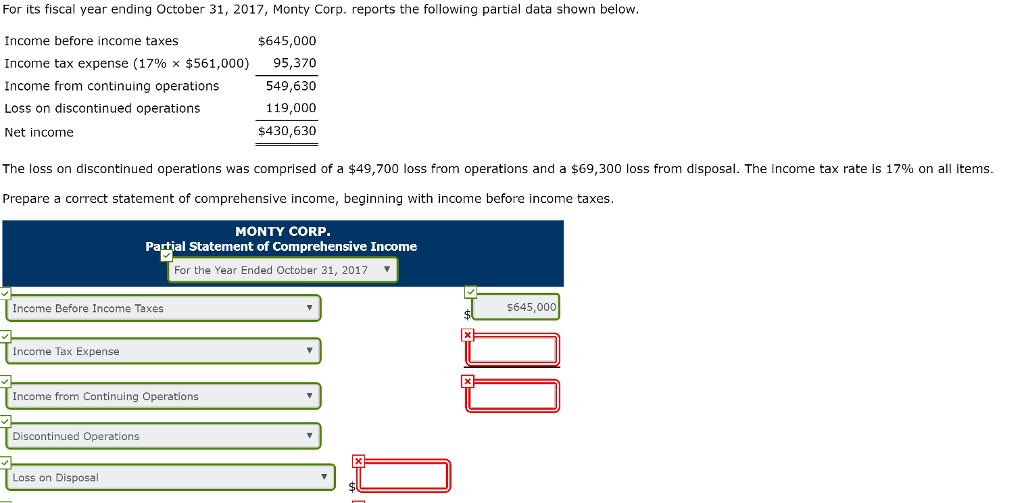

Solved For Its Fiscal Year Ending October 31 2017 Monty Chegg Com

Solved Trayer Corporation Has Income From Continuing Oper Chegg Com

Discontinued Operations Partial Income Statement Youtube

Examining The Income Statement Ppt Video Online Download

Other Comprehensive Income Statement Example Explanation

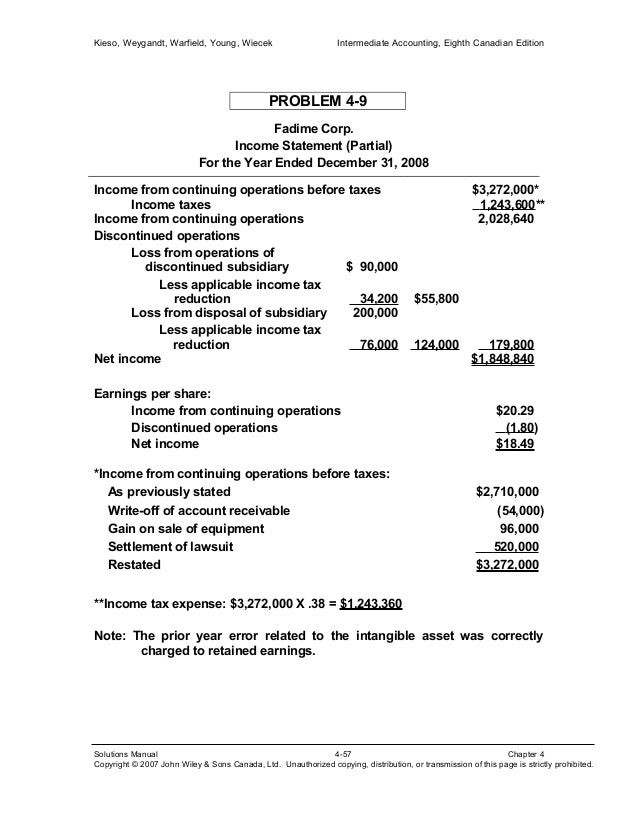

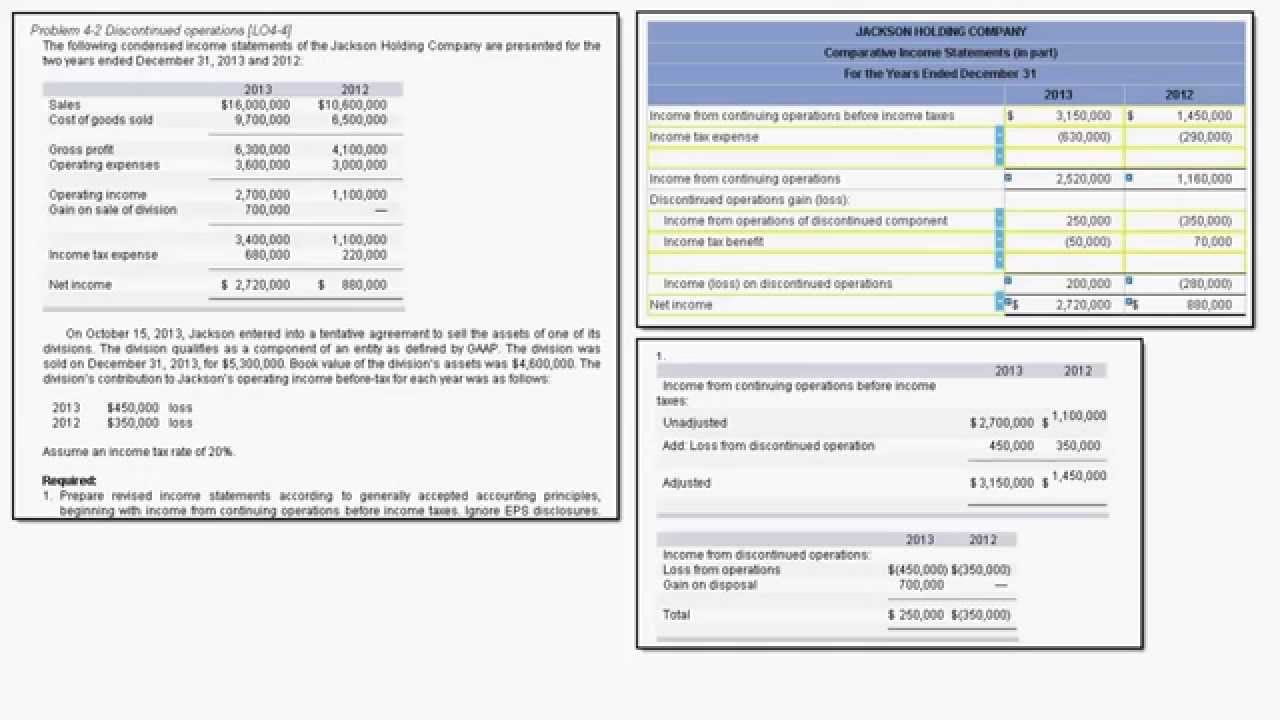

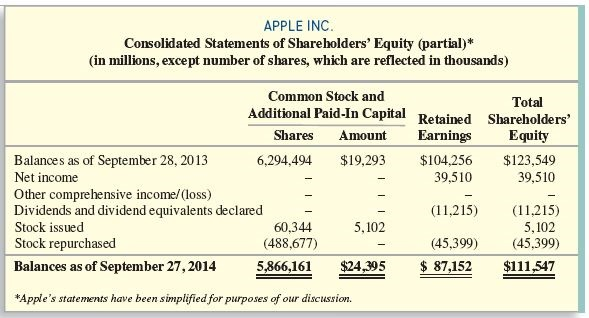

Ch04 Soln

Solved This Picture Represents Format Needed This Table Chegg Com

14 Financial Statement Analysis Learning Objectives Ppt Download

Chapter 4 Brief Exercise 4 5 A Income From Continuing Operations Income From Operations Gain On Sale Of Fv Ni Investments Income Tax On Income From Course Hero