Presentation Of Interest Expense In Income Statement

Income Statement Components Under Ias 1 Income Statement Personal Financial Statement Financial Statement

A Sample Income Statement Modified For Budget Variance Analysis Income Statement Financial Analysis Financial Statement

Income Statement Templates 29 Free Docs Xlsx Pdf Income Statement Personal Financial Statement Statement Template

Example Income Statement Income Statement Profit And Loss Statement Statement Template

Financial Statement Editable Powerpoint Template Financial Statement Financial Statement Analysis Statement Template

How To Calculate Ebitda Finance Lessons Cost Of Goods Sold Finance

Income statement for the year ended december 31 2011 000s sales 11 892 cost of goods sold 9 905 gross profit 1 987 research development 225 selling expense 520 general administrative expense 490 total operating expense 1 235 operating profit 752 interest income 114 interest expense 10 other income 25 pretax income 881 income taxes 352.

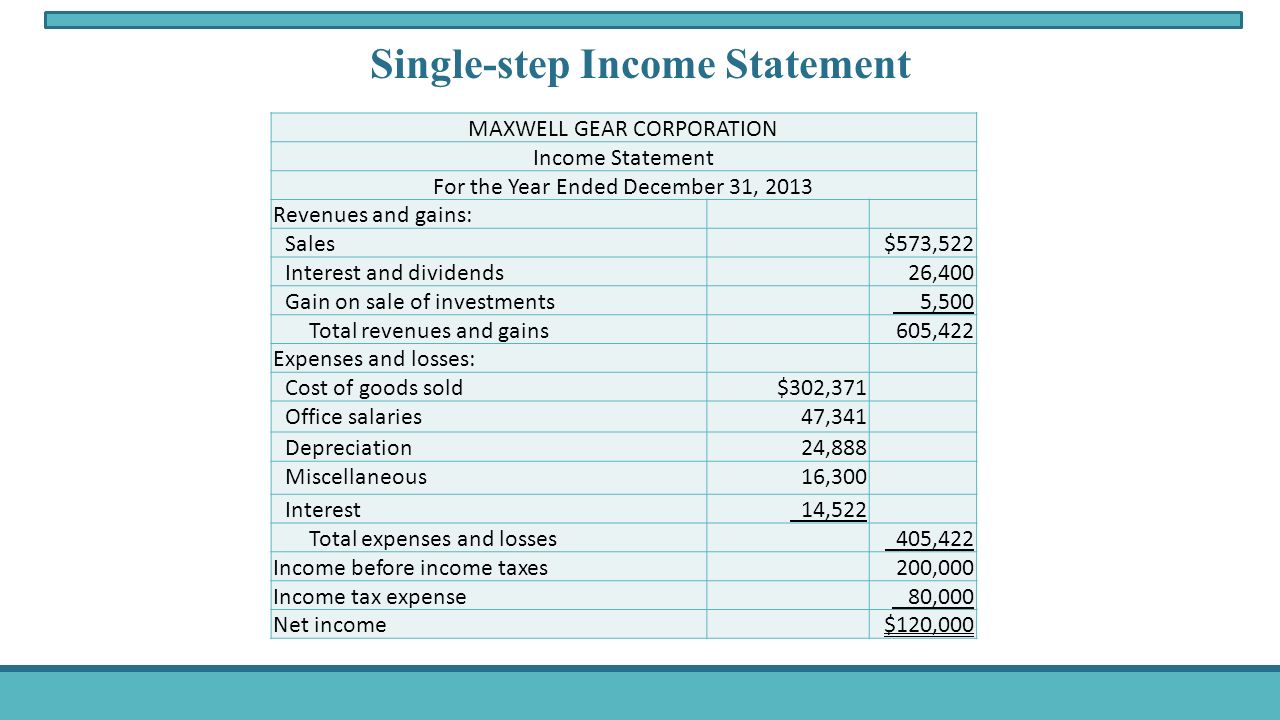

Presentation of interest expense in income statement. As a result of this analysis the staff recommended the following presentation in the statement of comprehensive income. Cost of goods sold 7 600. The expense paid on the loans and bonds is an expense out through the income statement. Net refers to the fact that management has simply subtracted interest income from interest expense to come up with one figure.

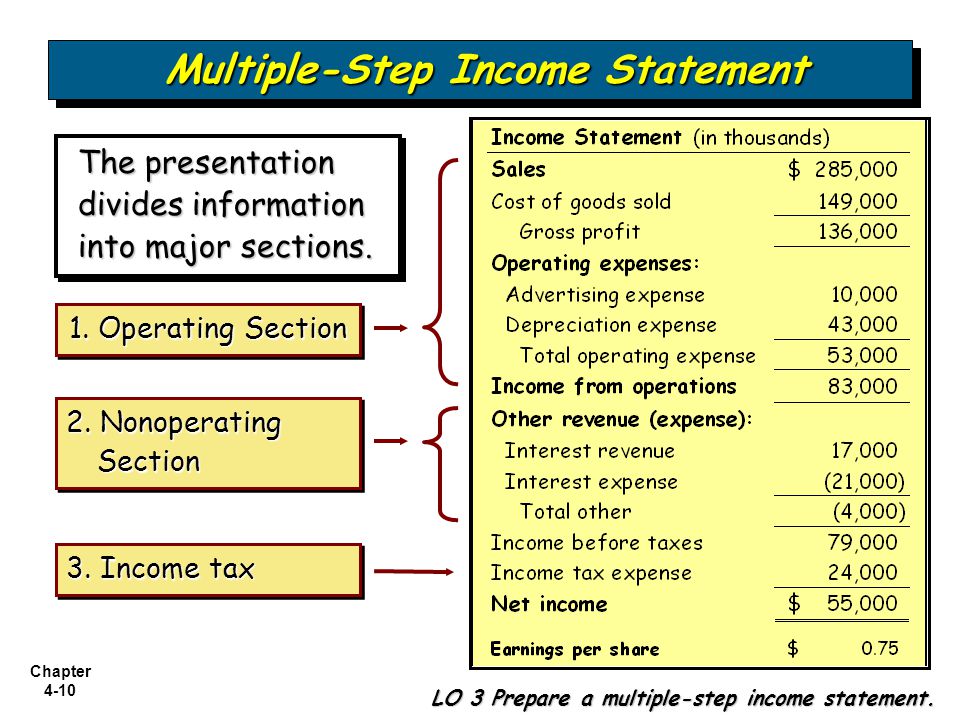

The standard requires a complete set of financial statements to comprise a statement of financial position a statement of profit or loss and other comprehensive income a statement of changes in equity and a statement of cash flows. Ias 1 was reissued in september 2007 and applies to annual periods beginning on or after 1 january 2009. Interest expense represents an amount of interest payable on any borrowings which includes loans bonds or other lines of credit and its associated costs are shown on the income statement. Interest expense 1 150.

The following income statement items appeared on the adjusted trial balance of schembri manufacturing corporation for the year ended december 31 2013 in 000s. General and administrative expenses 940. Interest expense is one of the core expenses found in the income statement income statement the income statement is one of a company s core financial statements that shows their profit and loss over a period of time. This applies accordingly to interest resulting from a negative interest rate on a financial liability which must not be presented as a negative part of interest expense i e a reduction.

Presented on the face of the income statement when such presentation is relevant to an understanding of the company s financial performance. The profit or loss is determined by taking all revenues and subtracting all expenses from both operating and non operating activities this statement is one of. These expenses highlight interest accrued during the period and not the interest amount paid over the time period. Interest expense 126 060 income before income tax 231 423 income tax 66 934 net income for the year 164 489 attributable to.

Under the indirect method we take the profit or loss before tax and interest paid and then we subtract the amount of interest paid during the year.

Financial Statements Financial Statement Financial Statement

Profit And Expense Spreadsheet Di 2020

Income Statement Template 7 Income Statement Statement Template Financial Statement

When An Accountant Records A Sale Or Expense Entry Using Double Entry Accounting He Or She Sees The Inte Income Statement Accounting Jobs Accounting Education

The Income Statement And Comprehensive Income Intermediate Accounting I Chapter 4 This Presentation Is Under Development Ppt Download

Creating Effective Financial Powerpoint Presentations 24point0 Editable Powerpoint Slides Templates Powerpoint Presentation Powerpoint Financial

Income Statement Expense And Losses Accountingcoach Income Statement Statement Template Profit And Loss Statement

Depreciation Turns Capital Expenditures Into Expenses Over Time Income Statement Income Financial Statement

Pin On Template

Image Result For Financial Reports Templates Statement Template Financial Statement Report Template

Profit And Loss Statement For Private Practice Profit And Loss Statement Business Tax Deductions Bookkeeping Business

Income Statement Income Statement Excel Tutorials Financial Information

Income Statement Template 40 Templates To Track Your Company Revenues And Expenses Template Sumo Income Statement Statement Template Income