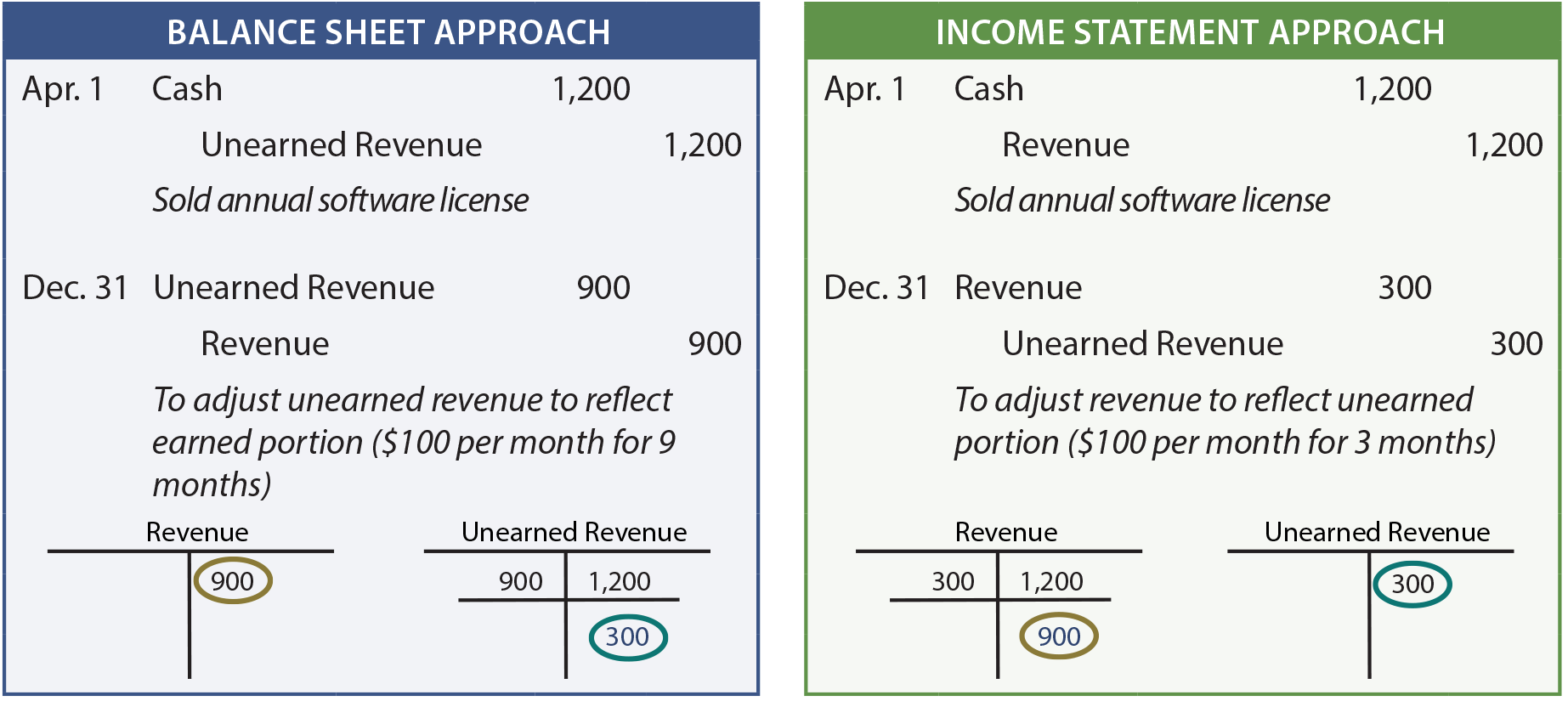

The Income Statement Approach To Calculating

Genevieve Wood I Picked This Diagram Because Of The Side By Side View Of The Contribution Margin And T Contribution Margin Income Statement Cost Of Goods Sold

Income Measurement Balance Sheet Income Income Statement

Ca Accounting Books Approaches For Calculating Prepayments Accounting Books Accounting Approach

Statement Of Comprehensive Income Overview Components And Uses

:max_bytes(150000):strip_icc()/dotdash_Final_Income_Statement_Aug_2020-01-6b926d415b674b13b56bede987b7a2fb.jpg)

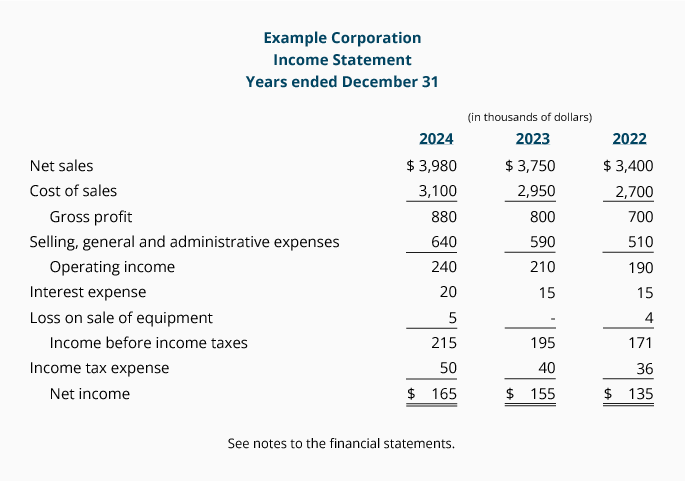

Income Statement Definition

Multiple Step Income Statement Accountingcoach

The alternative method for calculating gdp is.

The income statement approach to calculating. Gdp value added at basic prices taxes less subsidies on products. The income statement is one of a company s core financial statements that shows their profit and loss over a period of time. Assessing the economic contribution of the voluntary sector to gross domestic product can be considered methodologically as an under researched area in the uk since the majority of research work lacks detailed methodology. It s calculated by dividing the net operating income by the capitalization.

The income statement is one of three statements. The first is an income statement approach that measures bad debt as a percentage of sales. The income approach and the expenditure approach see also gross domestic product. This is a simple equation that shows the profitability of a company.

The income approach states that all economic expenditures should equal the total income generated by the production of all economic goods and services. There are two primary methods for estimating bad debt expense. This video shows the income statement approach to calculating breakeven points. The profit or loss is determined by taking all revenues and subtracting all expenses from both operating and non operating activities.

If revenue is higher than expenses the company is profitable. There are two primary methods to calculate gdp. If given the option use one of the following shortcut methods instead. According to the income approach gdp can be computed by finding total national income tni and then adjusting it for sales taxes t depreciation d and net foreign factor income f.

The income approach is a real estate valuation method that uses the income the property generates to estimate fair value. The income statement is used to calculate the net income of a business. With the production approach value added is measured as the. The second is a balance sheet approach that measures uncollectibles as a percentage of ending accounts receivable.

How To Calculate Retained Earnings On A Balance Sheet Business Finance Financial Statement Finance

The Adjusting Process And Related Entries Principlesofaccounting Com

General Ledger Accounting Play General Ledger General Ledger Example Good Essay

Hotel Revenue Projection Excel Template Plan Projections Hotel Revenue Management Revenue Management Hotel

Statement Of Retained Earnings Definitions Use Example Explained Earnings Statement Investing

Cash Flow Spreadsheet Template Cash Budget Template Cash Budget Template Will Be Related To Maintaining Three Imp Cash Flow Statement Cash Budget Cash Flow

Restaurant Chain Valuation Model Template Efinancialmodels Cash Flow Statement Cash Flow Budget Forecasting

Intermediate Accounting Kieso Weygandt Warfield Ppt Download

Single Step Vs Multi Step Income Statement Key Differences For Small Business Accounting

Download Cash Flow Forecast 12 Months Cash Flow Statement Cash Flow Spreadsheet Template

Forecasting Income Statement Interest Expense Wall Street Prep

Profit And Loss Statement Template Free Profit And Loss Statement Income Statement Statement Template

Income Statement Template Income Statement Statement Template Personal Financial Statement