Withholding Income Tax Brazil

General Information On The Brazilian Tax System Bpc Partners

Information On Withholding Income Tax Declarations Dirf

Save Thousands Of Dollars In Taxes With A Student Visa Go Study Australia

Employee Of The Quarter Certificate Awesome Tax Residency Certificate Format Netherlands A In 2020 Certificate Layout Microsoft Word Resume Template Certificate Format

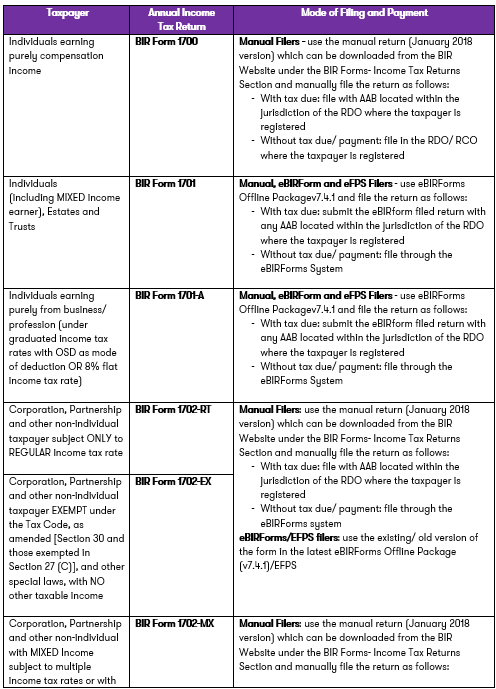

Manner Of Filing And Payment Of Annual Income Tax Return For Taxable Year 2018 As Of April 4 2019 Grant Thornton

Brazilian Federal Government Has Announced Comprehensive Tax Reform To Be Implemented In 2020

It applies to labor income capital income remittances abroad money prizes advertising services provided by legal entities and remuneration for services provided by legal entities.

Withholding income tax brazil. A corporation is resident in brazil if it is incorporated in brazil. Withholding tax unless the rate is reduced under a tax treaty. In the case of income tax it is generally calculated monthly and payments should generally be collected and paid. Corporate income tax irpj is levied on the taxable profits of an entity at a rate of 15.

There are several tax brackets for individuals. Brazil provides double taxation relief through a foreign tax credit system applicable to income tax paid to countries with which brazil has entered into a tax treaty or on a reciprocity basis when the source country also grants a foreign tax credit for taxes paid in brazil on brazilian source income. Brazilian resident companies are taxed on worldwide income. The standard tax rates for business are 1 and 1 5.

Withholding income tax wht at a 15 rate or 25 rate if the beneficiary is located in a tax haven or a country with a privileged tax regime. Offshore income is tax exempt. Irrf short for imposto sobre a renda retido na fonte in portuguese is the brazilian withheld income tax. The withholding tax is a modality of the federal tax over taxable income.

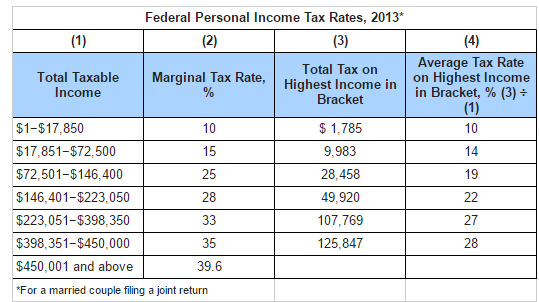

The 25 percent withholding income tax payment is to be effected by the local payer of the income through a voucher darf with the code 0473 income tax on non resident s income. Taxpayers in this condition are considered exempt and are not required to complete and file a brazilian annual tax return. Non resident companies are generally taxed in brazil through a registered subsidiary branch or pe based on income generated locally. Income tax employee discount for the individuals who have a local labor contract in brazil the company is responsible for the calculation and payment of the related income tax withholding which is due on a monthly basis and based on a progressive tax table rates vary from 0 to 27 5 as shown below.

Profits dividends distributed to resident or non resident beneficiaries individuals and or legal entities are generally not subject to irrf brazilian term for withholding income tax please see the income determination section for more information this provision is also applicable to dividends paid to non resident companies located in a tax haven jurisdiction. However as noted below taking. Please note that there are a number of other declarations returns imposed by the rfb for different taxes at federal municipal and state levels which make the tax administration in brazil notably bureaucratic.

Setting Up Supplier Withholding For Brazil

The Expat S Guide To Form 1116 Foreign Tax Credit The Expat S Guide To Form 1116 Foreign Tax Credit

This Section Describes How Wages Paid To A U S Citizen Or To A Resident Alien By A U S Person For Serv Federal Income Tax Income Tax Internal Revenue Service

2020 Updates Brazil Draft Law To Resume Income Tax And Dividends Auxadi

Solved For Tax Purposes Gross Income Is All The Money Chegg Com

Step By Step Document For Withholding Tax Configuration Sap Blogs

Irs Aims To Issue New Paycheck Withholding Tables In January Irs Paycheck Health Savings Account

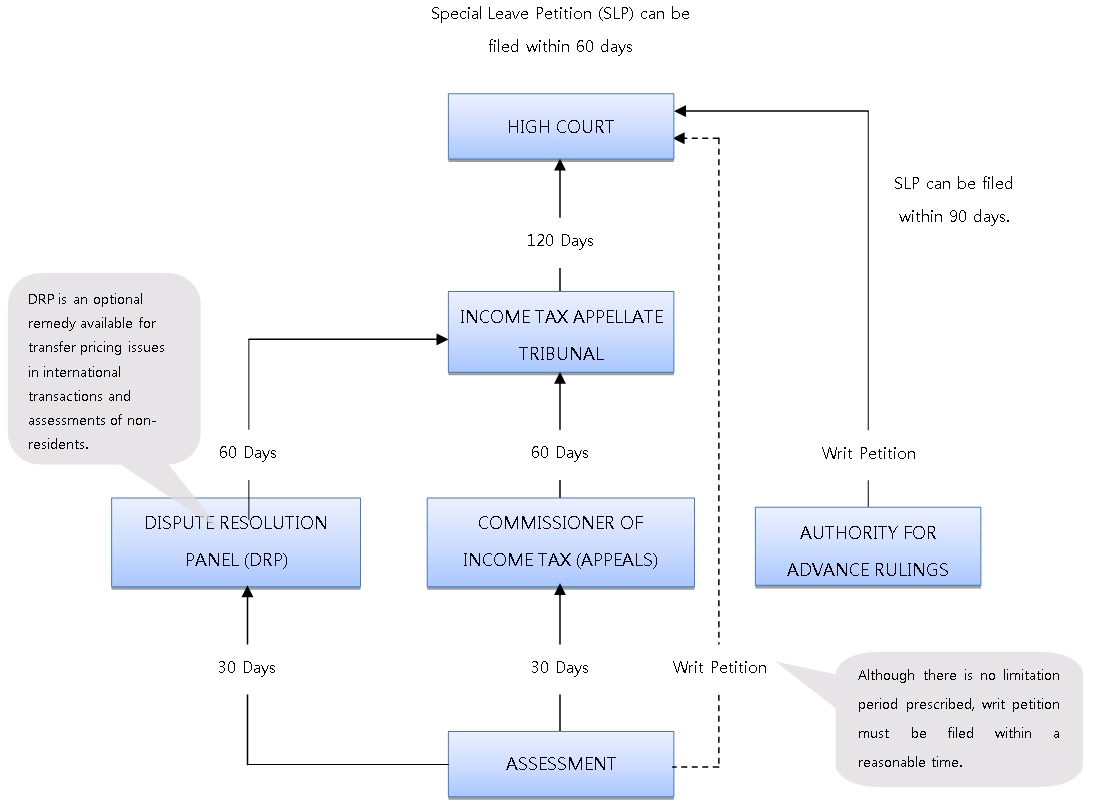

Managing Tax Disputes Some Legal And Practical Strategies Tax India

Global Military Spending Grows For First Time Since 2011 Military Spending Corruption In India Military

Brazil Corporate Taxation In The Dutch Caribbean And Latin American Region

Contact The Munims And Get 25 Off 91 6283275634 0176 2517417 Mail Mail Themunims Com Website Http Www With Images Accounting Services Business Branding Godaddy

Brazil Income Tax Return Central Bank Report Filing Ext Kpmg Global

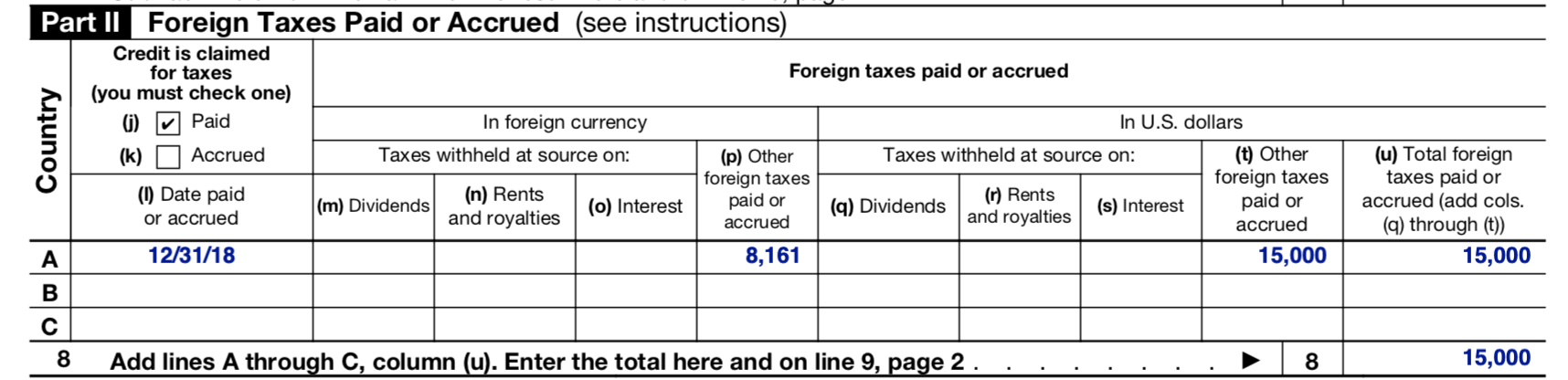

Income Tax Foreign Tax Credits How To Claim A Foreign Tax Credit Where The Foreign Tax Paid Is Covered By A Double Tax Agreement Interpretation Statement Is 16 05