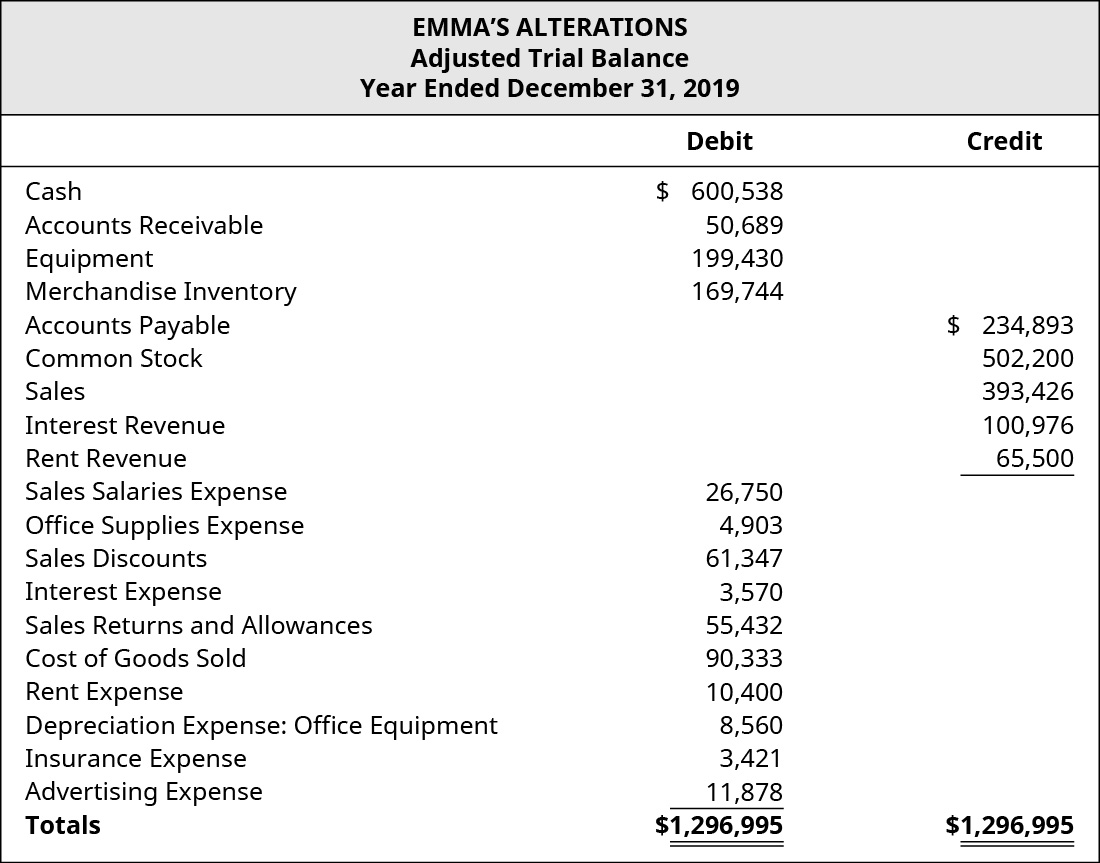

Bad Debt Expense Income Statement Presentation

Receivables Bad Debt Expense And Interest Revenue Ppt Download

Intermediate Accounting Ppt Download

Accounting For Accruals Advanced Topics Receivables And Payables Ppt Download

Multiple Step Income Statement Accountingcoach

Adjustments To Financial Statements Students Acca Global Acca Global

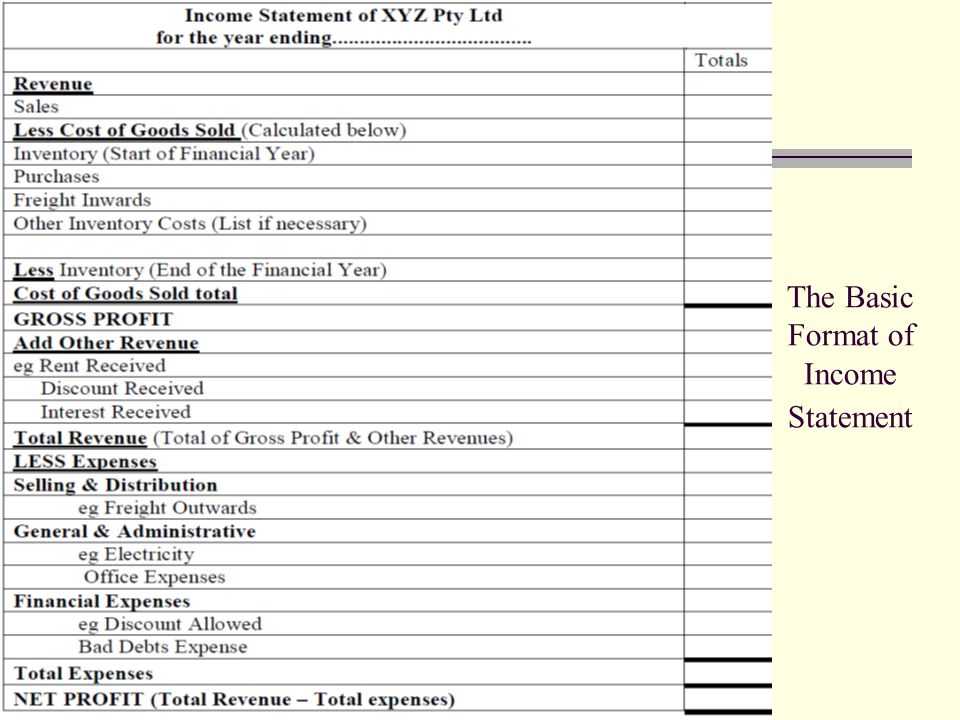

Describe And Prepare Multi Step And Simple Income Statements For Merchandising Companies Principles Of Accounting Volume 1 Financial Accounting

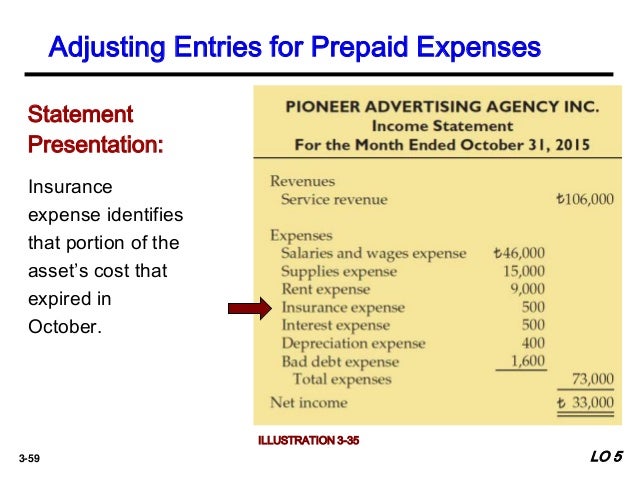

Bad debts are thus included as an expense in the income statement but not included as a line item in the cash flow statement direct method.

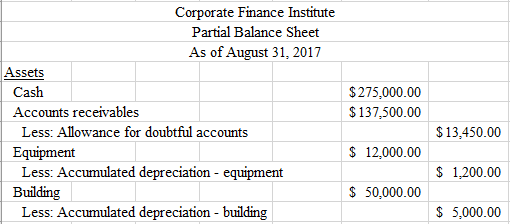

Bad debt expense income statement presentation. It should be noted that bad debts do however form part of the calculation of cash generated from operations when using the indirect cash flow statement which is the preferred method in the us. Suppose hasty hare had current accounts receivable of 160 000 and an allowance for doubtful accounts balance of 12 000. Allowance for doubtful accounts on the balance sheet. Bad debt expense is something that must be recorded and accounted for every time a company prepares its financial statements.

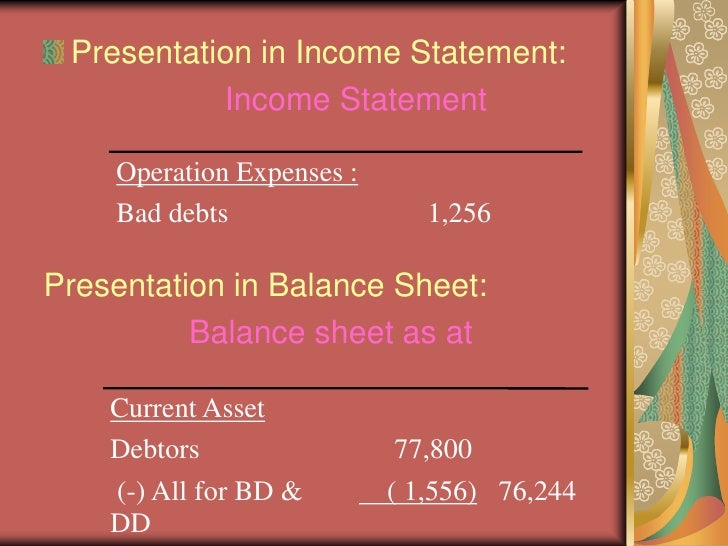

2014 09 revenue from contracts with customers eliminates these types of industry specific presentation rules leading to a major change to how health care organizations present their revenues. Recognizing bad debts leads to an offsetting reduction to accounts. This bad debts expense account will be shown separately under operating expenses on the income statement. Bad debt expense is reported on the income statement bad debt is the expense account which will show in the operating expense of the income statement.

The difference is recorded in the income statement as a provision for bad debt expense and helps calculate net revenue. Bad debt expense is the amount of an account receivable that cannot be collected. Non interest income condensed for presentation purposes non interest expense condensed for presentation purposes 24 income before income taxes income tax expense net income net income available to common 25 26. Bad debt expense also helps companies identify which customers default on payments more often than others.

Bad debt expenses are generally classified as a sales and general administrative expense and are found on the income statement. Accounting standards update asu no. Under the allowance for doubtful accounts method bad debt expense is recorded based on monthly sales. Revenue recognition guidance alters presentation of bad debt for healthcare organizations hospitals clinics and other healthcare organizations should prepare for big changes when implementing fasb s sweeping new rules to calculate the top line in their income statements.

The monthly bad debt expense is added to the allowance for doubtful accounts as a contra account to accounts receivable. An amount that will never be collected is considered a bad debts expense. The customer has chosen not to pay this amount either due to financial difficulties or because there is a dispute over the underlying product or service sold to the customer.

Lesson 3 Income Statements Li Jialong Ppt Download

Ch03 Financial Reporting And Accounting Standards

Bad Debt Overview Example Bad Debt Expense Journal Entries

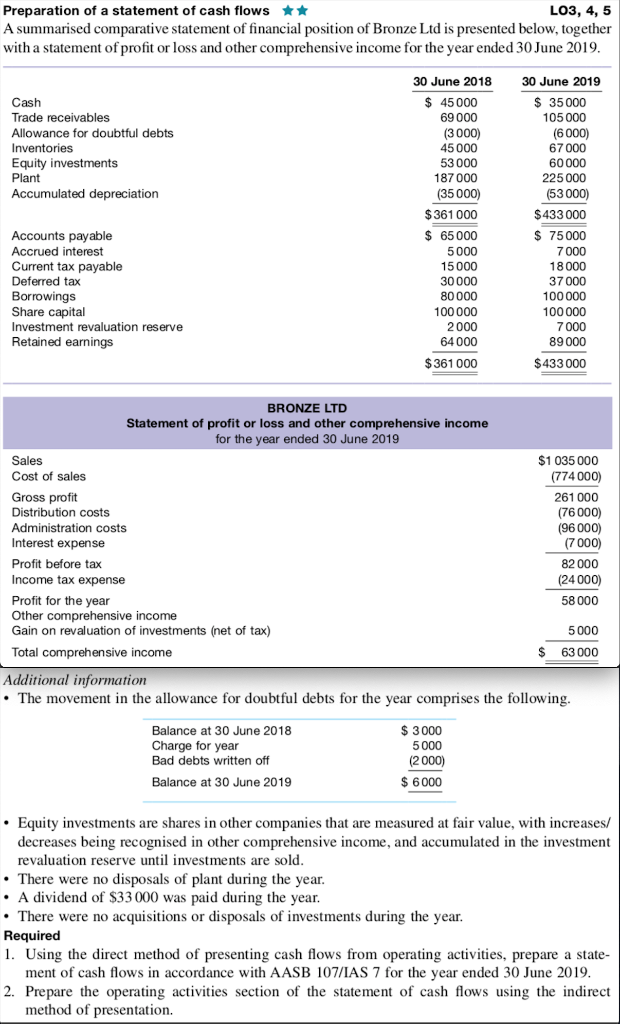

Solved Preparation Of A Statement Of Cash Flows A Summari Chegg Com

2 Income Statement Presentation Alternative Formats 1 Classification By Nature Of Expense Classification On The Basis Of Inputs What The Money Was Spent Ppt Download

Financial Statement Editable Powerpoint Template Financial Statement Financial Statement Analysis Statement Template

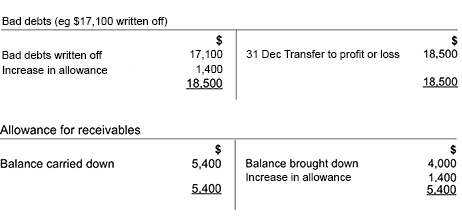

Chapter 25 Bad Debts Allowances For Doubtful Debts And Provisions For Discounts On Accounts Receivable Ppt Download

Best Accounting Flashcards Quizlet

Define And Apply Accounting Treatment For Contingent Liabilities Principles Of Accounting Volume 1 Financial Accounting

Account For Uncollectible Accounts Using The Balance Sheet And Income Statement Approaches Principles Of Accounting Volume 1 Financial Accounting

Ppt Receivables Powerpoint Presentation Free Download Id 5940716

Topic 6 Debtors

The Complete Accounting Cycle Ppt Download