Relative Definition Under Income Tax

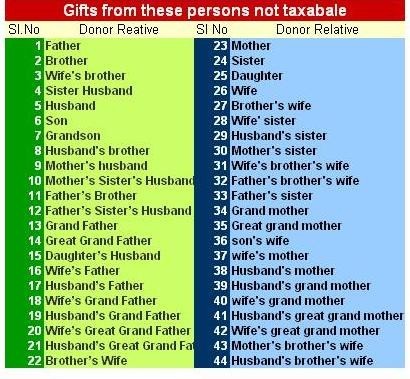

List Of Relatives Covered Under Section 56 2 Of Income Tax Act 1961

Pin On Itr Form

Https Www Saraltaxoffice Com Wp Content Uploads 2019 03 Relatives List As Per Itd Saral Income Tax Pdf

Income Tax Deductions List Fy 2020 21 Save Tax For Ay 2021 22

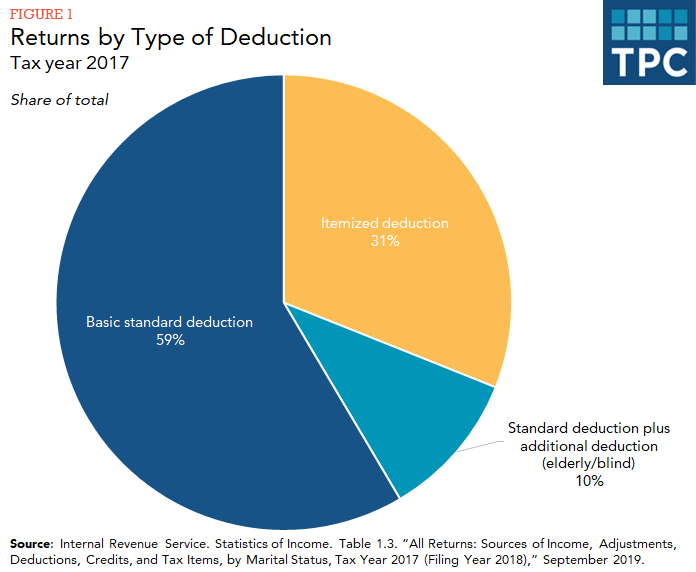

What Are Itemized Deductions And Who Claims Them Tax Policy Center

How Fortune 500 Companies Avoid Paying Income Tax

In the case of pendurthi chandrasekhar v.

Relative definition under income tax. Let us understand the definition of relatives as per the income tax act for gift and under fema. Section 56 did not envisage any occasion for a relative to give a gift. The definition is explained further in section 56 2 vii under which it is cleared that gifts received from relatives are not chargeable under income from other sources further clarifying that they. The fact of adoption is irrelevant in the above provision of income tax act 1961.

A qualifying relative is a person designated by federal income tax code to be allowed to be claimed as a dependent by a taxpayer assuming the taxpayer provided considerable financial support for. Meaning of relative under this section is quite short and crispy. The tax department thought so. You may also refer our other articles on the issue at following link.

As per gift tax any relative means as per section 56 2. The persons who are considered as relatives are. Further definition of relative under section 2 41 of income tax act 1961 is the main definition and if the term relative is not defined specifically under any other section then the meaning of term relative has to be defined according to this section. Dcit 2018 ts 5466 hc 2018 andhra pradesh o the high court held that an occasion is not necessary to accept a gift from a relative.

As per section 2 41 of the income tax act 1961 relative in relation to an individual means the husband wife brother or sister or any lineal ascendant or descendant of that individual. Brother or sister of the spouse of the individual. Income tax act contains various sections which involve relationship between two individuals. For income tax act we need to forget that the relative is a cohesive term.

As per the income tax act. The term relative definition under various laws is given as under. Definition of relative needs to be ascertained from the angel of recipient for each and every gift. A question arose whether for the purpose of levying tax under tamil nadu agricultural income tax agricultural income of any individual shall include agricultural income of a minor child of such individual as arising from assets transferred to the minor by such individual otherwise than for adequate consideration.

The term relative as per income tax act 1961 is defined under section 2 41 which says husband wife brother or sister or any lineal ascendant or descendent of that individual. Relative meaning jan 1 2020 income tax act 1961 kewal garg as per section 2 41 of income tax act 1961 unless the context otherwise requires the term relative in relation to an individual means the husband wife brother or sister or any lineal ascendant or descendant of that individual. In case of an individual. Section 2 41 relative in relation to an individual means the husband wife brother or sister or any lineal ascendant or descendant of that individual.

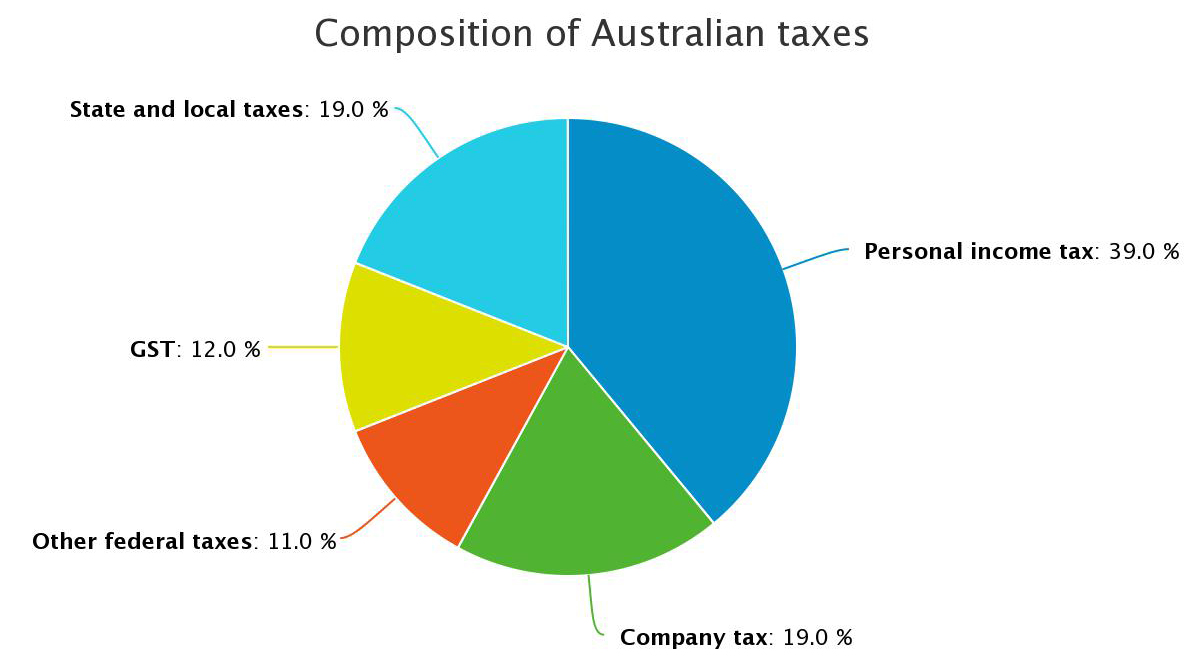

At A Glance Treasury Gov Au

Relative Income Hypothesis Macroeconomics Study Deeper Economics Notes Hypothesis Accounting Notes

The Times Group Tax Free Finance Plan Income Tax

Tax Statement Form Seven Things You Should Do In Tax Statement Form Tax Forms Fillable Forms Excel Templates

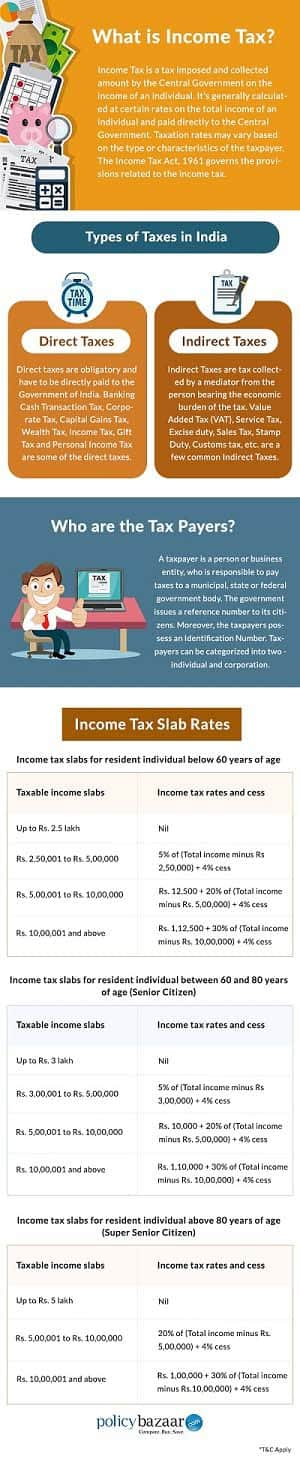

Income Tax It Returns Rules What Is Income Tax For Fy 2019 20

Pin On Money

Relatives U S 56 2 Vii From Whom Gift Is Permissible Income Tax Forum

Definition Of The Daily Favourable Feeding Habitat Orange Line Orange Line Orange Habitats

Pin On Examples Online Form Templates

Income Tax Notes Income From Salary Accounting Taxation Income Tax Income Tax Return Tax

Due Dates Advance Tax Payments Tax Payment Tax Deducted At Source Due Date

:max_bytes(150000):strip_icc()/Clipboard01-42e418fa494247adb22cf86e98cd3537.jpg)

Do Tax Brackets Include Social Security

Financial Capital Structures Define Leverage Owner Lender Risks Financial Business Risk Cost Of Capital