Gaap Statement Of Comprehensive Income

Income Statement Examples Gaap Ifrs Accounting

A Balance Sheet Is Basically A Statement Of Assets And Claim Over Assets Of An Entity As At A Particul Bookkeeping Business Accounting Notes Financial Position

Ifrs Vs Gaap Accounting Amt Training

Us Financial Statements In 2020 Financial Statement Personal Financial Statement Financial

Other Comprehensive Income Overview Examples How It Works

Pension Expense Both Gaap Ifrs For The Income Statement Finance Train

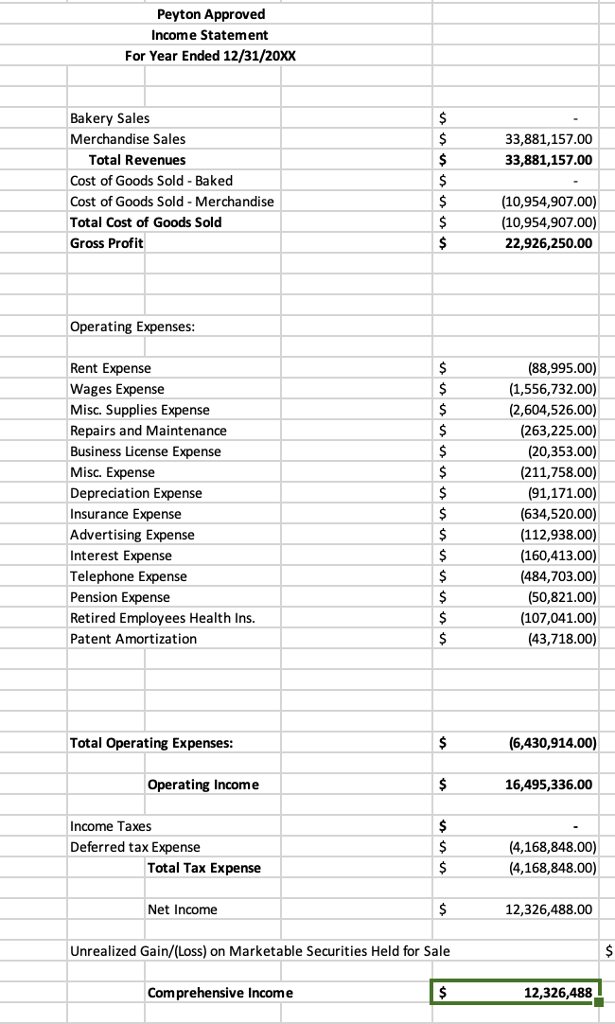

Statement of comprehensive income.

Gaap statement of comprehensive income. A standard ci statement is usually attached to the bottom of the income statement and includes a separate heading. A statement of comprehensive income is the overall income statement that consolidates standard income statement which gives details about the repetitive operations of the company and other comprehensive income which gives details about the non operational transactions such as the sale of assets patents etc. So ifrs is a more comprehensive and informative type of reporting income statement. Limitations of a statement of comprehensive income.

Income and other amounts of current period other comprehensive income. Example 3 ifrs based income statement. Statement of comprehensive income. 4 2 ifrs supplement 3if a company prepares a statement of comprehensive income then disclosure is required for 1 other comprehensive income classified by nature 2 comprehensive income of associates and joint ventures and 3 total comprehensive income the statement of comprehensive.

Although the income statement is a go to document for assessing the financial health of a company it falls short in a few aspects. A statement of comprehensive income that begins with profit or loss bottom line of the income statement and displays the items of other comprehensive income for the reporting period ias 1 p 81 so the statement of comprehensive income aggregates income statement profit and loss statement and other comprehensive income which isn t. 2 scope of section 5. Example 1 single step income statement.

Whenever ci is listed on the balance sheet the statement of comprehensive income must be included in the general purpose financial statements to give external users details about how ci is computed. Income statement example gaap generally accepted accounting principle has two classifications. Schedule reflecting a statement of income statement of cash flows statement of financial position statement of shareholders equity and other comprehensive income or other statement as needed. B5 statement of comprehensive income and income statement.

But don t depend solely on it. 3 presentation of total comprehensive income. The income statement encompasses both the current revenues resulting from sales and the accounts receivables which the firm is yet to be paid. Both before tax and net of tax presentations are permitted provided the entity complies withthe requirements in paragraph 220 10 45 12 correspond to the components of other comprehensive income in the statement in which other comprehensive income for the period is presented.

Generally Accepted Accounting Principles Gaap Accounting Principles Accounting Accounting Basics

Ch 4 The Income Statement Comprehensive Income Chegg Com

Avoiding Missteps In The Lifo Conformity Rule

Staff Accountant Resume Example Latest Resume Format Accountant Resume Resume Examples Resume Objective Statement

The Comprehensive Guide To Understanding Gaap Accounting Com Accounting Principles Business Savvy Understanding

Download Pdf Wiley Gaap 2016 Interpretation And Application Of Generally Accepted Accounting Prin In 2020 Accounting Principles Accounting Principles

Solved Create Notes To The Financial Statement Compose A Chegg Com

Accounting Vs Finance Which Degree Is Right For You Finance Career Finance Degree Accounting

Financial Statements Ppt Download

Pin On International Financial Reporting Standards Ifrs Course

It Concern With The Preparation Of Financial Statements Based On Gaap And Ifrs For Any Respectiv Financial Accounting Financial Information Accounting Services

Income Statement Presentation Ifrs Compared To Us Gaap

Wiley Interpretation And Application Of Ifrs Standards 2019 Ebook Interpretation Download Books Free Books Online