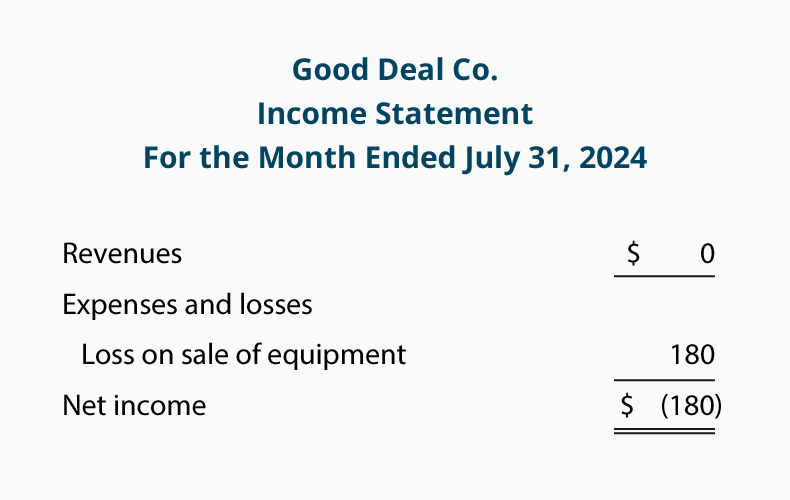

Gain On Sale Of Fixed Assets Income Statement Presentation

Income Statement Components Under Ias 1 Income Statement Personal Financial Statement Financial Statement

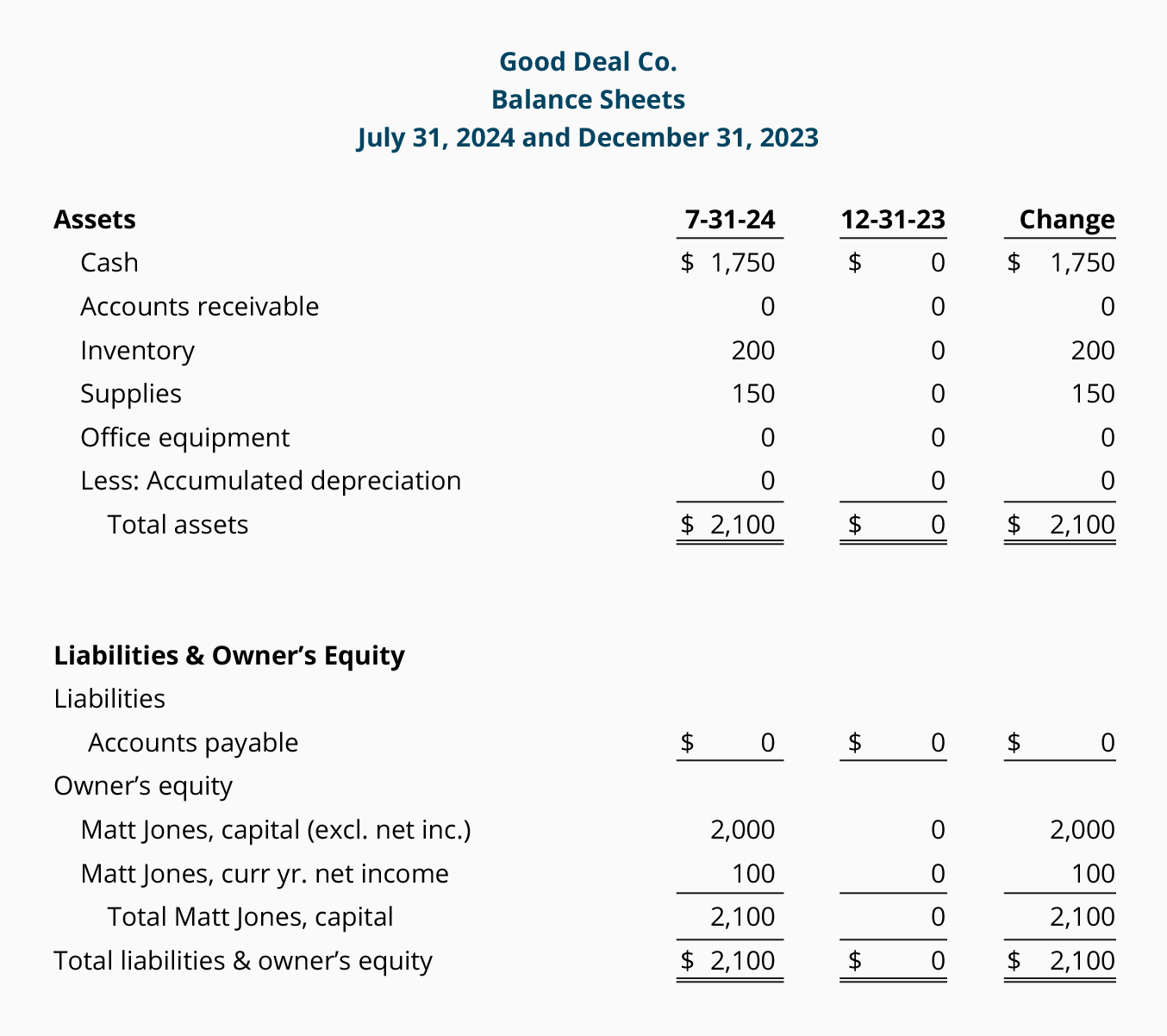

Disposal Of Assets Sale Of Asset Accountingcoach

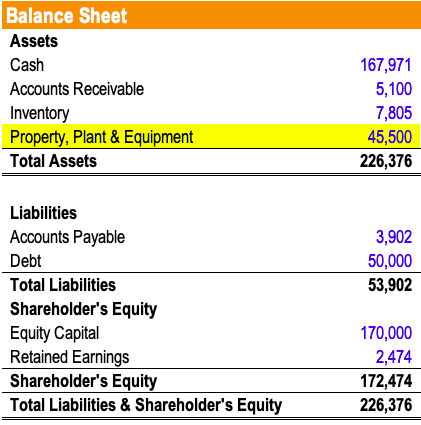

A Balance Sheet Is Basically A Statement Of Assets And Claim Over Assets Of An Entity As At A Particul Bookkeeping Business Accounting Notes Financial Position

Pin On Quotation

Free Downloadable Excel Pro Forma Income Statement For Small And New Businesses Income Statement Statement Template Financial Statement

Disposal Of Assets Sale Of Asset Accountingcoach

Gain on revaluation of investments.

Gain on sale of fixed assets income statement presentation. Our financial reporting guide financial statement presentation details the financial statement presentation and disclosure requirements for common balance sheet and income statement accounts it also discusses the appropriate classification of transactions in the statement of cash flows and addresses the requirements related to the statements of stockholders equity and other comprehensive. This type of asset provides long term financial gain has a useful life of more than one year and is classified as property plant and equipment pp e on the balance sheet. The sale would appear on the income statement but as a gain or loss on sale not revenue. Dividend income and interest income should be classified under investing activities unless in case of for example an investment bank.

Gaap perspective presentation of the. A gain on sale of assets arises when an asset is sold for more than its carrying amount the carrying amount is the purchase price of the asset minus any subsequent depreciation and impairment charges. Net income 77 000. Removal of income to be presented elsewhere in the cash flow statement e g.

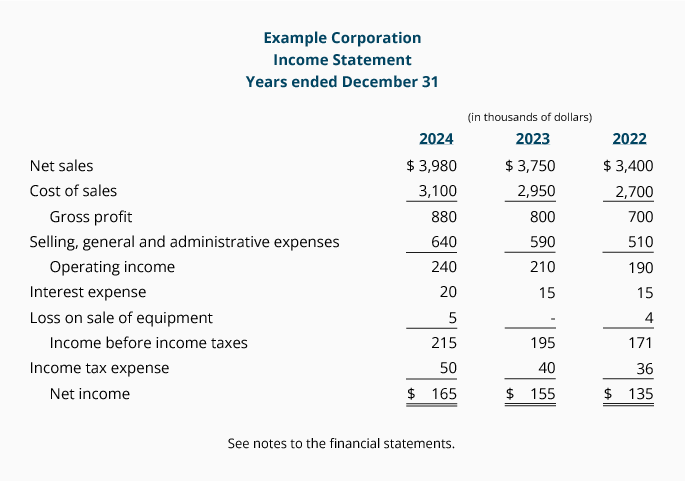

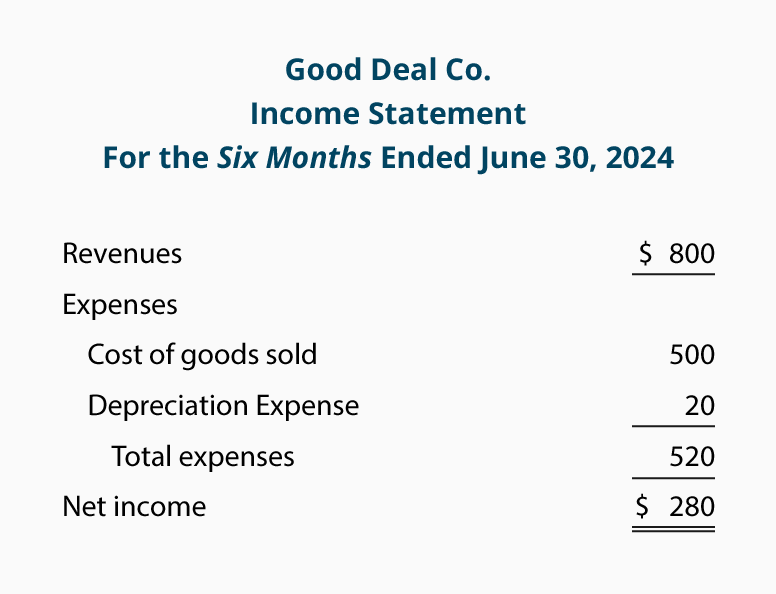

Gain on sale of plant assets 30 000 171 410 income from operations 357 483 interest on bonds and notes 126 060 income before income tax 231 423 income tax 66 934 net income for the year 164 489 attributable to. Net income before taxes 82 000. Gain loss on disposition 2 000. The income statement may look like this.

Either of the following. If a company disposes of sells a long term asset for an amount different from the amount in the company s accounting records its book value an adjustment must be made to the net income shown as the first amount on the cash flow statement. Where it goes the typical income statement starts with sales revenue then subtracts operating expenses which are just the regular day to day costs of doing business. Change in net assets for a not for profit entity of the discontinued operation for the periods in which the results of operations of the discontinued operation are presented in the statement where net income is reported or statement of activities for a not for profit entity.

Elimination of non cash income e g. Shareholders of boc hong 120 000 non controlling interest 44 489 earnings per share 1 74 u s. Example of gain or loss on the sale of fixed assets. Veristrat defines operating income as the money you make from your core business whether.

For example a business buys a machine for 10 000 and subsequently records 3 000 of depreciation.

Balance Sheet Analysis Part 4 Of The Introduction To Financial Statement Analysis Video Series Fro Financial Statement Analysis Financial Statement Financial

Multiple Step Income Statement Accountingcoach

A Sample Income Statement Modified For Common Size Analysis Income Statement Profit And Loss Statement Bookkeeping Business

How To Prepare Projected Balance Sheet Accounting Education Balance Sheet Accounting Education Accounting

Statement Of Comprehensive Income Overview Components And Uses

Forecasting Income Statement Interest Expense Wall Street Prep

Basic General Journal Entries And Format Journal Entries Learn Accounting Accounting Notes

Pin On The Accountant In Me

Single Step Vs Multi Step Income Statement Key Differences For Small Business Accounting

Financial Ratio Analysis Google Search Financial Ratio Financial Engineering Financial Statement Analysis

Depreciation Expense Depreciation Accountingcoach

Fixed Assets Definition Characteristics Examples

Hotel Valuation Financial Model Template Efinancialmodels Business Valuation Financial Modeling Revenue Management