Income In Respect Of A Decedent Self Employment Tax

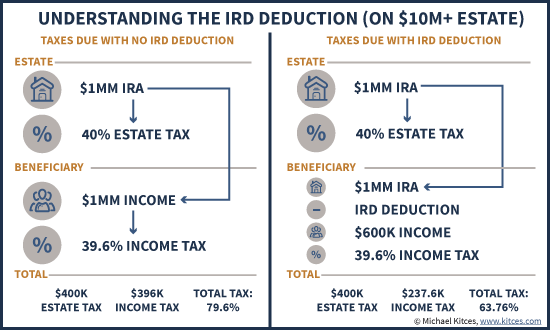

The Ird Deduction Inherited Ira Beneficiaries Often Miss

Pin By Sylvia Ducom On Quotes One Sentence Quotes Amazing Quotes Jack Sparrow Quotes

Income Statement Templates 29 Free Docs Xlsx Pdf Statement Template Income Statement Profit And Loss Statement

/GettyImages-BA61273-883c9d0942db4168b8acd8b51acbe1bd.jpg)

Income In Respect Of A Decedent Ird Definition

Historical Growth Of The World Population Since Year 0 Open I World Population Historical Death Metal

Top Tax Write Offs For The Self Employed Turbotax Tax Tips Videos Tax Write Offs Business Tax Small Business Tax

In other words the income in respect of a decedent is the gain the decedent would have realized had he lived.

Income in respect of a decedent self employment tax. 611 depletion deductions and the sec. For self employment tax purposes only the decedent s self employment income will include the decedent s distributive share of a partnership s income or loss through the end of the month in which death occurred. 862 discusses the scheme for taxing income in respect of a decedent ird. The ird scheme is intended to eliminate as much as possible the consequences of death on the operation of the income tax laws.

The most common types of ird include annuities retirement plans and final wage payouts. Income in respect of a decedent ird defines a category of receipts received after the taxpayer passes away which are taxed differently from most of the decedent s other assets. This type of income in respect of a decedent should be reported as other income in box 3 of form 1099 misc. Bloomberg tax portfolio income in respect of a decedent no.

212 expenses for the production of income sec. The gain to be reported as income in respect of a decedent is the 1 000 difference between the decedent s basis in the property and the sale proceeds. 164 deductions for taxes sec. 163 interest deductions sec.

Income in respect of a decedent. Since this was paid in the year after he died this should be reported on a 1099 misc to you but it isn t subject to self employment tax. However there are many other less readily identifiable types of ird. Income in respect of a decedent ird is money owed to a person before they passed away like a salary or wages.

This problem has been solved. High died on february 15 before receiving payment. Include self employment income actually or constructively received or accrued depending on the decedent s accounting method. 162 business expenses sec.

More on this concept is irs publication 559 survivors executors and administrators under income in respect to a decedent for a little more for background irs publication 525 taxable and. The term income with respect to a decedent refers to those amounts to which a decedent was entitled but which were not properly includible in computing his her taxable income for the taxable year ending with the date of his her death or for a previous taxable year under the method of accounting employed by the decedent i. The so called deductions in respect of a decedent drd encompass five deductions and one credit including sec. 27 foreign tax credit see regs.

How Property Is Divided When A Man Dies Intestate Intestate Succession Property Legal Services Property Management

Is Your Inheritance Considered Taxable Income H R Block

Empowering Women Part1 Healthy Food List Kids Diet Healthy Eating For Kids

10 Exceptional Executive Summary Template Pdf 2020 Template For Free In 2020 Executive Summary Template Executive Summary Example Executive Summary

Pin On Reminders For Jfb

Ask The Taxgirl Tax On Income Received After Death

Https Www Accaglobal Com Content Dam Acca Global Pdf Students 2012 Sa Oct10 F6 Mys Pdf

Https Www Irs Gov Pub Irs Drop Rr 82 196 Pdf

Power Of Attorney General Power Of Attorney Form Legal Forms Power Of Attorney

How Does The Personal Representative Deal With The Income And Capital Gains Arising After The Deceased S Death Low Incomes Tax Reform Group

Http Bit Ly 2viazvb Labour Ministry Seeks Collaboration With Afdb On Job Creation Http Bit Ly African Development Bank Public Private Partnership Lettering

Publication 514 2019 Foreign Tax Credit For Individuals Internal Revenue Service

Income Tax Deductions For Salaried Employees Fy 2019 20