Income Statement Presentation Gain On Sale Of Asset

Disposal Of Assets Sale Of Asset Accountingcoach

Learn The Basics Of Preparing An Income Statement Income Statement Profit And Loss Statement Cost Of Goods Sold

Income Statement Components Under Ias 1 Income Statement Personal Financial Statement Financial Statement

Small Business Income Statement Template Inspirational Download Our Free In E Statement Template In 2020 Income Statement Statement Template Profit And Loss Statement

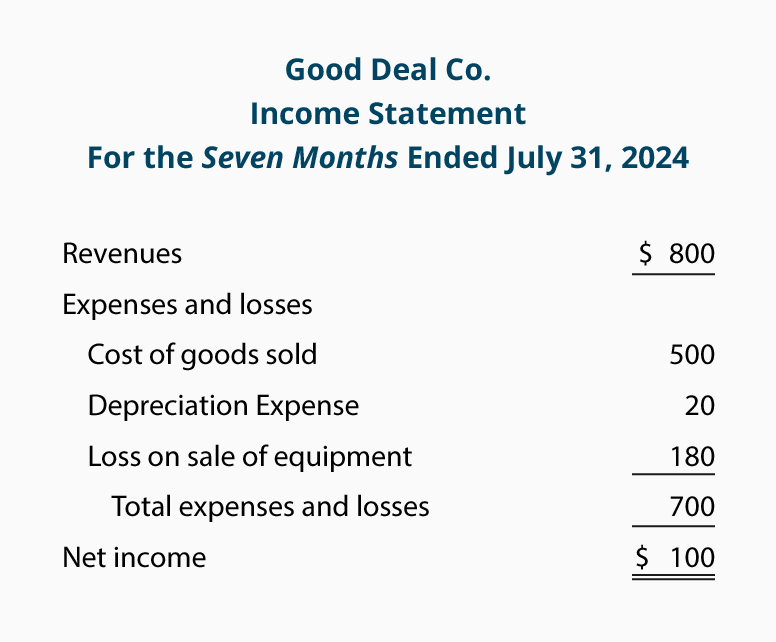

Income Statement Expense And Losses Accountingcoach Income Statement Statement Template Profit And Loss Statement

Depreciation Turns Capital Expenditures Into Expenses Over Time Income Statement Income Financial Statement

For more on the several meanings of capital in business finance and economics see capital.

Income statement presentation gain on sale of asset. The company records this 50 000 as a gain on sale of investments on its income statement under other income. The asset s net value gets subtracted out in the operating section because that section will have already reflected the gain in net income from the income statement. Say your construction company owns a forklift. However cash was not reduced.

This loss was reported on the income statement thereby reducing net income. The gain is classified as a non operating item on the income statement of the selling entity. When your company sells off an asset or investment any gain on the sale should be reported on your income statement the financial statement that tracks the flow of money into and out of your business. From the above example we can say that unrealized gain is a difference between the value of investment now and the investment done in the past.

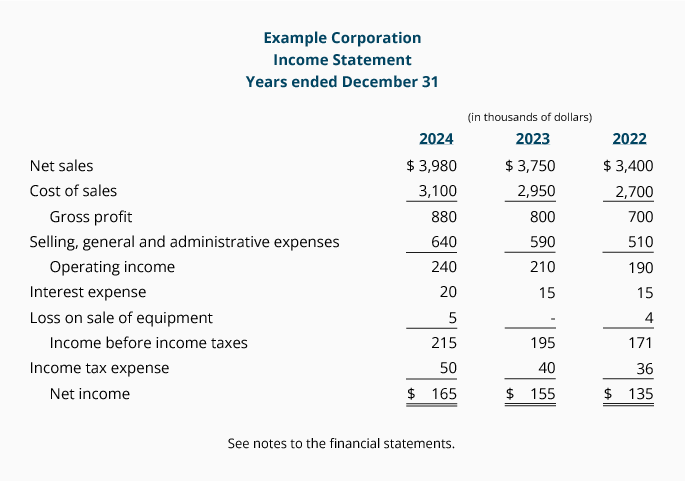

A gain on sale of assets arises when an asset is sold for more than its carrying amount the carrying amount is the purchase price of the asset minus any subsequent depreciation and impairment charges. Cash of 900 was actually received from the sale of the equipment and it appears in its entirely in the investing activities section of the cash flow statement. A company purchases 700 000 in shares of ford. In the income statement example in exhibit 1 below for instance capital gains taxes income taxes on gain are taxes on a profit from an extraordinary item sale of land during the reporting period.

The post tax profit or loss for the period from the discontinued operations and. However say he sells these positions for 30000 later in the year or next year it would record a realized gain of 20000 in the net income and he is liable to pay taxes on such gains. For example a business buys a machine for 10 000 and subsequently records 3 000 of depreciation. If instead of selling for 5 500 it sold for 3 000 giving you a 1 500 loss you present the loss on asset disposal on the income statement as a negative.

Our financial reporting guide financial statement presentation details the financial statement presentation and disclosure requirements for common balance sheet and income statement accounts it also discusses the appropriate classification of transactions in the statement of cash flows and addresses the requirements related to the statements of stockholders equity and other comprehensive. Eighteen months later it sells these shares for 750 000. It is subtracted from other income. Inventory on july 31 is 200 4 calculators at a cost of 50 each.

The post tax gain or loss on disposal based on the fair value minus costs to sell of the asset or disposal group. However because of the circumstances under which you received this money the gain should not be counted as revenue. There must be a single amount on the face of the statement of comprehensive income or income statement for the total of.

Pin On Quotation

Connections Between Income Statement And Balance Sheet Accounts Income Statement Accounting Jobs Accounting Education

A Balance Sheet Is Basically A Statement Of Assets And Claim Over Assets Of An Entity As At A Particul Bookkeeping Business Accounting Notes Financial Position

Cash Flow Statement Payment And Equipment Accountingcoach Cash Flow Statement Cash Flow Education Sales

Financial Statement Example Of A Company 4 Things Your Boss Needs To Know About Financial In 2020 Financial Statement Statement Template Personal Financial Statement

Basic Income Statement Example And Format Income Statement Profit And Loss Statement Statement Template

How To Create A Basic Profit Loss Statement Free Download The Spreadsheet Alchemist Profit And Loss Statement Statement Template Statement

Income Statement Template 7 Income Statement Statement Template Financial Statement

Pin On The Accountant In Me

Multiple Step Income Statement Accountingcoach

Part A Prepare Financial Statements Income Statement Financial Statement Income Statement Financial

Free Downloadable Excel Pro Forma Income Statement For Small And New Businesses Income Statement Statement Template Financial Statement

Financial Statement Editable Powerpoint Template Financial Statement Financial Ratio Powerpoint Presentation Design