Income Tax Act Zimbabwe 2017

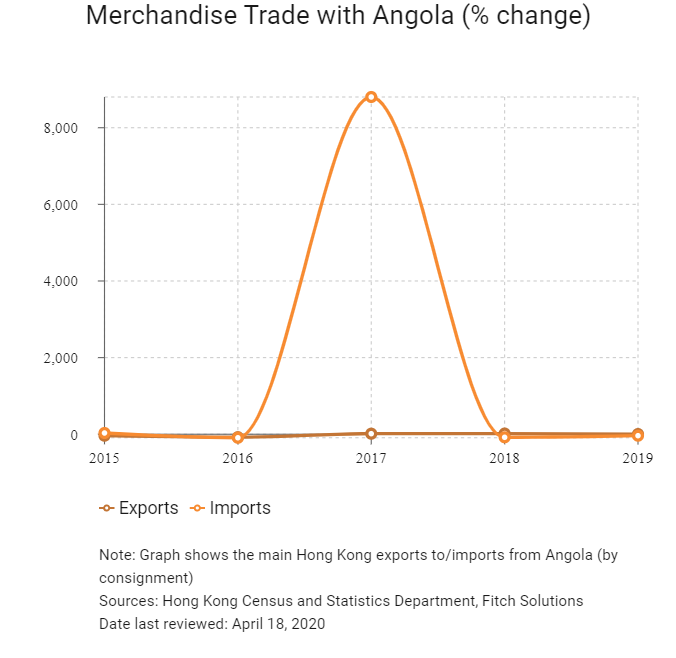

Angola Market Profile Hktdc Research

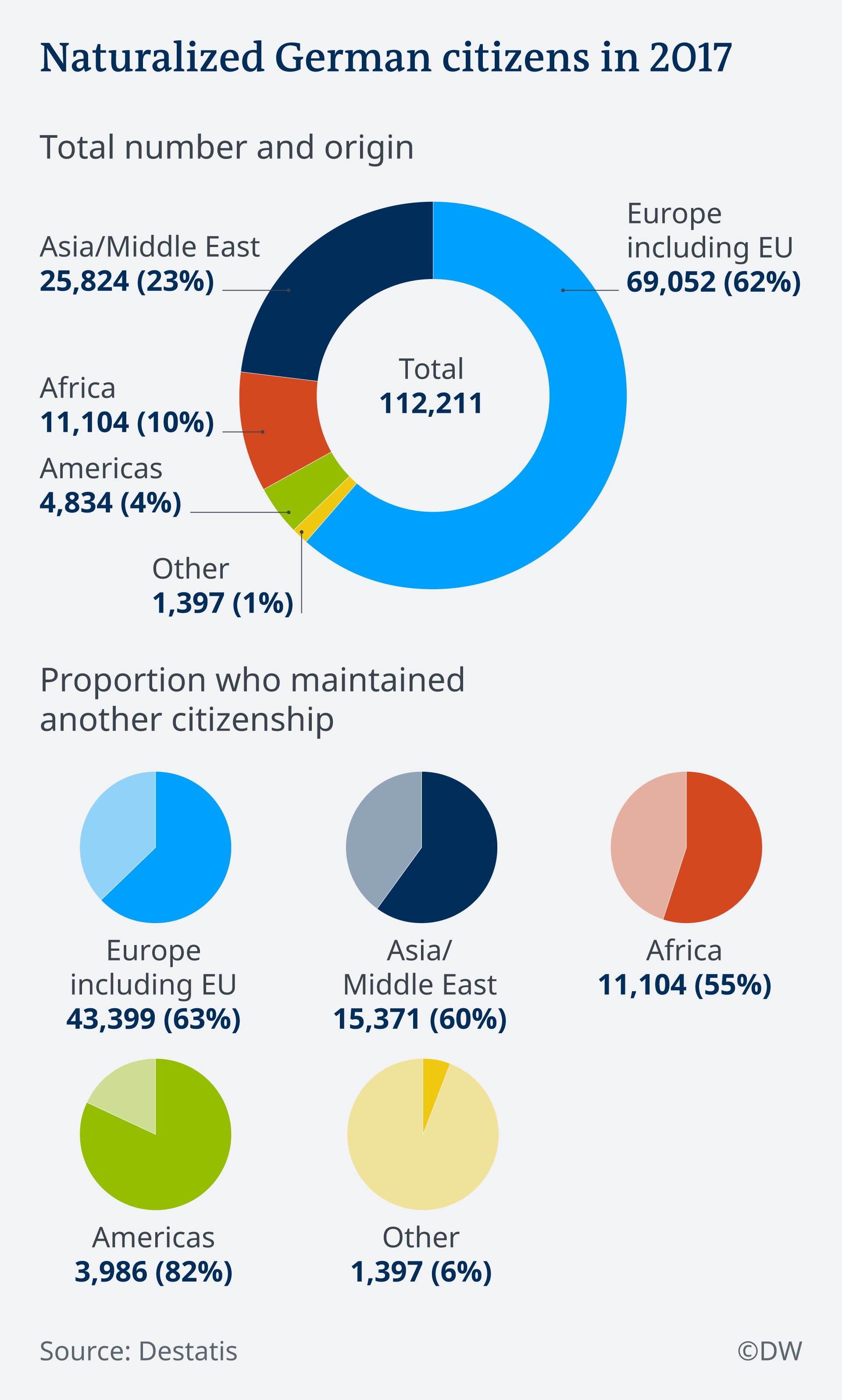

Liicornell Thanks For Being The Wikipedia Of Laws Knowledge Is Power Standuprepublic Mldschool Nvcopblock Definitions Knowledge Is Power Knowledge

Pdf A Review Of Mining Taxes In Africa Tax Burden The Strength Of Democratic Systems And Levels Of Corruption

Angola Hktdc Belt And Road Portal

Https Juta Co Za Media Filestore 2017 11 Tax Law Review November 2017 Doc Pdf

2019 Insurance Industry Outlook Deloitte

2 interpretation 1 in this act affiliate in relation to a petroleum operator has the meaning given by subsection 4 of section thirty two.

Income tax act zimbabwe 2017. It has been indicated that zimbabwe is considering moving to a residence based system during the current tax reform exercise. Income tax act 1 1 2017 thin capitalisation payment of tax on deemed dividend zimbabwe currently a thin capitalization rule which effectively can result in a tax disallowance of borrowing costs relating to the portion of debt. The zimbabwe income tax act chapter 23 06 was amended with effect from 1 january 2016 to incorporate section 98a and 98b which provide for the commissioner general s power to make appropriate adjustments where the arms length principle is deemed not to have been observed. Zimbabwe s finance act 2 of 2017 took effect upon its publication government gazette no.

This requirement extended to payments made to non residents. Zimbabwe s finance act 2 of 2017 took effect upon its publication government gazette no. 18 of 24 march 2017. Tax rates individuals employment income.

The act contains provisions concerning individuals that affect the taxation of severance rental income pension pay outs various tax credits employee fringe benefits nonresident directors fees and permanent establishment. Income derived or deemed to be derived from sources within zimbabwe is subject to tax. The current legislation requires registered businesses to withhold and remit to zimra 10 of the payment of usd 1 000 in aggregate per annum made to a local business not in possession of a tax clearance certificate itf 263. The act contains provisions concerning individuals that affect the taxation of severance rental income pension pay outs various tax credits employee fringe benefits nonresident directors fees and permanent establishment.

This act may be cited as the income tax act chapter 23 06. 2 of 2017 0 income of.

Https Www Pwc Com Gx En Tax Corporate Tax Worldwide Tax Summaries Pwc Worldwide Tax Summaries Corporate Taxes 2017 18 Africa Pdf

Https Www Unilever Com Images Unilever Annual Report On Form 20 F 2017 Tcm244 516429 En Pdf

Https Www Un Org Esa Ffd Wp Content Uploads 2017 10 15stm Crp23 Technical Services Pdf

Http Atlasmara Com Media 1332 2017 Results Presentation Pdf

Courts Of Zimbabwe Author At Tpcases Com

Proceedings From Nec 2017 By Undp Independent Evaluation Office Issuu

Oecd Ilibrary Home

Https Ec Europa Eu Eurostat Documents 3859598 8141546 Ks Gq 17 002 En N Pdf 6edae81c F570 4174 B5c8 D8ba927e8e7e

Https Www Dlapiper Com Media Files Insights Publications 2017 05 Apa Map Guide 2017 P

Https Www Rbz Co Zw Documents Mps Mpsaug2017 Pdf

Striving For People Planet And Peace 2017