Income Tax Withholding Rules Pakistan

Pakistan Budget Fy 2019 20 Income Tax Measures World News Observer

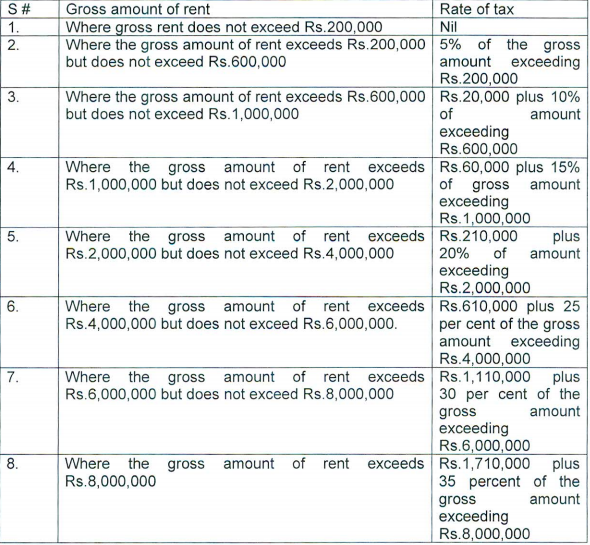

Fbr Not To Tax Annual Property Rent Income Of Up To Rs0 2m Profit By Pakistan Today

Petiwala Books Complete Withholding Income Tax Sales Tax On Services Laws In Pakistan

Withholding Tax Not Levied On Motorcycle Auto Riksha Federal Board Of Revenue Government Of Pakistan

Tax Excellence Team Quick Increment In Salary Bonus Workshop Call Now For Enroll Today 02134329107 To 109 In 2020 Web Marketing Network Marketing Internet Marketing

Updated up to june 30 2020.

Income tax withholding rules pakistan. Main source of revenue by govt. Withholding tax rates applicable withholding tax rates. If a reduced rate is available in a tax treaty such rate would be applicable. Explains the provisions of the income tax ordinance 2001 governing withholding tax in a simple and concise manner.

Almost 70 percent revenue source as reported in 2017. Inherited from income tax act 1922 in which withholding concept of salary and interest was present only. Section 165 filing of income tax biannual withholding statement itrp services pakistan january 08 2020 every person collecting tax under division ii of this part 1 or chapter xii 2 or the tenth schedule or deducting tax from a payment under division iii of this part 3 or chapter xii 4 or the tenth schedule shall 5 furnish to the. The tax withheld is deemed to be the final tax liability of the non resident.

O persons from whom tax is to be deducted or collected. In general payments made on account dividend interest royalties and fee for technical services income derived from pakistan sources are subject to a 15 withholding tax wht which tax has to be withheld deducted from the gross amount paid to the recipient. In the case of a non resident where royalty or fts is attributable to a pe in pakistan the amount of royalty fts shall be chargeable to tax as normal income. Tax laws amendment ordinance 2016 8 ordinance no xv of 2015 the exemption of withholding tax under sub section 4 of section 236p of the income tax ordinance 2001 available to pakistan real time interbank settlement mechanism prsm has been withdrawn.

Withholding income tax regime wht rates card guideline for the taxpayers tax collectors withholding tax agents as per finance act 2020 updated up to june 30 2020 disclaimer this withholding tax rates card is just an effort to have a ready reference and to facilitate all the stakeholders of withholding tax regime. It mainly revolves around the obligations of the withholding agents as to collection or deduction of tax at source i e.

Https Download1 Fbr Gov Pk Sros 2019101151017301sro1160 Pdf

Profit On Debt 2020 Section 151 And 7b Income Tax Rate On Profit Youtube

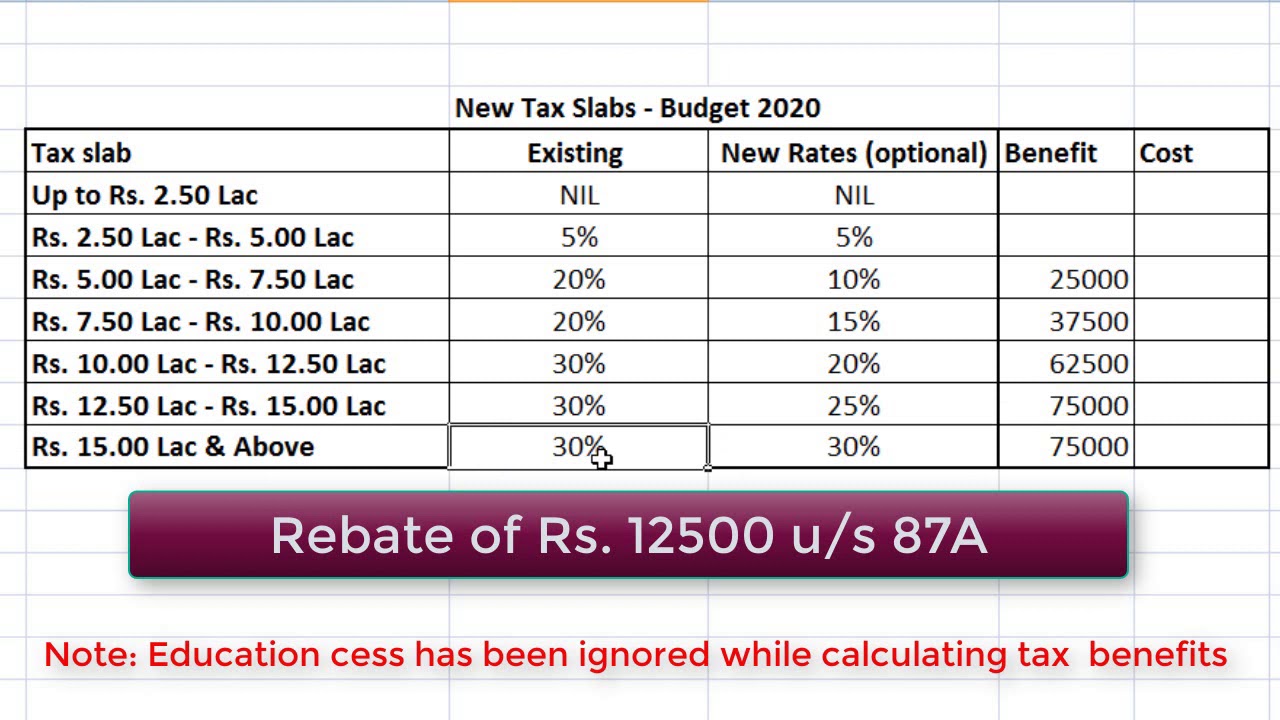

Budget 2020 New Income Tax Rates New Income Tax Slabs Income Tax Calculation 2020 21 Youtube

What S The Difference Between Quarterly Taxes Vs Annual Taxes Quarterly Taxes Tax Tax Payment

Income Tax Ordinance 2001 Pcda Pakistan Chemists Druggists

Major Changes To Income Tax Law Made Through Finance Bill 2020 Pkrevenue Com

Karachi Federal Board Of Revenue Fbr Has Been Urged To Reduce The Amount Of Penalty In Case Of Defaulting In Filing State Federal Board Tax Rules Tax Refund

Softax Private Ltd Workshop On Advanced Salary Taxation Special Emphasis On Complex Issues And Tax Saving Opti In 2020 Income Tax Return Emphasis Tax Return

No More Withholding Tax On Educational Fees In 2020 Education School Fees Tax Payer

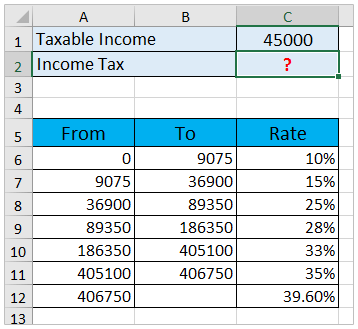

How To Calculate Income Tax In Excel

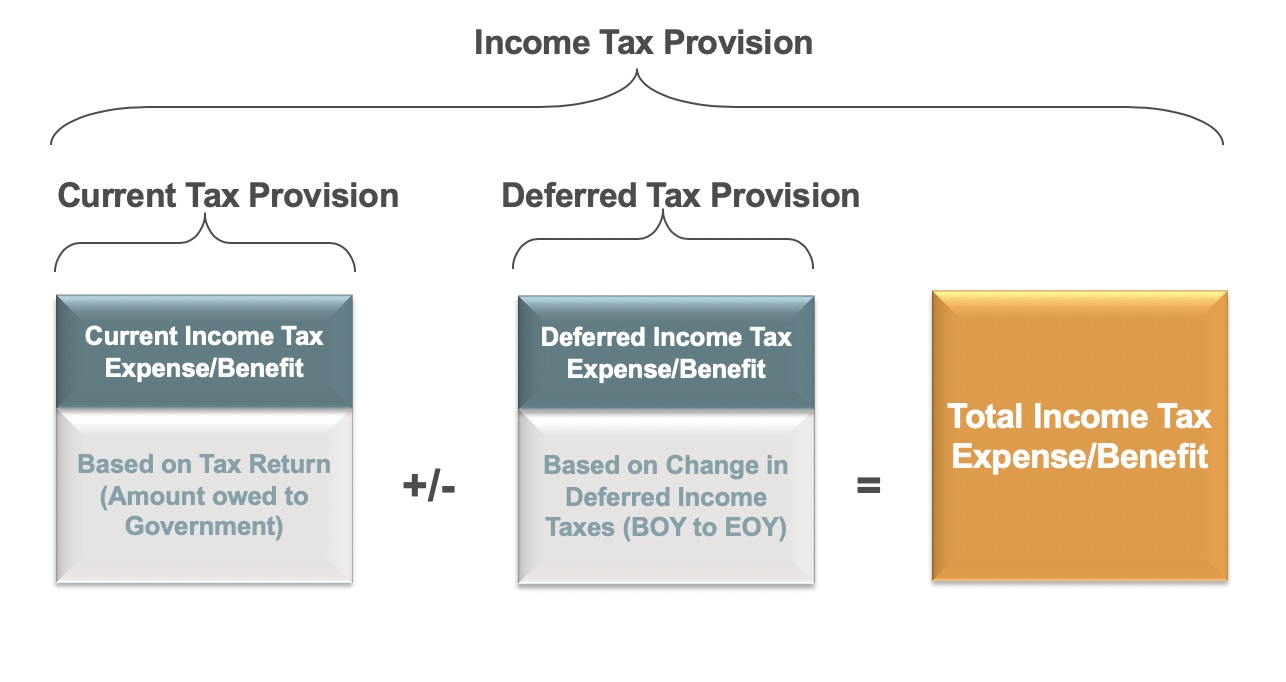

Accounting For Income Taxes Under Asc 740 An Overview Gaap Dynamics

Pm Imran Khan Big Order In 2020 Tax Consulting Imran Khan Tax Services