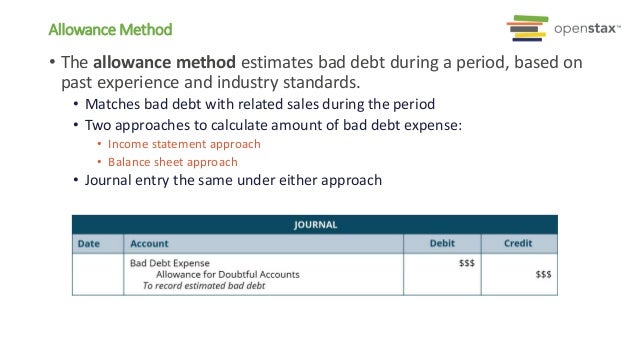

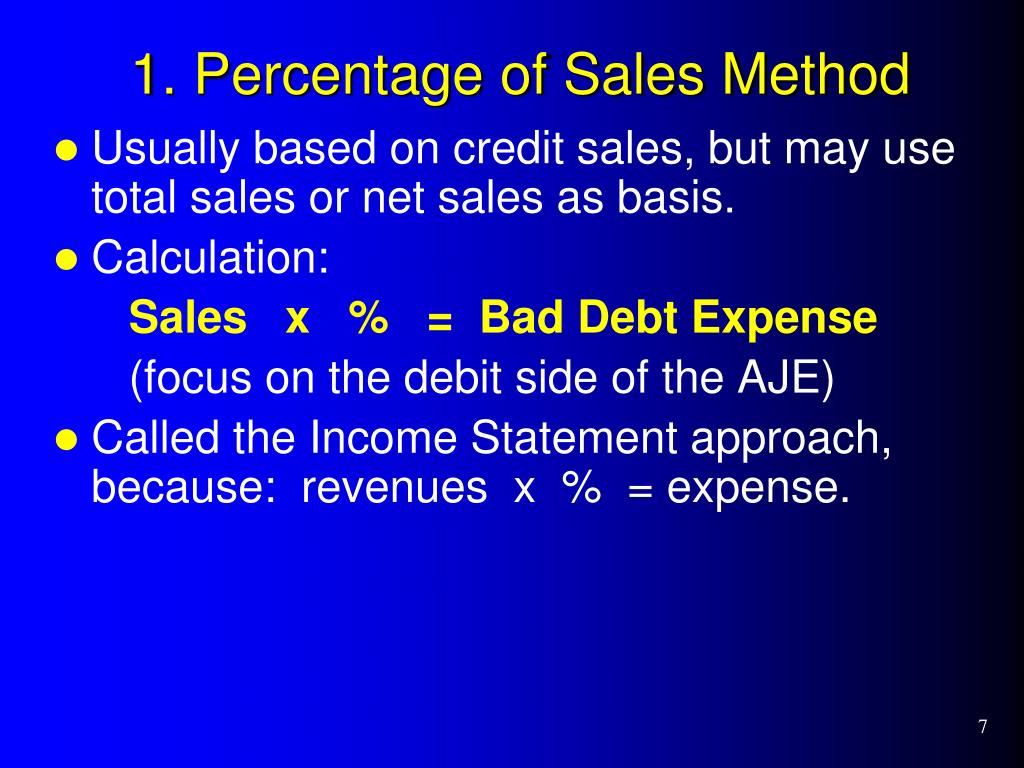

Outline The Income Statement Approach To Calculating The Bad Debts Expense

Account For Uncollectible Accounts Using The Balance Sheet And Income Statement Approaches Principles Of Accounting Volume 1 Financial Accounting

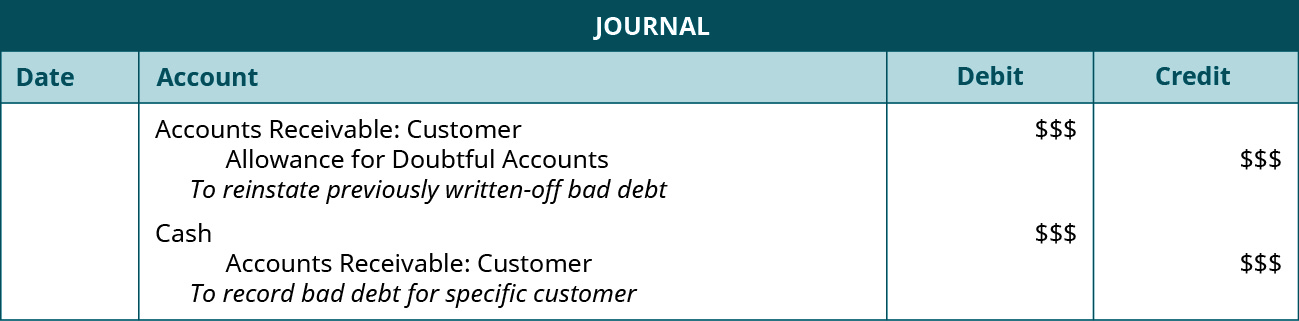

Writing Off An Account Under The Allowance Method Accountingcoach

Chapter 11 Long Term Assets

Assessment Questions Pdf Free Download

Multiple Step Income Statement Accountingcoach

Ppt Chapter 7 Accounts Receivable And Notes Receivable Powerpoint Presentation Id 498078

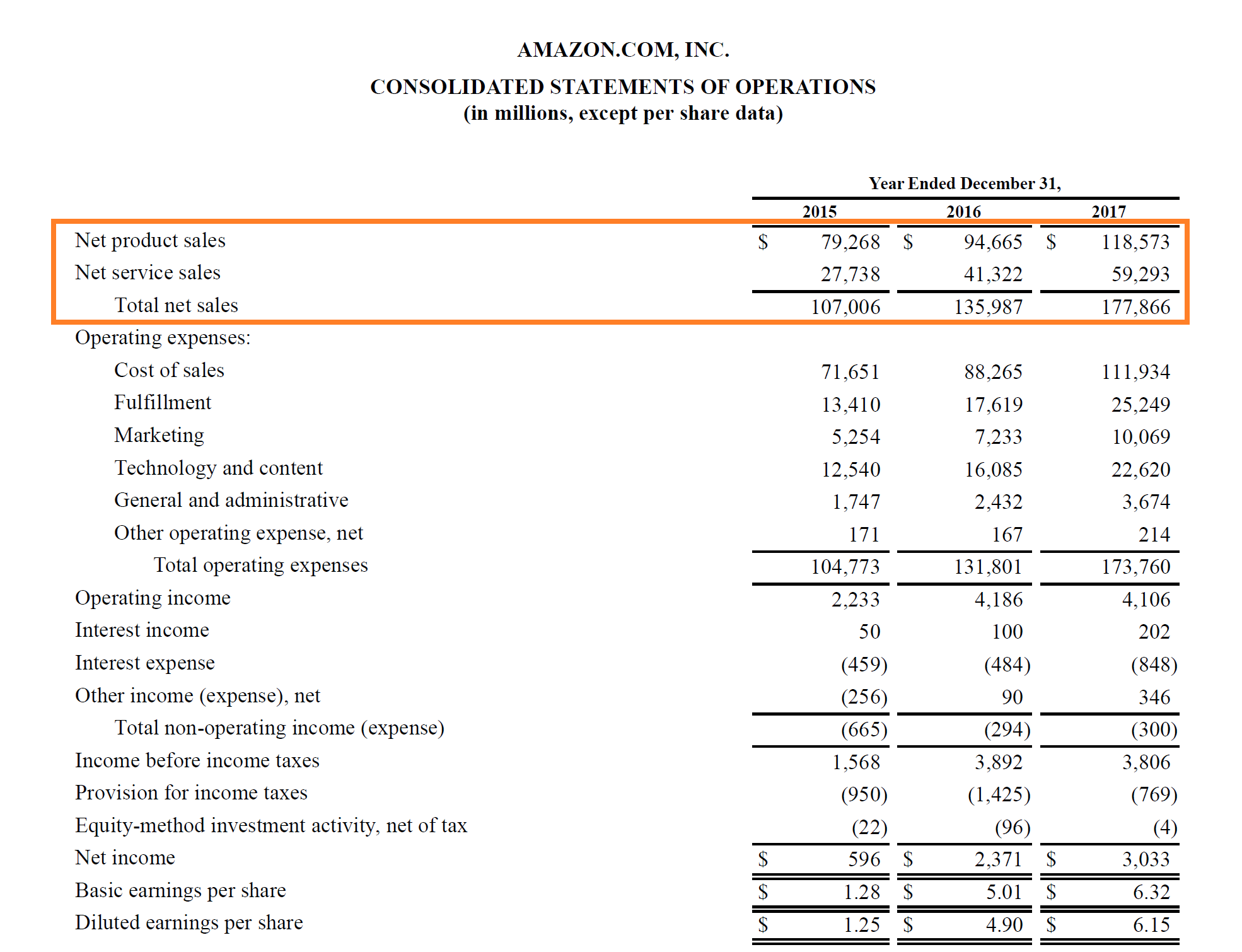

Bad debts get recorded on a company s income statement.

Outline the income statement approach to calculating the bad debts expense. On the income statement bad debt expense would still be 1 of total net sales or 5 000. Why is there a difference in the amounts for bad debts expense and allowance for doubtful accounts. It means under this method bad debt expense does not necessarily serve as a direct loss that goes against revenues. The difference between.

The reason why this contra account is important is that it exerts no effect on the income statement accounts. The income statement approach to estimating bad debts determines bad debt expense directly by relating uncollectible amounts to credit sales. It s an inevitable reality that not all customers will pay down their account balances. The balance sheet approach to bad debts expresses uncollectible accounts as a percentage of accounts receivable.

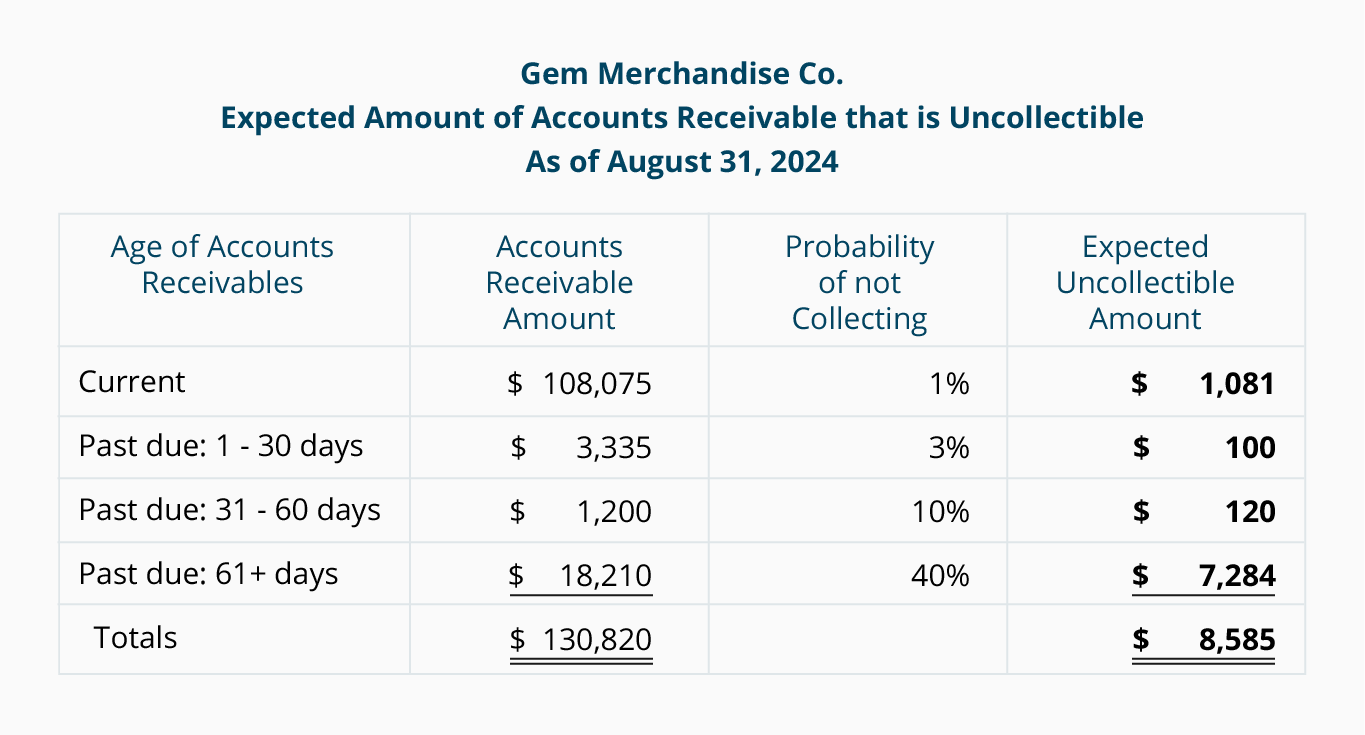

Bad debt expense equation helps in obtaining a true and fair view of financial statements as net profit and debtors are correctly estimated by identifying bad and doubtful debts. For example at the end of the accounting period your business has 50 000 in accounts receivable. Under this approach businesses find the estimated value of bad debts by calculating bad debts as a percentage of the accounts receivable balance. With respect to financial statements the seller should report its estimated credit losses as soon as possible using the allowance method.

Journal entry dr bad debts expense 400 cr allowance for doubtful debts 400 the balance sheet approach is superior to the income statement approach because it ensure s the net balance of accounts receivable is the best. In applying the percentage of sales method companies annually review the percentage of uncollectible accounts that resulted from the previous year s sales. Amount reported as bad debts expense the amount reported in the income statement account bad debts expense pertains to the estimated losses from extending credit during the period shown in the heading of the income statement. Bad debt expense recognized through the allowance method helps the organization to keep some funds aside for meeting future expenses.

To account for this lost income businesses record bad debt expense on a periodic basis.

Aging Of Accounts And Mailing Statements Accountingcoach

Estimating Bad Debts Financial Accounting

Chapter 7 Cash And Receivables Pdf Free Download

The Income Statement Boundless Accounting

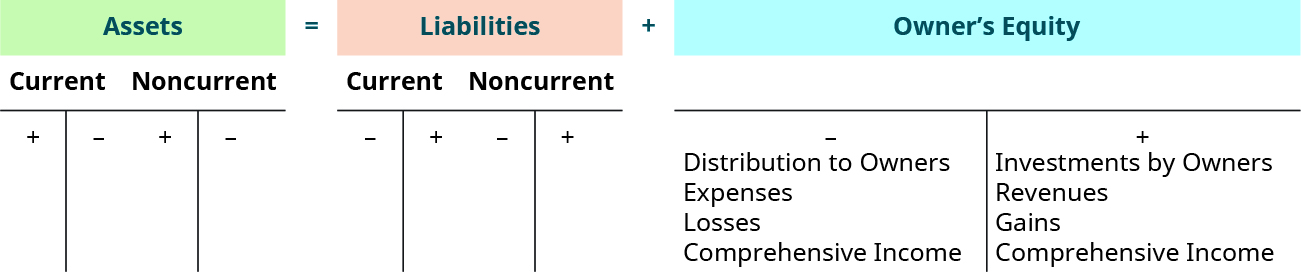

Define Explain And Provide Examples Of Current And Noncurrent Assets Current And Noncurrent Liabilities Equity Revenues And Expenses Principles Of Accounting Volume 1 Financial Accounting

Two Different Ways To Measure Bad Debt Allowance

Provision For Doubtful Debts Or Allowance For Bad Debts Or Allowance For Un Collectible Accounts Definition Types Calculation General Entries Solved Examples

Define And Explain Common Types Of Receivables Pdf Free Download

Credit Risk And Allowance For Losses Accountingcoach

Sales Revenue Definition Overview And Examples

The Income Statement Approach For Estimating Bad Debts Focuses On Current Years Course Hero

Review For Exam No 3 Acct 2301 Sac Chapters 7 9 Pdf Free Download

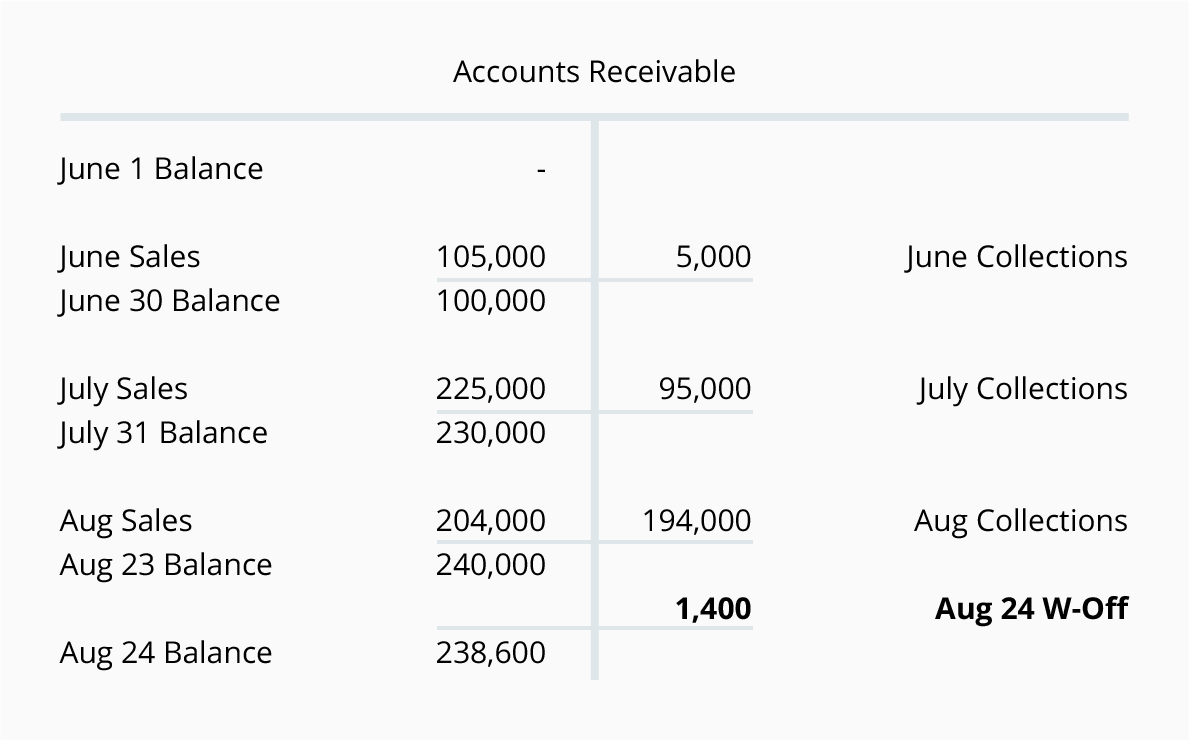

Https Www Csulb Edu Mdchase 500salesandreceivables Pdf