Capital Vs Revenue Expenditure Income Tax Act

:max_bytes(150000):strip_icc()/dotdash_Final_Capital_Expenditures_vs_Revenue_Expenditures_Whats_the_Difference_2020-01-160a38c63f364966bfc46acc4b6b2917.jpg)

How Do Capital And Revenue Expenditures Differ

Taxation In Spain Wikipedia

Taxation In Germany Wikipedia

Income Tax Return Reconciliation Income Tax Return Income Tax Tax Return

Revenue Growth From Vips In Macau Has Turned Around Suggesting The Chinese Economy Has Turned Around As Well Revenue Growth Chart Graphing

Taxmann S Capital Markets Securities Laws By Siddhartha Sankar Saha Incorporated Credit Ranking Ipo Grading Money Market Capital Market Marketing Security

For instance the alteration of accounting entry of the capital expenditure if recorded in the revenue by mistake or intention it shrink the amount of revenue and profit while revenue expense if capitalised appreciates the profits which misrepresent the actual position of the business.

Capital vs revenue expenditure income tax act. Commissioner of income tax 1998 232 itr 771 commissioner of gift tax v. Several previous year v. Capital expenditure produces benefits for several previous years whereas revenue expenditure is consumed within a previous year. Distinguish has to be made between revenue losses and capital losses of the business because under the provisions of this act capital losses can be set off against the income from capital gain only whereas the revenue losses are business losses and as such can be set off against any other income of the assessee.

To hold that all expenditure which is revenue in nature would not fall under section 35ab of the act and would have necessarily to fall under section 37 of the act to our. It refers to the distinction of capital from revenue expenditure for tax purposes. According to mohanlal hargovind of jubbulpore vs. Acquisition of fixed assets v.

Capital v revenue expenditure is a term used throughout this toolkit. Business expenditure capital vs. Expenditure that is capital is generally. Routine expenditure capital expenditure is incurred in acquiring extending or improving a fixed asset whereas revenue expenditure is incurred in the normal course of business as a business expenditure.

Revenue expenditure is taken into account while computing taxable profits and would be eligible for a tax deduction whereas on capital expenditure only depreciation can be claimed.

Ream More Incometax Taxes Capitalgain Property Management Money Everydaytaxes Since The Decision In 2020 Capital Gain Income Tax This Or That Questions

Overview Of Revenue And Capital Expenditure

Pro Forma Income Statement Income Statement Statement Template Profit And Loss Statement

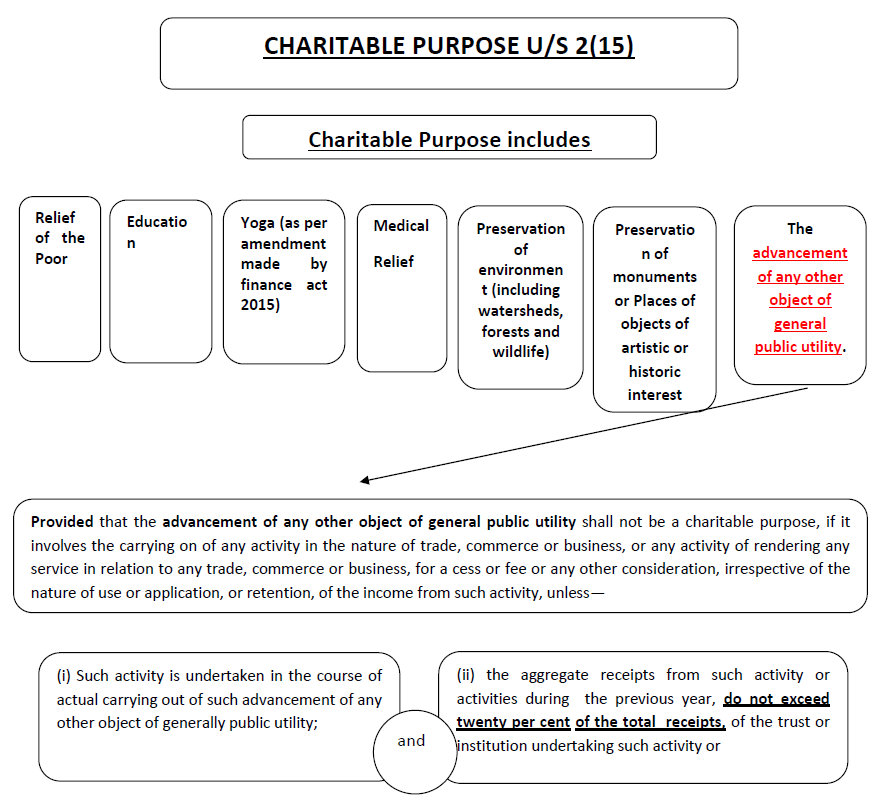

Provisions Of Charitable Trust As Amended By Finance Act 2020

Africa Tax In Brief 18 Feb 2020 Lexology

Plus One Accountancy Notes Chapter 8 Financial Statements I Financial Statements Ii A Plus Topper Financial Statement Financial Chapter

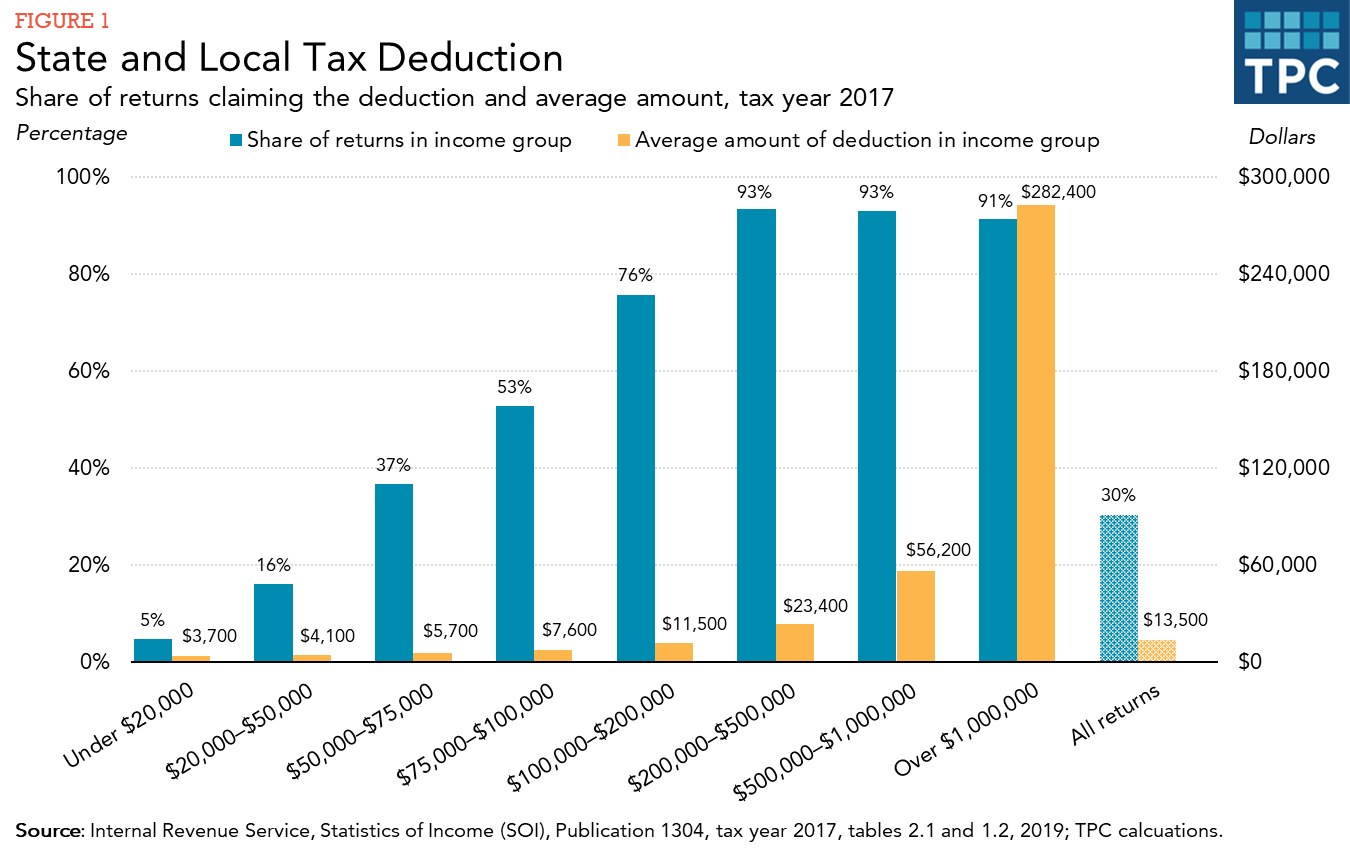

How Does The Deduction For State And Local Taxes Work Tax Policy Center

Pdf The Impact Of Personal Income Tax On Government Expenditure In Oyo State

Section 35d Preliminary Expenses Untying The Knots

Income From Other Sources Casual Income Residual Dividend Income

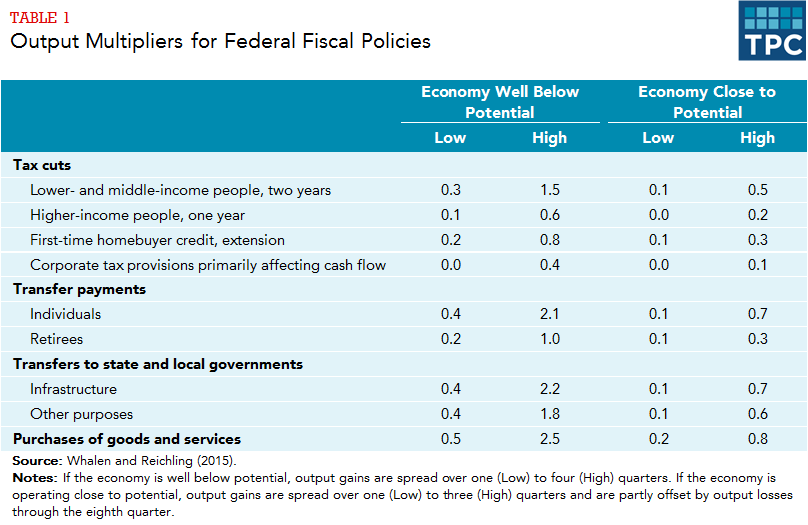

How Do Taxes Affect The Economy In The Short Run Tax Policy Center

Capital Loss Set Off Rules On Sale Of Stocks Equity Mutual Fund Schemes Mutuals Funds Cost Of Capital Fund

How Did The Tax Cuts And Jobs Act Change Personal Taxes Tax Policy Center