Ifrs 17 Income Statement Presentation

Ifrs 17 Presentations Of Revenue And Income Statement Without Premiums

The New Ifrs 17 Disclosure In Short What Needs To Be In The Financial Statement

Https Www Ifrs Org Media Feature Supporting Implementation Ifrs 17 Webcast Ifrs 17 Recognising The Contractual Service Margin In Profit Or Loss Ifrs 17 Ic Webcast Csm Allocation Slides Pdf

Ifrs 17 Insurance Contracts

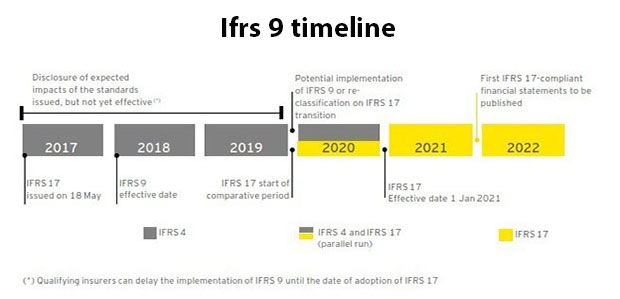

Https Www Ifrs Org Media Feature Supporting Implementation Ifrs 17 Webcast Ifrs 17 Transition To Ifrs 17 Ifrs 17 Webcast Transition To Ifrs 17 Combined Pdf

Ifrs 17 Explained Understanding The New Accounting Standard

Financial highlights 15 consolidated statement of profit or loss 16 consolidated statement of profit or loss and.

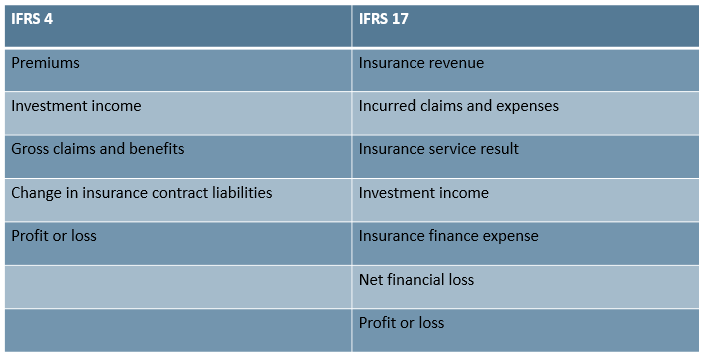

Ifrs 17 income statement presentation. In this article we highlight key considerations affecting preparers when choosing the structure format and contents of the income statement and other presentation matters. Other comprehensive income 17 consolidated statement of financial position 18 consolidated statement of changes in equity 20. Reporting of investment components separately from insurance contract. The standard requires a complete set of financial statements to comprise a statement of financial position a statement of profit or loss and other comprehensive income a statement of changes in equity and a statement of cash flows.

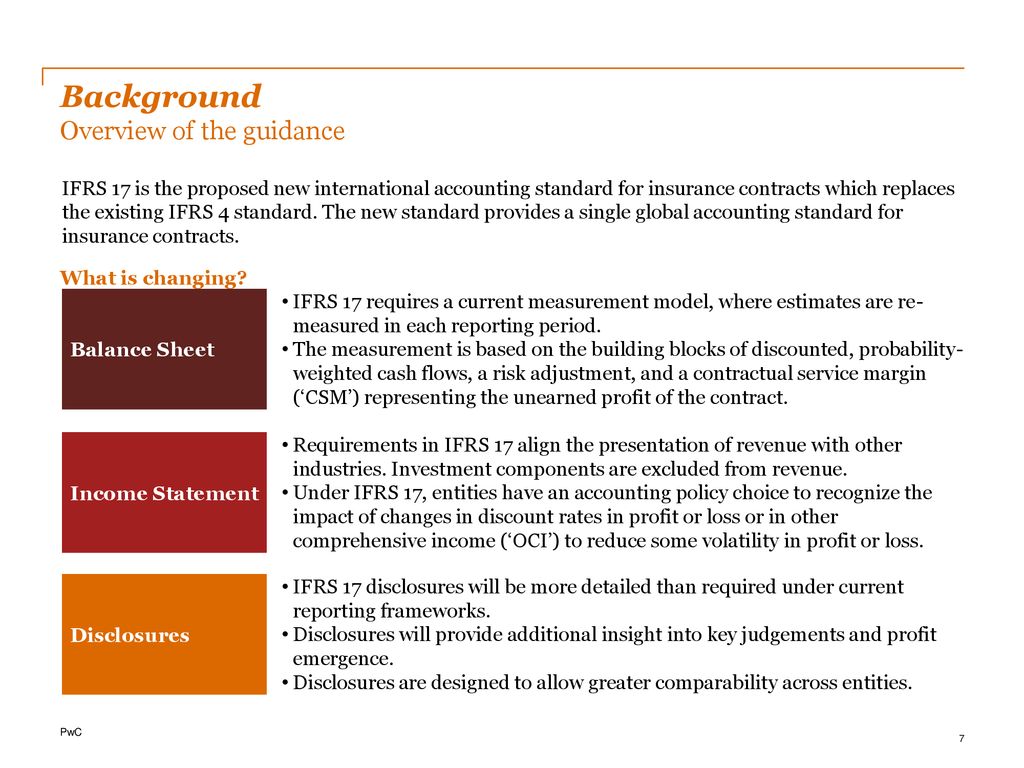

Ifrs 17 establishes the principles for the recognition measurement presentation and disclosure of insurance contracts within the scope of the standard. The objective of ifrs 17 is to ensure that an entity provides relevant information that faithfully represents those contracts. About ifrs 17 5 about the group 9 independent auditors report 10 consolidated financial statements 14. Example 3 ifrs based income statement.

Ifrs 17 has impact on all parts here we will focus on the balance sheet income statement and changes in equity balance sheet the presentation of the consolidated balance sheet will often only have minor changes. This information gives a basis for users of financial statements to assess the effect that insurance contracts have. Ifrs preparers have some flexibility in selecting their income statement format and which line items headings and subtotals are to be presented on the face of the statement. Presentation of financial statements 231 v example disclosures for entities that early adopt ifrs 9.

Employee benefits 2011 255 vii example disclosures for entities that. Suppose pqr is a uk based company that follows ifrs for reporting. The insurance assets and insurance liabilities need to be splits right now they can be aggregated same holds for the reinsurance. In the above example we can see that apart from normal entities all the activities that are unusual and continuous are also taken into count.

Detailed analyses of movements in insurance liabilities in the period. Financial instruments 2010 233 vi example disclosures for entities that early adopt ias 19. Presentation and disclosure ifrs 17 will transform the presentation ofinsurers income statements and bring disclosure requirements which will be new to many including. Ias 1 was reissued in september 2007 and applies to annual periods beginning on or after 1 january 2009.

Https Www Ifrs Org Media Feature Supporting Implementation Ifrs 17 Webinar Understanding Ifrs 17 Nss Webinar Slides Pdf

Ifrs 17 Insurance Contracts The Final Standard Is Here Ppt Download

Ifrs 17 9 Series A Fork In The Road Insurance Asset Risk

Https Www Actuaries Org Uk Documents C1 Gi Gi Age Ifrs

Ifrs 17 5 Questions Every Insurer Should Ask Bdo Canada

Session 55 Ifrs 17 What To Expect When You Re Expecting A New Standard

Http Www Actuariesindia Org X 1 S Viwei0zlsr0z0h55njtpun45 Seminardocs 9th 20cbgi Ppt Ifrs 2017 20data 20and 20disclosure 20requirements 20 20 20rajesh 20dalmia Pdf

Profit Emergence Under Ifrs 17

General Insurance The Wide Ranging Implications Of Ifrs 17 The Actuary

Https Www Pwc Ie Publications 2017 Ifrs17 In Depth A Look At Current Financial Reporting Issues Pdf

What Is Sap Insurance Analyzer Financial And Risk Management Accounting Jobs Risk Management Accounting