Income Tax Rates Estate Administration

New Federal Income Tax Rates 2018 Mortgage Interest Rates Pay Off Mortgage Early Mortgage Payoff

How Does Your State Structure Its Individual Income Tax Brackets Like The Federal Income Tax 33 States And Income Tax Brackets Tax Lawyer Federal Income Tax

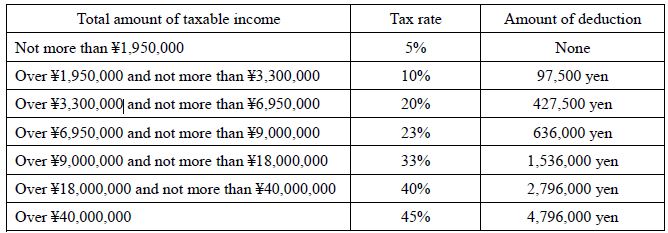

Real Estate Related Taxes And Fees In Japan

Distributable Net Income Tax Rules For Bypass Trusts

Income Tax And Capital Gains Rates 2017 Skloff Financial Group Capital Gain Income Tax Income

Irs Releases 2020 Tax Rate Tables Standard Deduction Amounts And More Tax Brackets Standard Deduction Income Tax Brackets

Unlike individuals executors do not benefit from the personal allowance personal savings allowance or the dividend allowance.

Income tax rates estate administration. For instance the chart above would suggest that a 15 000 estate would have tentative tax of 2 800. This will depend on the types of assets in the estate and is levied on dividends or distributions from investments interest from savings rents and other kinds of income. Furthermore there is no liability to higher rate tax. At that point the prs will account for the tax paid on the estate income for the whole administration period to hmrc under the informal procedure.

The applicable rates of income tax for prs are 7 5 on dividend income and 20 on savings and other income. Technically there is tentative estate tax liability for even the smallest taxable estates.

How The Tcja Tax Law Affects Your Personal Finances

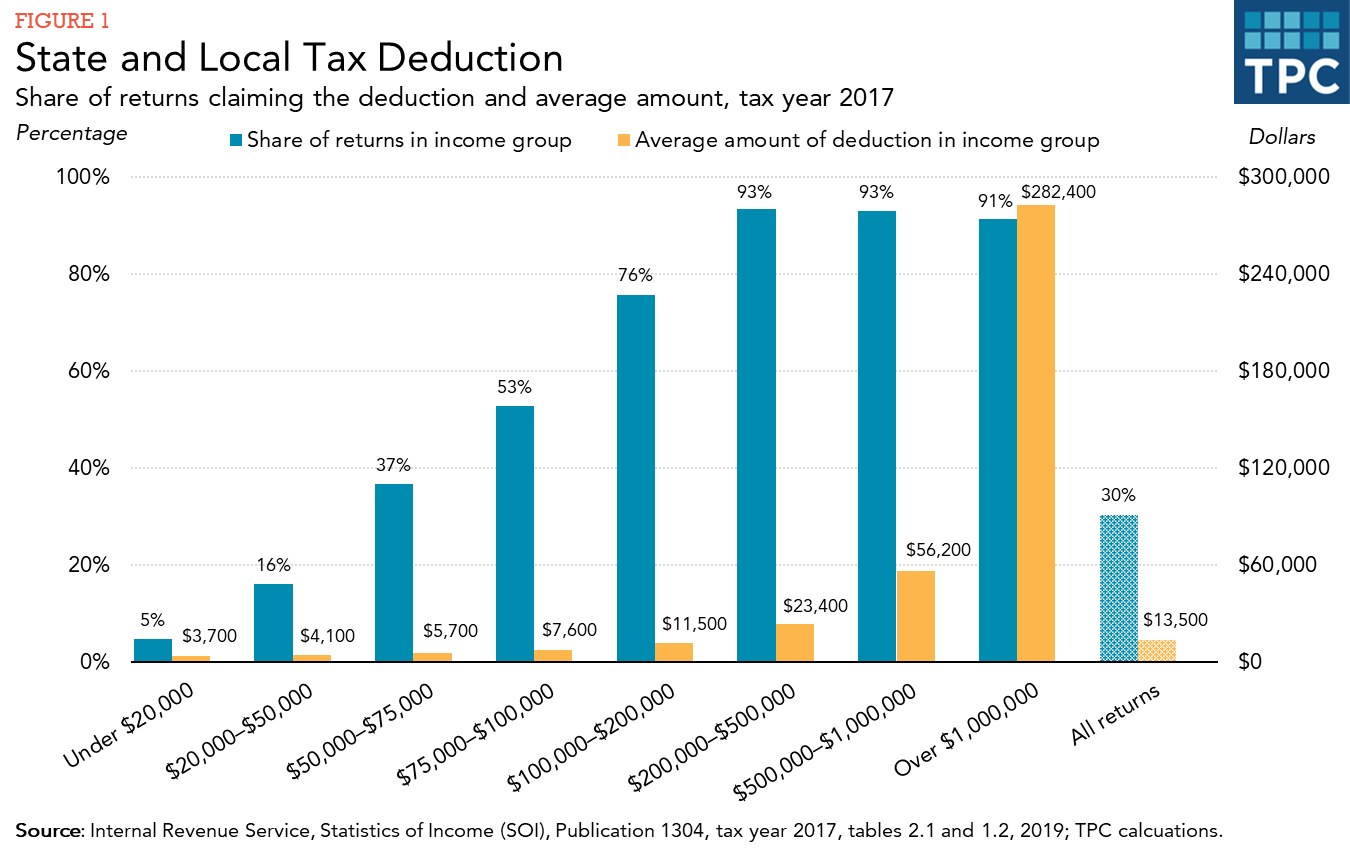

How Does The Deduction For State And Local Taxes Work Tax Policy Center

Smeinfo Understanding Tax

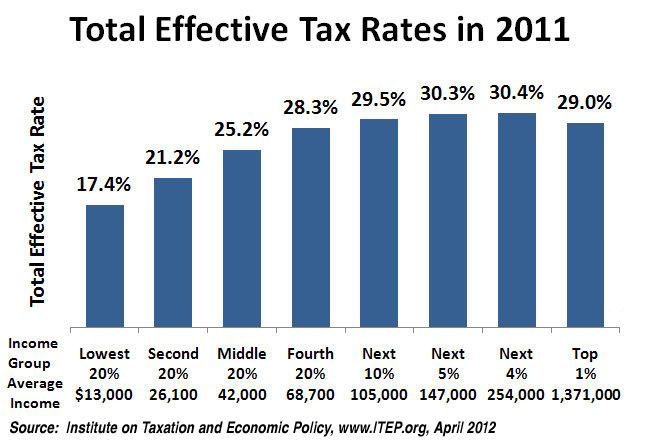

Progressive Proportional And Regressive Taxes Boundless Economics

Pin On Estate Planning

How The New Tax Law Changes Roth Ira Conversions Financial Planning

:max_bytes(150000):strip_icc()/TaxRates-marriedfilingseparately2-c08c527d8c98486d800ae561f3012d66.jpg)

What Tax Breaks Are Afforded To A Qualifying Widow

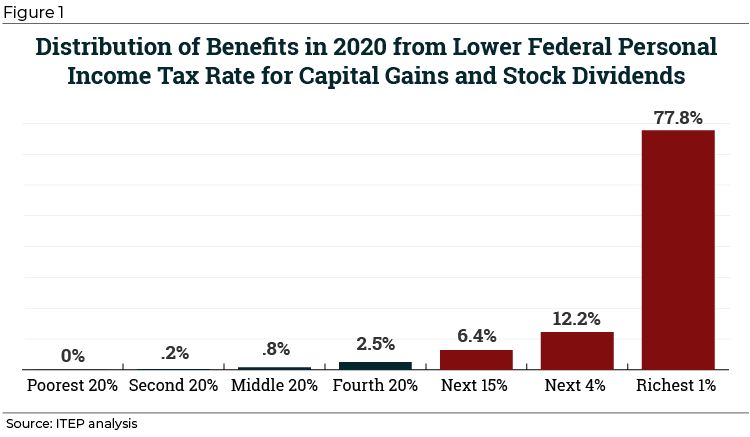

Congress Should Reduce Not Expand Tax Breaks For Capital Gains Itep

How Is Tax Liability Calculated Common Tax Questions Answered

Tax Solution Tax Return Us Tax Tax

Preparing For 2019 Malaysian Tax Season Ssm Certified Mbrs Training

Image Explaining Duties Of An Executor For Taxation Probate Infographic Duties

Switzerland S Tax Rates A Complete Guide For Expats Expatica