Income Tax Rates For Trusts And Estates 2018

New Federal Income Tax Rates 2018 Mortgage Interest Rates Pay Off Mortgage Early Mortgage Payoff

How The New Tax Law Changes Roth Ira Conversions Financial Planning

Latest Tds Rates Chart For Fy 2017 18 Ay 2018 19 Income Tax Income Tax Return Income Tax Preparation

How The New Tax Law Changes Roth Ira Conversions Financial Planning

Grat Gratification How One Business Owner Achieves Substantial Estate Tax Savings With A Grantor Retained Annuity Trust Http Estate Tax Business Owner Annuity

Trust Me There Is No Better Way Than To Do Tax Filing With Spectrum A Completed Tax Compliance Software 360 Sol Tax Software Filing Taxes Income Tax Return

New tax brackets for trusts and estates.

Income tax rates for trusts and estates 2018. Unless revised by future legislation the rates and brackets will revert back to 2017 levels after 2025. Income may become remittable if for example exchange controls are lifted. 2018 federal income tax rates. Estate and trusts not liable to pay tax at the trust rate tfn15.

For 2018 2019 taxable income attributable to net unearned income is taxed according to the brackets applicable for trusts and estates. Posted on january 6th 2018. Taxpayers can elect to apply the change to 2018 and 2019. Inflation adjustments will be made to these amounts for 2019 2025 based on chained cpi.

The tax rates which are shown below are to be used for taxable years beginning after december 31 2018 and through 2025. For 2020 this income is taxed at the parent s marginal tax rate. A comparison of. Treated as arising in the 2017 to 2018 tax year.

However new tax rates in place for 2018 will lower the tax rate on income over 12 500 to 37 down from 39 6 the year prior. Tax rates and income levels for trusts and estates remain virtually unchanged for irs filings for 2017. You shouldn t include this income in the trust and estate tax return. Rate reduction and thresholds.

Trust tax rates the united states tax rates and brackets for trusts and estates continue to change. These tax tables are designed for trusts and estates filing a 2018 income tax return. By joel roettger apr 17 2018 estate planning tax trusts. The law provides for tax years 2018 through 2025 a new table under sec.

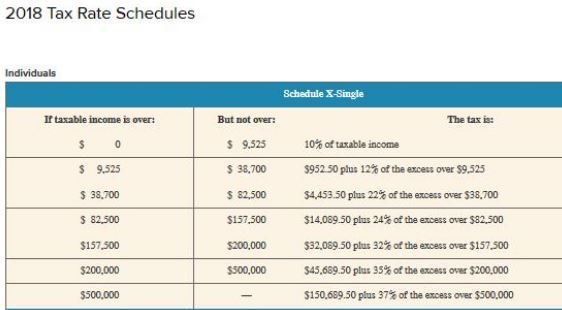

1 j 2 e of ordinary income tax rates and thresholds for trusts and estates subject to adjustment for inflation for years after 2018 as shown in the chart below. A table showing the 2018 federal marginal income tax rates for estates and trusts under the tax cuts and jobs act. Below are the new tax brackets and tax rates for individuals estates and trusts for 2018 under the new tax reform that are reflected in the tax jobs and cuts act. The brackets 10 percent 24 percent 35 percent and 37 percent are still extremely compressed with the top rate applying at 12 500 of taxable income.

Learn The Difference Between A Will A Revocable Trust And An Irrevocable Trust Download Our Free Guide To Learn If A Revocable Trust Trust Engagement Letter

Latest Income Tax Slab Rates Fy 2018 19 Ay 2019 20 Basunivesh

Trust Tax Rates Atotaxrates Info

Solved Henrich Is A Single Taxpayer In 2018 His Taxable Chegg Com

14 Tax Changes For Hedge Funds And Private Equity Under The Trump Tax Reform Trump Taxes Private Equity Equity

Pin On Testbank

Pin On Benang

Preparing For 2019 Malaysian Tax Season Ssm Certified Mbrs Training

2018 S Guide To Investment Property Research At Your Fingertips Investment Property Investing Real Estate Classes

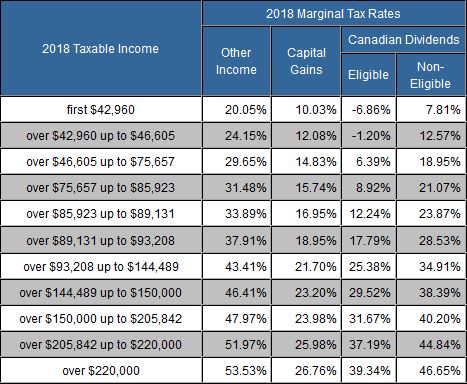

Taxtips Ca Ontario 2017 2018 Income Tax Rates

Https Www Money Education Com Images Jfd 2019 Annual Updates 2019 Annual Estates Update Pdf

How The Tcja Tax Law Affects Your Personal Finances

If You Have Any Questions About The New Tax Forms Or Need Assistance Preparing And Filing Your Tax Return Help Is J In 2020 Accounting Services Tax Forms Tax Services