Presentation Of Bad Debt Expense On Income Statement

Bad Debt Overview Example Bad Debt Expense Journal Entries

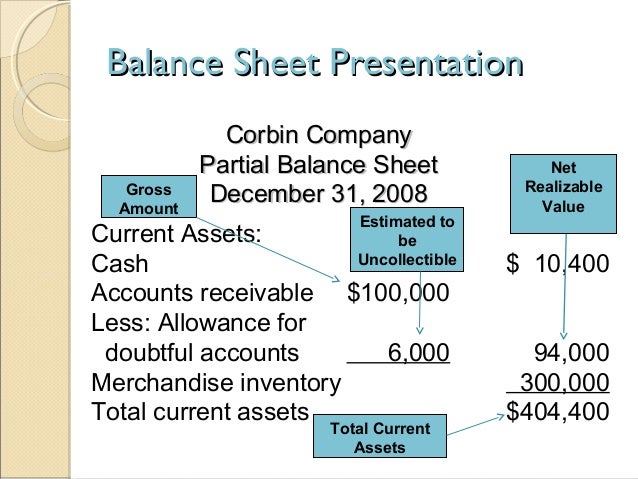

Multiple Step Income Statement Accountingcoach

Financial Statement Editable Powerpoint Template Financial Statement Financial Statement Analysis Statement Template

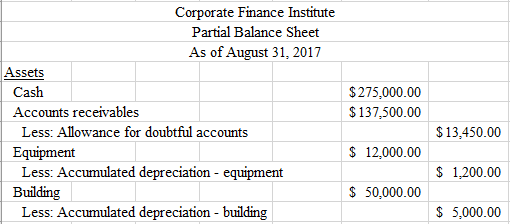

7 2 Accounting For Uncollectible Accounts Financial Accounting

Income Statement Template 7 Income Statement Statement Template Financial Statement

Bad Debts

Bad debts are inherently included in operating activities.

Presentation of bad debt expense on income statement. The bad debt expense appears in a line item in the income statement within the operating expenses section in the lower half of the statement. Because the bad debt is no longer an asset you adjust the value of your accounts receivable to reflect the loss of that asset. Understanding bad debt expense bad debt expenses are generally classified as a sales and general administrative expense and are found on the income statement recognizing bad debts leads to an. Look at a cash flow statement and notice net income is the very first item listed in operating activities.

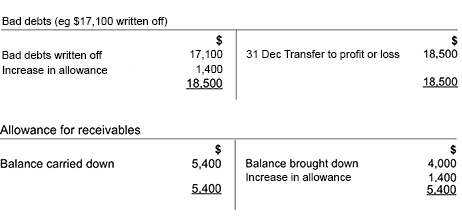

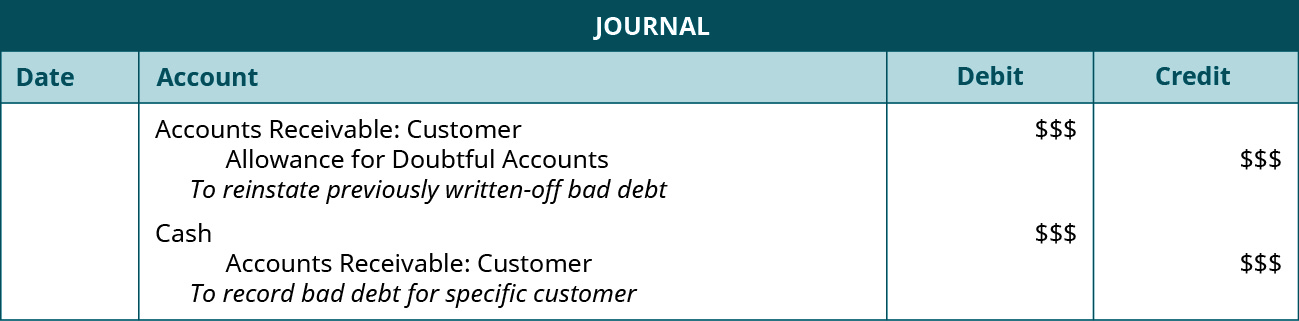

Some companies identify the specific customers whose accounts are bad debts and calculate the bad debt expense each accounting period based on customers accounts. Bad debt expense related to this revenue is presented in the financial statements as an operating expense. 5 1 allowance for doubtful accounts 700 accounts receivable broghan 700 to write off broghan company receivable and record bad debt expense. This presentation affects the comparability of revenue from one healthcare provider to another.

You can record bad debts in a couple of ways. As an example of the allowance method abc international records 1 000 000 of credit sales in the most recent month. As your company uses up or spends down its bad debt reserve the release of that liability flows through your income. Busi 1310 chapter 8 handout example two 2a prepare the journal entries for these two transactions using the allowance method.

Net income effect you would also charge 2 000 to bad debt expense which appears on your income statement. Net income includes bad debt a non cash. Continued on page 2. It should be noted that bad debts do however form part of the calculation of cash generated from operations when using the indirect cash flow statement which is the preferred method in the us.

Accounts receivable aging method. Determined that a receivable from broghan company for 700 would not be collectible. This method is based on an evaluation of the collectibility of accounts receivable.

Best Photos Of Income Statement Template Pdf Business Multiple Step Format Multi Bad Debt Expense 3 Golagoon

Profit And Loss Statement For Private Practice Profit And Loss Statement Business Tax Deductions Bookkeeping Business

Income Statement Template Free Word Templates Income Statement Personal Financial Statement Statement Template

Calculating Bad Debt Expense And Allowance For Doubtful Accounts Bad Debt Accounting Cpa Exam

Image Result For Financial Reports Templates Statement Template Financial Statement Report Template

Adjustments To Financial Statements Students Acca Global Acca Global

Accounting For Accruals Advanced Topics Receivables And Payables Ppt Download

Debit And Credit Cheat Sheet Rules For Debit Credit Accounting Basics Small Business Bookkeeping Bookkeeping Business

Image Result For Pretty Financial Reporting Templates Statement Template Profit And Loss Statement Income Statement

Financial Analysis Quick Ratio 22 000 41 500 Ppt Download

Image Result For Blank Income Statement Statement Template Income Statement Financial Statement

Account For Uncollectible Accounts Using The Balance Sheet And Income Statement Approaches Principles Of Accounting Volume 1 Financial Accounting

5 Types Of Financial Statements Balance Sheet Income Cash Flow 2 Bookkeeping Business Financial Statement Financial Accounting