Zimbabwe Income Tax Law

What You Need To Know About Payroll In Zimbabwe

Angola Amends Industrial And Personal Income Tax Codes Furtherafrica

Africa Tax In Brief 18 Feb 2020 Lexology

An Assessment Of The Administrative Capacity Of The Zimbabwe Revenue Authority To Deliver The Envisaged Benefits Of The New Income Tax Bill Semantic Scholar

Un Income Tax

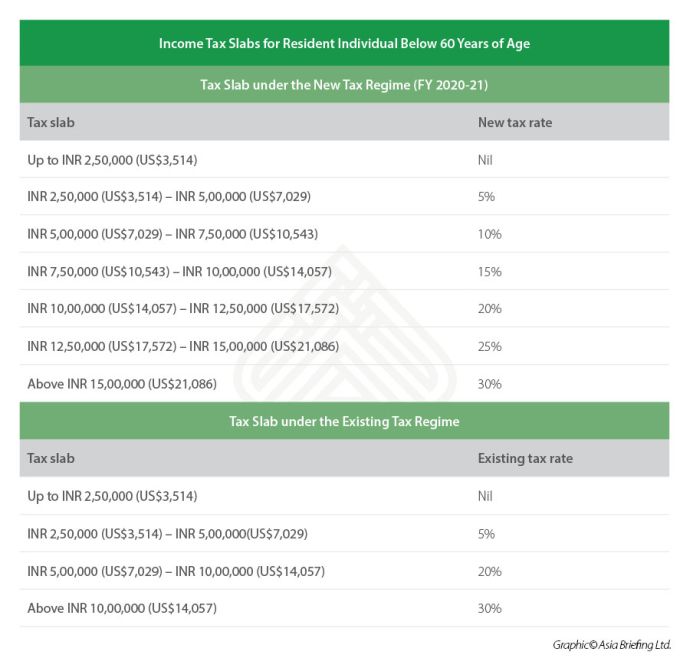

India S New Income Tax Plan Proposed Under Budget 2020 Tax India

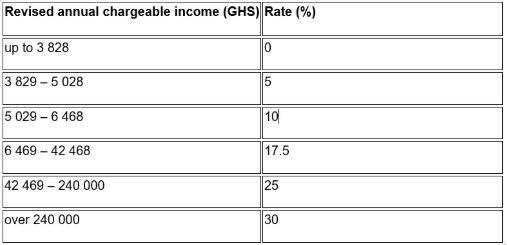

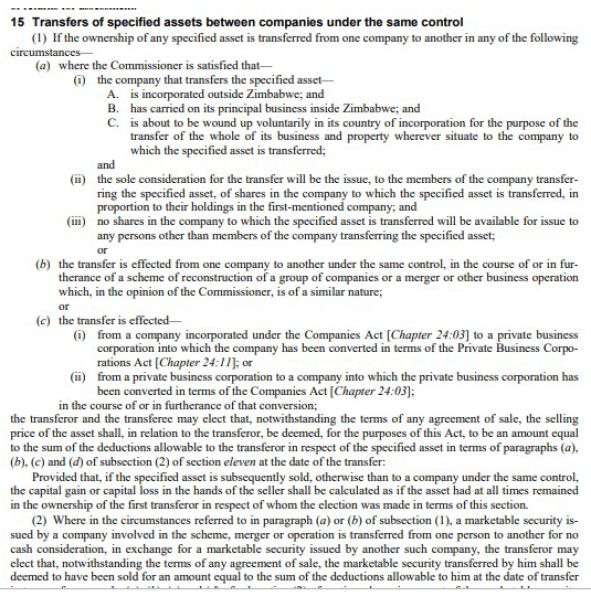

Income tax law the administration of income tax is governed by the income tax act of zimbabwe chapter 23 06 which guides on how income tax will be levied how it is calculated and other legislative guidelines.

Zimbabwe income tax law. Yes investment income is taxable at an effective rate of 25 75 percent being 25 percent plus 3 percent aids levy while capital gains on specified assets are taxable at 20 percent. Zimbabwe has thin capitalisation rules based on a 3 1 debt to equity ratio. Section 63 of the act squarely cast the burden of proof on the appellant and not on the commissioner. The 3 aids levy is also imposed.

Exempt income is also spelt out. The zimbabwean tax system is currently based on source and not on residency. In addition any disallowed interest will be treated as a deemed dividend and subjected to a 15 wht. Its sources and what could be deemed as a source of income including employment benefits.

Income tax is levied on earnings income of an individual or a business. This book looks at the tax law and practice in zimbabwe. It identifies what constitutes gross income. It also differentiates between capital receipts and revenue receipts in its bid to identify gross income.

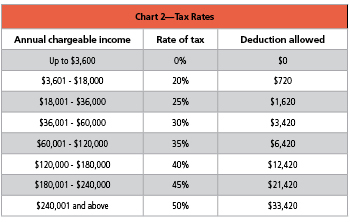

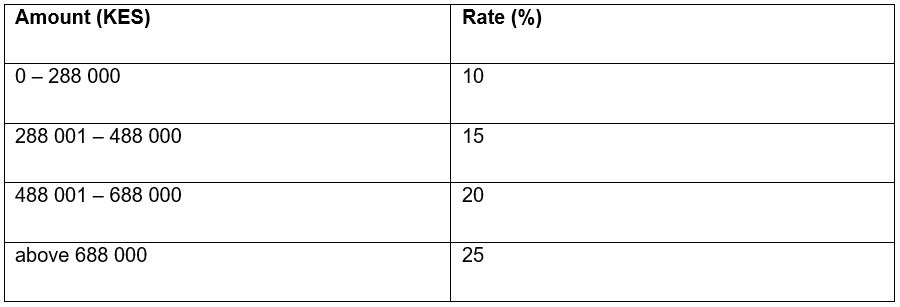

Compensation for services rendered in zimbabwe is deemed to be derived from a zimbabwean source regardless of where the payment is made or where the payer resides. Income tax rates deduction 0 1 980 00 0. Iii no amount in respect of the contribution is allowed as a deduction in terms of any law imposing a tax on income which is in force in a country other than zimbabwe. I the amount of any arrear contributions which are paid by the taxpayer in respect of past service with his employer to a pension fund other than a retirement annuity fund or to the consolidated revenue fund and which.

Income derived or deemed to be derived from sources within zimbabwe is subject to tax. It has been indicated that zimbabwe is considering moving to a residence based system during the current tax reform exercise. A portion of the overall interest may be disallowed if this ratio is exceeded.

How To Calculate Income Tax Tax Calculations Explained With Example By Yadnya Youtube

Income Tax Amendments The Tax Laws Amendment Act 2020

Pin On Janu Ardy Books Pdf

Income Tax 12 Changes That Kick In Today Heres Our Tax Calculator To Help You Out Community Reinvestment Act Tax Day Regulatory

Now Reach Over And Grab Your Cell Phone Look For A Cook County Property Tax Appeal Attorney And Get A Consultatio Things To Sell Property Tax Financial

Income Tax Liabilities For Mainland Chinese Employees In Hong Kong What Employers Need To Do Eca International

Capital Gains Tax Tax Zimbabwe

Dentons Global Tax Guide To Doing Business In Zimbabwe

Africa Tax In Brief 19 May 2020 Lexology

Liicornell Thanks For Being The Wikipedia Of Laws Knowledge Is Power Standuprepublic Mldschool Nvcopblock Definitions Knowledge Is Power Knowledge

Canada Global Payroll And Tax Information Guide Payslip

Talent Magnifier Offers E Accounts Finance E Gst With Income Tax Training In Delhi Training Courses Portfolio Management Corporate Training

Latest News Tax Return 2019 Salt Deduction Cap Middle Class Homeowners Hit By The New Tax Law This Is Going To Wipe Us Property Tax Tax Deadline Tax Return