Key Features Of Statement Of Comprehensive Income

Statement Of Comprehensive Income Overview Components And Uses

Statement Of Comprehensive Income Explained Accountingcoach

The Elements Of An Income Statement Dummies

Statement Of Comprehensive Income Format Examples

Basic Element Of The Income Statement In Financial Reporting And Analysis Tutorial 21 November 2020 Learn Basic Element Of The Income Statement In Financial Reporting And Analysis Tutorial 12490 Wisdom Jobs India

:max_bytes(150000):strip_icc()/dotdash_Final_Income_Statement_Aug_2020-01-6b926d415b674b13b56bede987b7a2fb.jpg)

Income Statement Definition

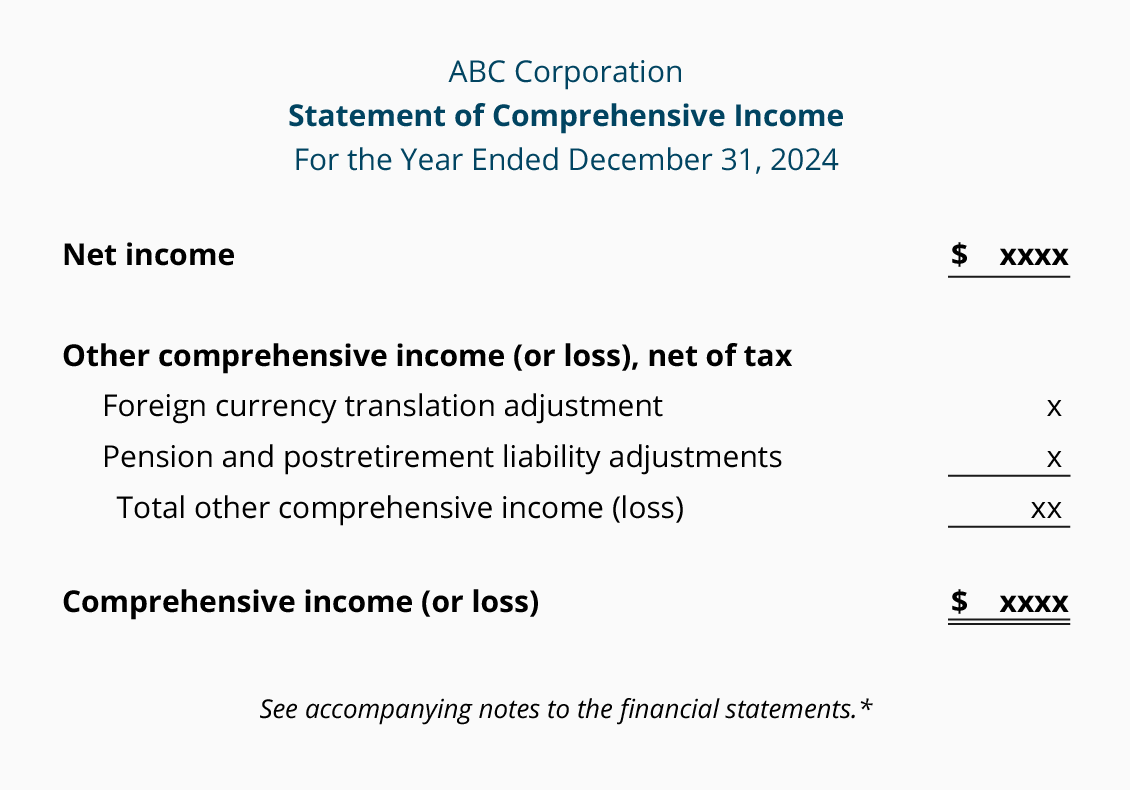

Statement of comprehensive income.

Key features of statement of comprehensive income. Other comprehensive income does not include changes relating to ownership such as dividends paid to shareholders new shares issued or share buy backs. Items recognized directly to equity or reserves such as changes in revaluation surplus gains or losses from subsequent measurement of available for sale financial. Comprehensive income includes a net income and b other comprehensive income. Notice that we report net income that occurs in the current reporting period in the income statement and also report accumulated net income that hasn t been distributed as dividends in the balance sheet as retained earnings.

The main example is the revaluation of tangible assets. The statement of comprehensive income. Statement of comprehensive income. The net income net income net income is a key line item not only in the income statement but in all three core financial statements.

The reason for this is that some gains the business makes during the year are not realised gains. The statement of comprehensive income has 2 basic elements. Whenever ci is listed on the balance sheet the statement of comprehensive income must be included in the general purpose financial statements to give external users details about how ci is computed. A statement of comprehensive income that begins with profit or loss bottom line of the income statement and displays the items of other comprehensive income for the reporting period ias 1 p 81 so the statement of comprehensive income aggregates income statement profit and loss statement and other comprehensive income which isn t.

This is simply an extension of the income statement. While it is arrived at through the income statement the net profit is also used in both the balance sheet and the cash flow statement. The gain is not realised until the asset is sold and converted into cash. A statement of comprehensive income contains two main things.

One of the most important financial statements is the income statement. Profit or loss for the period. A standard ci statement is usually attached to the bottom of the income statement and includes a separate heading. A statement of comprehensive income is a financial statement that includes both standard income and other comprehensive income.

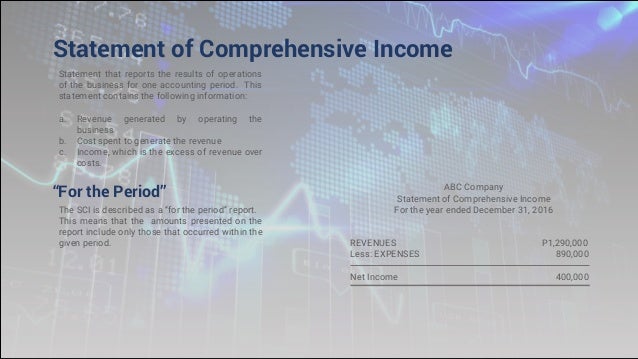

A statement of comprehensive income is the overall income statement that consolidates standard income statement which gives details about the repetitive operations of the company and other comprehensive income which gives details about the non operational transactions such as the sale of assets patents etc. Other comprehensive income. It provides an overview of revenues and expenses including taxes and interest.

How To Prepare An Income Statement A Simple 10 Step Business Guide

Single Step Income Statement Advantages Disadvantages Example

Single Step Vs Multi Step Income Statement Key Differences For Small Business Accounting

The Income Statement Boundless Accounting

Fundamentals Of Abm2 Statement Of Comprehensive Income Abm Specialize

Financial Statements As At 31 12 18

Statement Of Comprehensive Income Vs Income Statement Legalzoom Com

A Beginner S Guide To Vertical Analysis In 2020 The Blueprint

Fundamentals Of Abm2 Statement Of Comprehensive Income Abm Specialize

Http Xbrlsite Azurewebsites Net 2019 Core Core Sfac6 Documentation Pdf

Ias 1 Presentation Of Financial Statements

Chapter 2 Statement Of Financial Position And Income Statement

Prepaid Expenses Definition Example Financial Edge Training