Income Statement By Function Depreciation

Depreciation Turns Capital Expenditures Into Expenses Over Time Income Statement Income Financial Statement

Income Statement Components Under Ias 1 Income Statement Personal Financial Statement Financial Statement

Sample Financial Statement Analysis Example In 2020 Financial Statement Analysis Financial Statement Financial

Financial Statement Analysis Street Of Walls

:max_bytes(150000):strip_icc()/JCPIncomestatementMay2019Investopedia-ef93846733094d2cbd1fdfe97126b3bc.jpg)

Are Depreciation And Amortization Included In Gross Profit

Pin On Wordpdf Formats

An income statement by nature method is the one in which expenses are disclosed according to their nature such as depreciation transports costs rent expense wages and salaries etc.

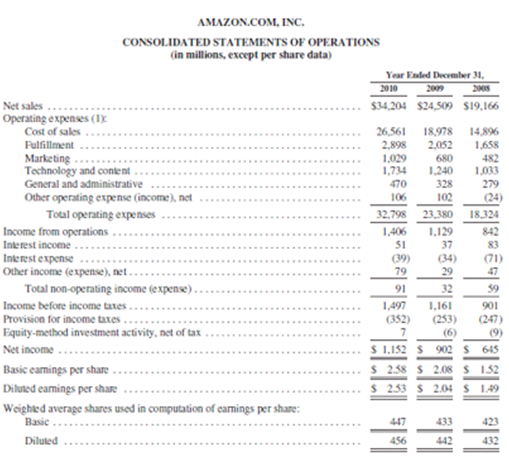

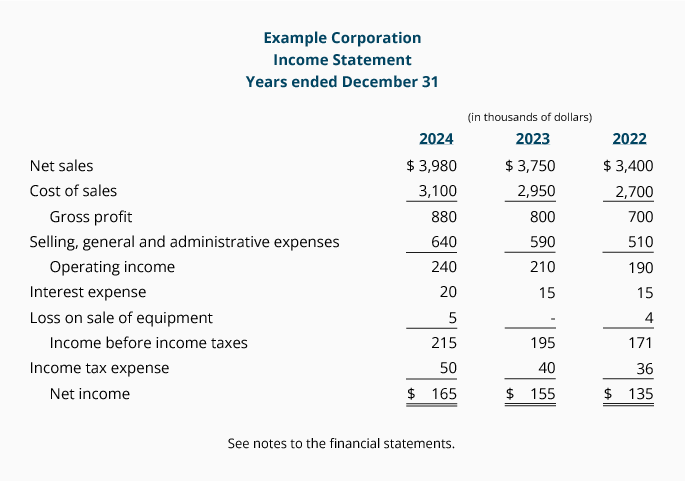

Income statement by function depreciation. The income statement reports all the revenues costs of goods sold and expenses for a firm. The following example shows the format of an income statement by function of expense. Depreciation of the equipment and building used in the manufacturer s selling and general administrative functions. It is accounted for when companies record the loss in value of their fixed assets through depreciation.

This expense is most common in firms with copious amounts of fixed assets. Depreciation is a non cash expense and serves as a tax shelter so it is shown on the income statement. Or a nonprofit entity that reports expenses by function could do so by aggregating its expenses into the following general functions. This depreciation will be reported on the manufacturer s income statement in the section containing its sg a expenses.

After subtracting selling and administrative expenses and depreciation you arrive at the operating profit. For example the depreciation on the sales staff motor van is considered part of the company s selling expense. The expenses in an income statement are either classified by their nature or by their function. One expense reported here relates to depreciation.

Examples of income statement line items that are presented by function are. In this research work titled the effect of depreciation on the income statement of with particular reference to united bank for africa uba plc. The effect of depreciation on income statement reporting a study of united bank for africa uba plc enugu branch abstract. The depreciation will be reported on the retailer s income statement in the section containing its sg a expenses.

The use of function method to disclose expenses still requires us to disclose the individual expenses by nature method under each function either on the face of the income statement or in the notes to the income statement. Depreciation can be a selling expense administration expense distribution costs and part of the cost of production. Physical assets such as machines equipment or vehicles degrade over time and reduce in value incrementally. Where depreciation is reported depends on the assets being depreciated.

Income Statement Pdf Editable Premium Printable Templates Home Title Income Statement Profit And Loss Statement Financial Statement

Profit And Loss Income Statement Excel Business Insights Group Ag In 2020 Income Statement Profit And Loss Statement Financial Statement

The Income Statement Boundless Accounting

Financial Statement Editable Powerpoint Template Financial Statement Statement Template Financial Statement Analysis

Ytd Profit And Loss Statement Template Income Statement Statement Template Personal Financial Statement

Projected Income Statement Template Beautiful Excel In E Statement 7 Free Excel Documents Downloa In 2020 Statement Template Income Statement Profit And Loss Statement

Multiple Step Income Statement Accountingcoach

Indirect Cash Flow Method Description Cash Flow Cash Flow Statement Flow

Monthly Profit And Loss Statement Template Google Search Profit And Loss Statement Statement Template Income Statement

Income Statement Present By Nature Wikiaccounting

:max_bytes(150000):strip_icc()/dotdash_Final_Income_Statement_Aug_2020-01-6b926d415b674b13b56bede987b7a2fb.jpg)

Income Statement Definition

Balance Sheet For A Small Business In 2020 Balance Sheet Template Balance Sheet Balance

Simplified Income Statement Template Unique In E Statement Template 25 Free Word Excel Pdf In 2020 Income Statement Statement Template Mission Statement Template