A Partnership Financial Statement Showing Net Income Or Loss Distribution To Partners

Financial Statement Template Ifrs Ten Ways On How To Prepare For Financial Statement Templat Income Statement Personal Financial Statement Financial Statement

2019 Marriage Visa Income Requirements For The Sponsoring Spouse Boundless Immigration Income Statement Profit And Loss Statement Statement Template

Distribution Of Profit In Partnership Explanation Examples Play Accounting

Profit And Loss Appropriation Account In 2020 Accounting Accounting And Finance Profit

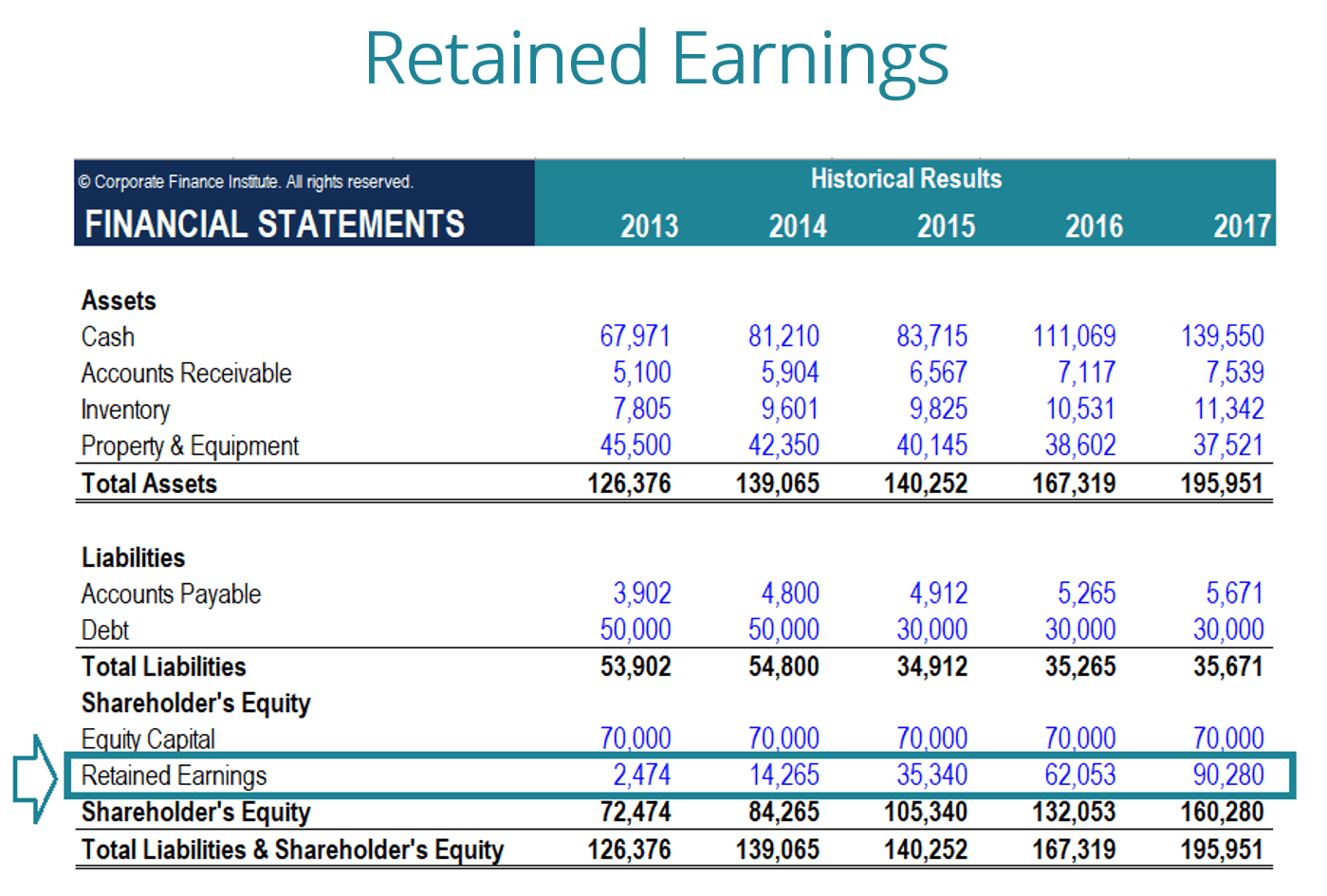

What Are Retained Earnings Guide Formula And Examples

:max_bytes(150000):strip_icc()/AppleIncomeSattementDec2019-cd967d0a8f5e4748a1060f83a7e7acbc.jpg)

Net Income After Taxes Niat

A partnership agreement may allow some partners a specific salary in addition to their ultimate profit share.

A partnership financial statement showing net income or loss distribution to partners. Distribution of profit among partners source. If the net income of the partnership was 40 000 but partner b had a salary of 15 000 then the amount to be distributed equally would be 40 000 15 000 25 000 so each partner would receive 25 000 2 12 500. Net income earned by a partnership is distributed to partners in a number of forms which includes salaries interest on opening capital balances and or in the form of share in the remaining net income. There are three general approaches to income distribution.

As partners are the owners of the business they do not receive a salary but each has the right to withdraw assets up to the level of his her capital. They belong only in the division of profit statement section. Income statement the main part of the income statement is prepared exactly as for a sole trader. However certain adjustments such as interest on drawings capital salary commission.

Encrypted tbn0 gstatic in accordance with the provisions of the partnership deed the profits and losses made by the firm are distributed among the partners however sharing of profit and losses is equal among the partners if the partnership deed is silent. Preparing partnership financial statements. Equal allocation ratio based allocation and salary and capital based allocation. The partnership agreement should include how the net income or loss will be allocated to the partners.

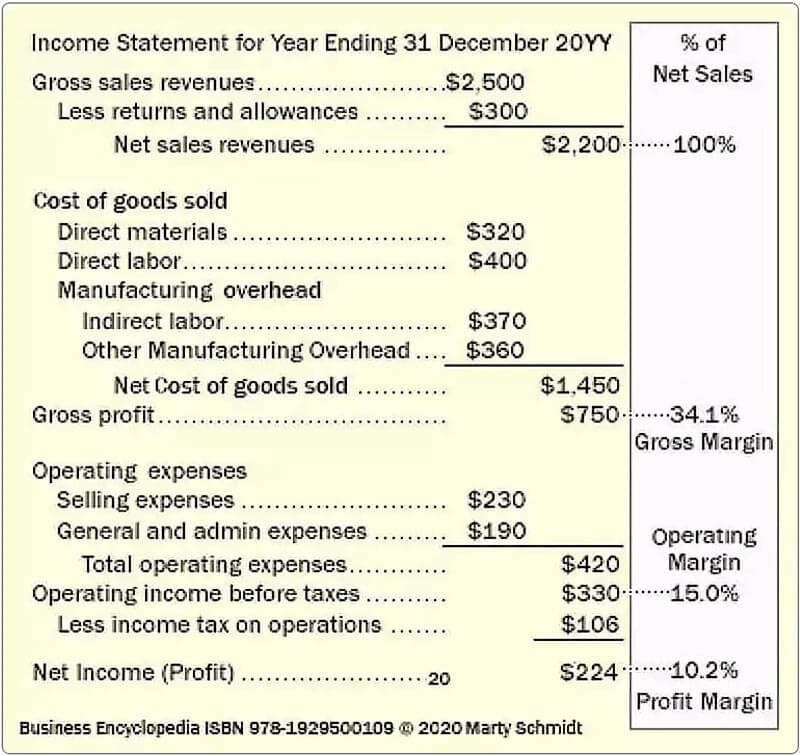

The income statement also called a profit and loss statement or p and l shows a business s income and expenses over a set period of time. Revenue and income are at the top and expenses are at the bottom followed by the business s net income calculation. If the agreement is silent the net income or loss is allocated equally to all partners. From here this net income is to be allocated to the partners.

Net income equals total revenue minus total expenses. The capital of partner a is reduced by the drawings of 5 000.

How To Read Income Statement Understand Structure And Contents

Debit And Credit Cheat Sheet Bookkeeping Basics Part 2 What Is Normal A Debit Or A Credit Accounting Basics Bookkeeping Accounting Classes

/dotdash_Final_What_Changes_in_Working_Capital_Impact_Cash_Flow_Sep_2020-01-13de858aa25b4c5389427b3f49bef9bc.jpg)

What Changes In Working Capital Impact Cash Flow

How Do Net Income And Operating Cash Flow Differ

Which Transactions Affect Retained Earnings

:max_bytes(150000):strip_icc()/dotdash_Final_Income_Statement_Aug_2020-02-23bef448b8aa4c9bac46c8e15b2b9f0a.jpg)

Income Statement Definition

:max_bytes(150000):strip_icc()/dotdash_Final_Gross_Profit_Operating_Profit_and_Net_Income_Oct_2020-01-55044f612e0649c481ff92a5ffff1b1b.jpg)

Gross Profit Operating Profit And Net Income

Operating Income Vs Net Income What S The Difference

Ts Grewal Solutions For Class 12 Accountancy Accounting For Partnership Firms Fundamentals With Images Solutions Fundamental Accounting

Ts Grewal Solutions Class 12 Accountancy Accounting Partnership Firms Fundamentals 42https Www Cbsetuts Com Ts Grewal Soluti Solutions Fundamental Accounting

The Common Size Analysis Of Financial Statements

:max_bytes(150000):strip_icc()/Howdogrossprofitandnetincomediffer2-962e065a0ae84e52b083fff305afaa96.png)

How Do Gross Profit And Net Income Differ

Pin On Customize Reports Templates Online