All Income Statement Accounts Will Be Closed At The End Of The Period

How To Read The Balance Sheet Understand B S Structure Content Financial Position Balance Sheet Financial Asset

How To Read The Balance Sheet Understand B S Structure Content Balance Sheet Financial Statement Balance

A Sample Income Statement For A Fake Company Accounting And Finance Bookkeeping Business Income Statement

How To Read Income Statement Understand Structure And Contents Income Statement Statement Income

Income Statement Template 7 Income Statement Statement Template Financial Statement

5 Free Income Statement Examples And Templates Income Statement Financial Statement Statement Template

:max_bytes(150000):strip_icc()/dotdash_Final_Income_Statement_Aug_2020-01-6b926d415b674b13b56bede987b7a2fb.jpg)

False assets liabilities and owner s capital are real accounts and do not get closed at the end of the period.

All income statement accounts will be closed at the end of the period. At the end of a company s fiscal year close all temporary accounts. Conversely permanent accounts accumulate balances on an ongoing basis through many fiscal years and so are not closed at the end of the fiscal year. Then the income summary account is closed to retained earnings a component of equity on the balance sheet. A temporary account is an account that is closed at the end of every accounting period to start a new period with a zero balance.

Assets liabilities and owner s capital are real accounts and do not get closed at the end of the period. Entries required to close the balances of the temporary accounts at the end of the period are called final entries f all income statement accounts will be closed at the end of the period. First all revenue and expense accounts are closed to an account called income summary. This reduces all income statement accounts to 0 so future periods can be accounted for with a clean slate.

True assets liabilities and owner s equity are permanent real accounts and do not get closed at the end of the period. T 17 at the end of the fiscal period prepaid expenses are reported on the income statement as expenses. The income summary account is also known as the clearing account. A closing entry is a journal entry made at the end of accounting periods that involves shifting data from temporary accounts on the income statement to permanent accounts on the balance sheet.

This is done in order to avoid a mix up of the balances between two or more accounting periods. 16 all income statement accounts will be closed at the end of the period. 1 true false 19. All income statement accounts will be closed at the end of the period true internal control is enhanced by separating the control of a transaction from the record keeping function.

Temporary accounts accumulate balances for a single fiscal year and are then emptied. All income statement accounts will be closed at the end of the period.

Statement Of Retained Earnings Definitions Use Example Explained Income Statement Statement Financial Statement

Income Statement Definition

Balance Sheet Example Template Format Balance Sheet Template Balance Sheet Accounting Basics

Sales Cost Of Goods Sold And Gross Profit Cost Of Goods Sold Cost Of Goods Cost Accounting

Accounting Competency Exam Sample Exam Answers Provided At The End In 2020 Accounting Process Accounting Financial Statement

Month End Closing Checklist Financial Statement Month End Income Statement

Multi Step Income Statement Template Inspirational Balance Sheet Vs In E Statement Difference An In 2020 Income Statement Statement Template Budget Template Excel Free

Financial Ratios Statement Of Cash Flows Accountingcoach In 2020 Cash Flow Statement Financial Ratio Financial Statement Analysis

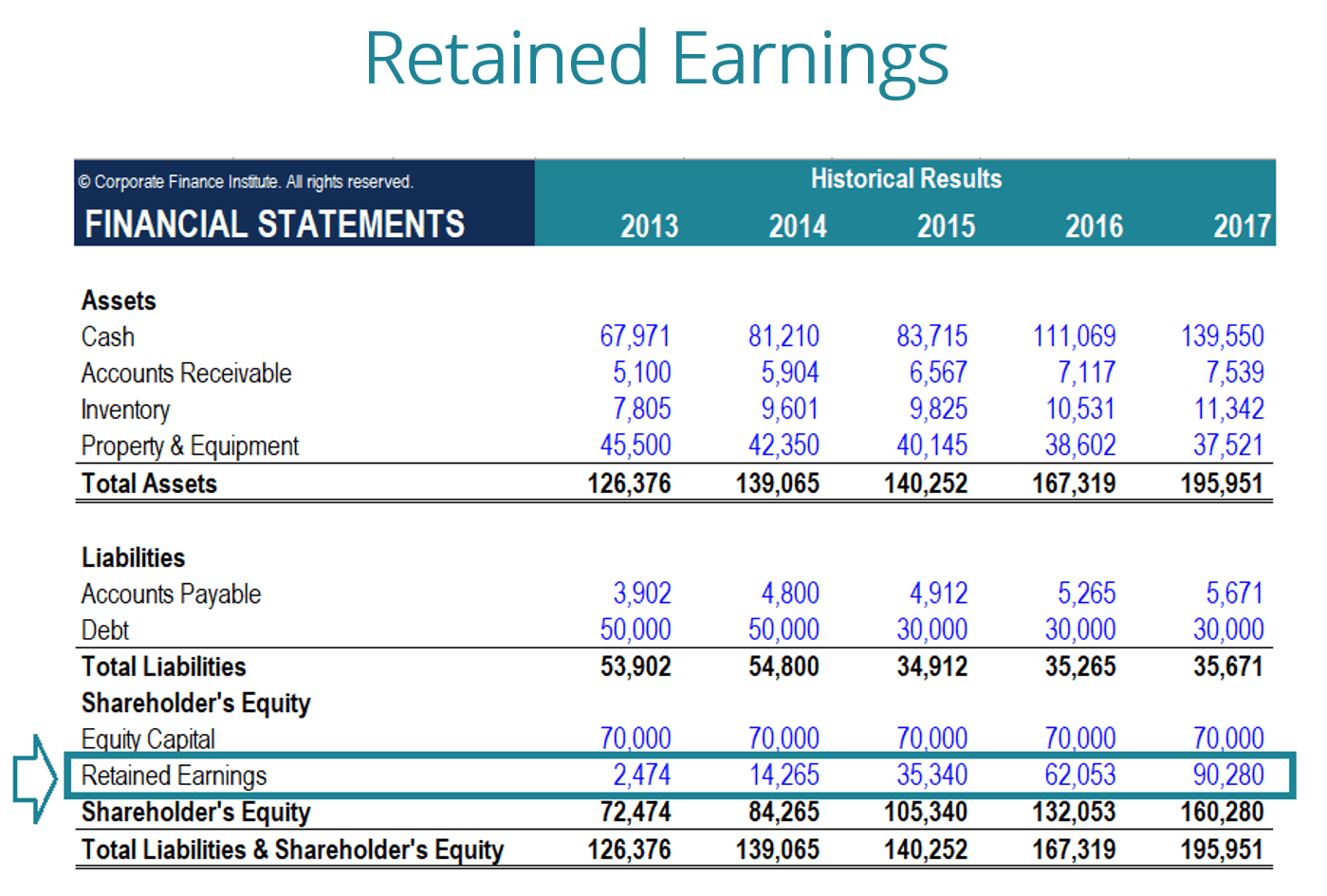

What Are Retained Earnings Guide Formula And Examples

Month End Closing Checklist Checklist Checklist Template Months

Depreciation Turns Capital Expenditures Into Expenses Over Time Income Statement Income Financial Statement

Order Of Preparing Financial Statements In 2020 Financial Statement Financial Statement

M 9f Closing Retained Earnings Earnings Accounting Income Statement