Comprehensive Income One Statement Approach

Statement Of Comprehensive Income Overview Components And Uses

Ca Accounting Books Approaches For Calculating Prepayments Accounting Books Accounting Approach

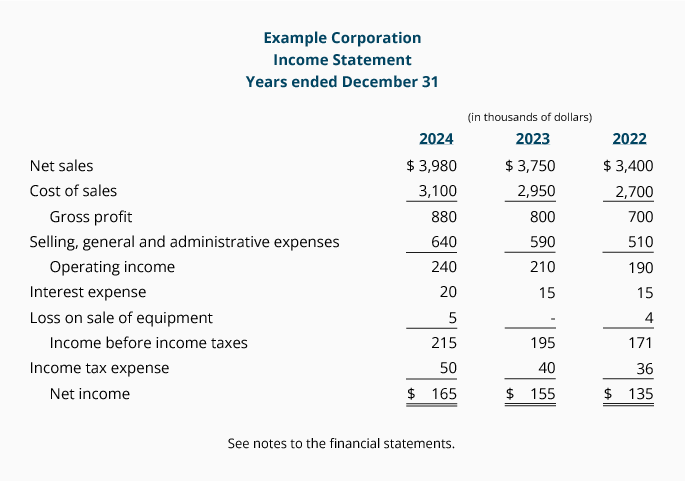

How To Prepare An Income Statement A Simple 10 Step Business Guide

Income Statements Explained Accountingcoach

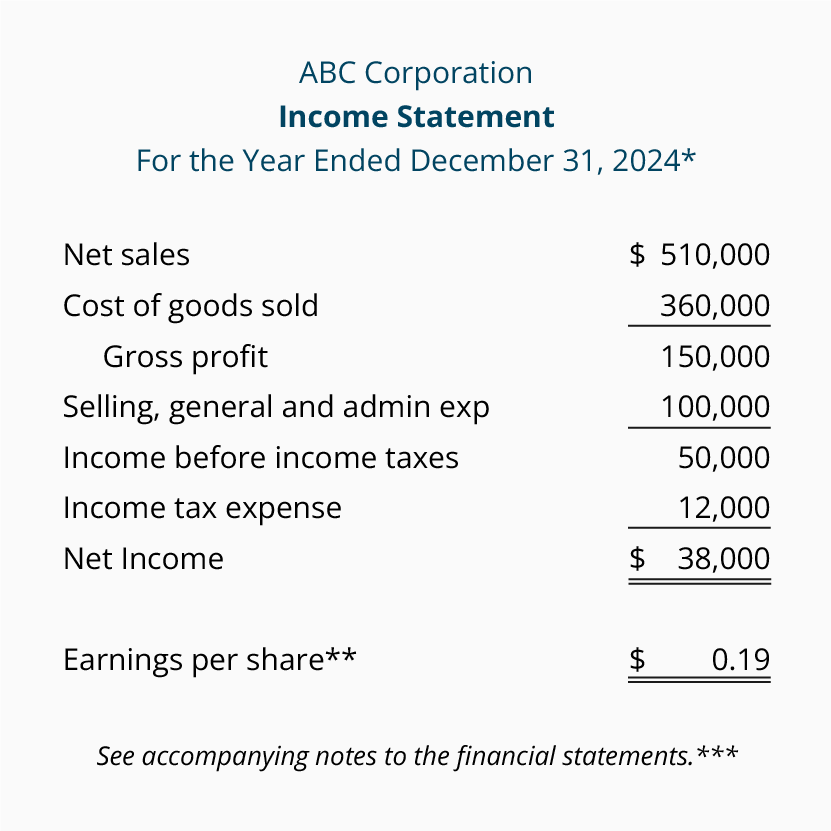

Multiple Step Income Statement Accountingcoach

:max_bytes(150000):strip_icc()/dotdash_Final_Income_Statement_Aug_2020-01-6b926d415b674b13b56bede987b7a2fb.jpg)

Income Statement Definition

In other words the statement highlights the adjustments on equity during a given timeframe.

Comprehensive income one statement approach. Provided the following statement of net income for the current year. Presented in a statement of comprehensive income which can be either a single statement or two statements where one is a separate income statement displaying components of profit and loss and the other is a statement of comprehensive income displaying components of other. Statement of comprehensive income refers to the statement which contains the details of the revenue income expenses or loss of the company that is not realized when a company prepares the financial statements of the accounting period and the same is presented after net income on the company s income statement. The company also had 735 of unrealized holding gains on its available for sale investment portfolio.

The statement of comprehensive income illustrates the financial performance and results of operations of a particular company or entity for a period of time. Comprehensive income includes all of the changes in equity during a period except those resulting from investments by owners and distributions to owners. All income is subject to a 40 income tax rate. The statement of comprehensive income provides a summary of a company s net assets over a given period of time.

All income is subject to a 40 income tax rate. In addition an entity has the choice of presenting the statement of comprehensive income using a one statement or a two statement approach. The question is whether the entity wishes to produce a single combined statement or two separate ones. Comprehensive income statement one statement approach.

True how is net income represented in the one statement approach. Comprehensive income statement one statement approach. Provided the following statement of net income for the current year. Comprehensive income is the change in equity net assets of a business enterprise during a period from transactions and other events and circumstances from non owner sources.

An entity shall present an analysis of expenses using a classification based on either the function or the nature of the expenses whichever provides information that is reliable and more relevant.

Single Step Income Statement Advantages Disadvantages Example

Single Step Vs Multi Step Income Statement Key Differences For Small Business Accounting

Statement Of Comprehensive Income Format Examples

Single Step Income Statement Definition Explanation Example And Template Pdf And Excel

Ca Accounting Books Approachs For Accrued Expenses Accounting Books Accrual Accounting Accounting

Spreadsheet Template Excel Monthly Cash Flow Template Excel Cash Cash Flow Statement Cash Flow Spreadsheet Template

The Due Diligence For Companies In India Enterslice Financial Checklist Diligence Risk Management

Opening Entry In Accounting Double Entry Bookkeeping Bookkeeping Accounting Cost Accounting

Etsy Seller No Tax Manual Income Expense Bookkeeping Etsy Bookkeeping Templates Small Business Bookkeeping Bookkeeping

Business Finance Laminated Reference Guide Trade Finance Finance Business Finance

Capability Statement Template Word Awesome 15 Capability Statement Templates Pdf Word Pages Statement Template Mission Statement Template Templates

Variable Costing Income Statement Examples How It Is Prepared

I Will Pay Someone To Do My Homework The First Place To Look For An Msds Msdssearch Is The Most Comprehensive Single Personal Statement Essay Examples Essay