Income Statement Gain On Disposal Of Assets

5 Free Income Statement Examples And Templates Income Statement Financial Statement Statement Template

04x Table 03 Income Statement Financial Statement Profit And Loss Statement

How To Put Together An Income Statement For Dummies Income Statement Profit And Loss Statement Sample Business Plan

When An Accountant Records A Sale Or Expense Entry Using Double Entry Accounting He Or She Sees The Inte Income Statement Accounting Jobs Accounting Education

Disposal Of Assets Sale Of Asset Accountingcoach

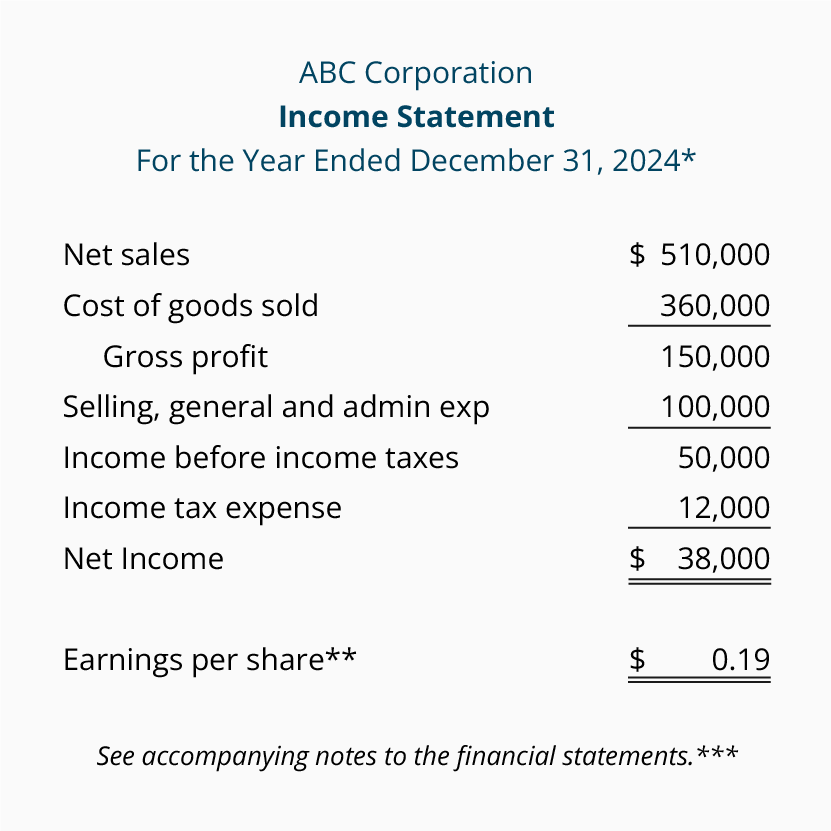

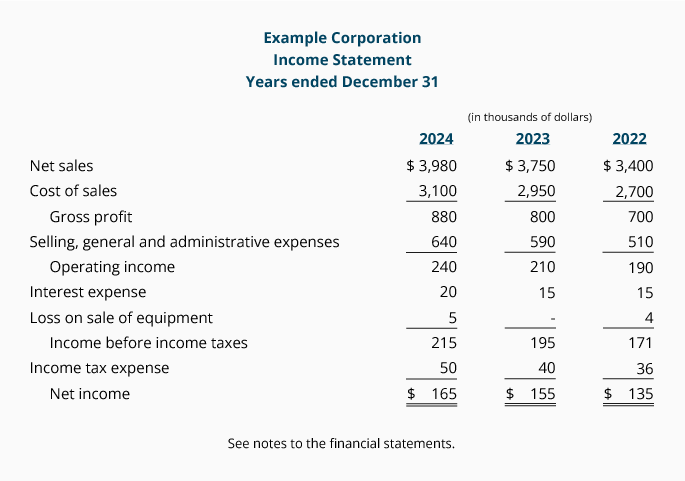

Income Statements Explained Accountingcoach

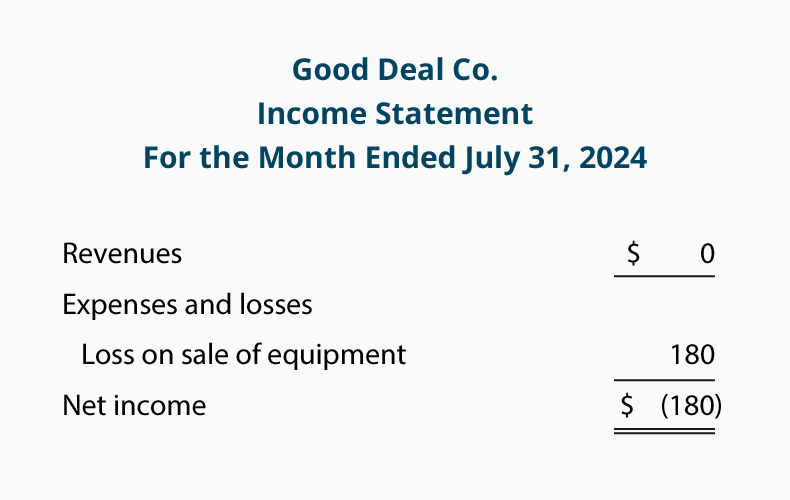

Asset sales require a separate entry on the income statement.

Income statement gain on disposal of assets. The gain from selling assets can be another income stream but mingling it with regular sales income is an accounting no no. The documentation of these cash flows is how the cash flow statement connects the income statement to the balance sheet. These three core statements are intricately it is an important concept because it primarily relates to the company s capital assets types of. To sell or on the disposal of the assets or disposal group s constituting the discontinued operation.

It also shows how your company s use or acquisition of assets liabilities and equity impact cash. Gains and losses from asset sales then go below operating profit on the income. For the purposes of this discussion we will assume that the asset being. Asset disposal is the removal of a long term asset from the company s accounting records three financial statements the three financial statements are the income statement the balance sheet and the statement of cash flows.

An involuntary conversion involving an exchange for monetary assets is accounted for the same way as a sales transaction with a gain or loss reported on the income statement. What is asset disposal. For example let s say a company sells one of its delivery trucks for 3 000. A disposal account is a gain or loss account that appears in the income statement and in which is recorded the difference between the disposal proceeds and the net carrying amount of the fixed asset being disposed of.

The disposal of assets involves eliminating assets from the accounting records this is needed to completely remove all traces of an asset from the balance sheet known as derecognition an asset disposal may require the recording of a gain or loss on the transaction in the reporting period when the disposal occurs. The cash flow statement shows the impact of your company s sales and profit generating or operating activities on its cash. The account is usually labeled gain loss on asset disposal the journal entry for such a transaction is to debit the disposal account for the net difference between the. When gains and losses are reported on an income statement they are generally separately disclosed because knowledge of them is useful for assessing future cash flows.

A gain or loss on disposal can result. The result is operating profit the profit the company made from doing whatever it is in business to do. If a company disposes of sells a long term asset for an amount different from the amount in the company s accounting records its book value an adjustment must be made to the net income shown as the first amount on the cash flow statement.

Methods For Preparing The Statement Of Cash Flows Cash Flow Cash Flow Statement Profit And Loss Statement

Pin On Cash Flow

How To Read Income Statement Understand Structure And Contents Income Statement Statement Income

Depreciation Turns Capital Expenditures Into Expenses Over Time Income Statement Income Financial Statement

Reporting Unusual Items Income Statement Accountingcoach

Pin On Educational Knowledge

Statement Of Retained Earnings Definitions Use Example Explained Income Statement Statement Financial Statement

How To Read The Balance Sheet Understand B S Structure Content Balance Sheet Financial Statement Balance

Income Statement Components Under Ias 1 Income Statement Personal Financial Statement Financial Statement

Income Statement Pdf Editable Premium Printable Templates Home Title In 2020 Income Statement Profit And Loss Statement Financial Statement

Plus One Accountancy Notes Chapter 8 Financial Statements I Financial Statements Ii A Plus Topper Financial Statement Investment Loss Financial

Pin On Financial Statements

The Income Statement Income Statement Sales And Marketing Statement