Other Comprehensive Income Financial Statement Presentation

Other Comprehensive Income Overview Examples How It Works

Statement Of Comprehensive Income Overview Components And Uses

Financial Statement Presentation You Are The Senio Chegg Com

Income Statement Definition Types Templates Examples And Importance Information Wikiaccounting

How Do Malaysian Ace Market Companies Report Comprehensive Income

Other Comprehensive Income Statement Example Explanation

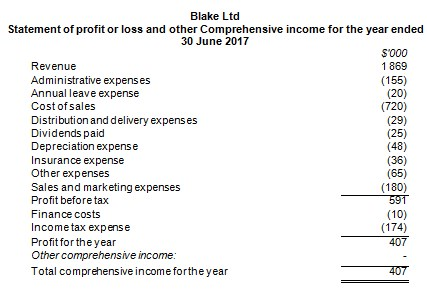

Revenues expenses gains and losses that are reported as other comprehensive income have not been realized yet.

Other comprehensive income financial statement presentation. Amended by presentation of items of other comprehensive income. But don t depend solely on it. Other comprehensive income is those revenues expenses gains and losses under both generally accepted accounting principles and international financial reporting standards that are excluded from net income on the income statement this means that they are instead listed after net income on the income statement. Definitions 7 the following terms are used in this standard with the meanings specified.

This project involves a proposal for a possible limited scope amendment to ias 1 presentation of financial statements that would require all entities to present a single statement of comprehensive income so removing the two statement approach separate statements of income and comprehensive income currently permitted by ias 1. Other reports and statements in the annual report such as a financial review an environmental report or a social report are outside the scope of ias 1. This project arose out of the comprehensive. In other words it adds additional detail to the balance sheet s equity section to show what events changed the stockholder s equity beyond the traditional.

Comprehensive income or in two statements a separate income statement and a statement of comprehensive income separately from owner changes in equity see paragraphs bc49 bc54 of the basis for conclusions. Other comprehensive income comprises revenues expenses gains and losses that according to the gaap and ifrs standards are excluded from net income on the income statement. Our financial reporting guide financial statement presentation details the financial statement presentation and disclosure requirements for common balance sheet and income statement accounts it also discusses the appropriate classification of transactions in the statement of cash flows and addresses the requirements related to the statements of stockholders equity and other comprehensive. Effective for annual periods beginning on or after 1 july 2012.

Comment deadline 30 september 2010. Amended by annual improvements 2009 2011 cycle comparative. Exposure draft ed 2010 5 presentation of items of other comprehensive income published. To adapt the financial statement presentation of members or unitholders interests.

A statement of comprehensive income is the overall income statement that consolidates standard income statement which gives details about the repetitive operations of the company and other comprehensive income which gives details about the non operational transactions such as the sale of assets patents etc. According to ias 1 presentation of financial statements a complete set of financial statements has the following components. Statement s of profit or loss and other comprehensive income statement of changes in equity and. See examples whats included.

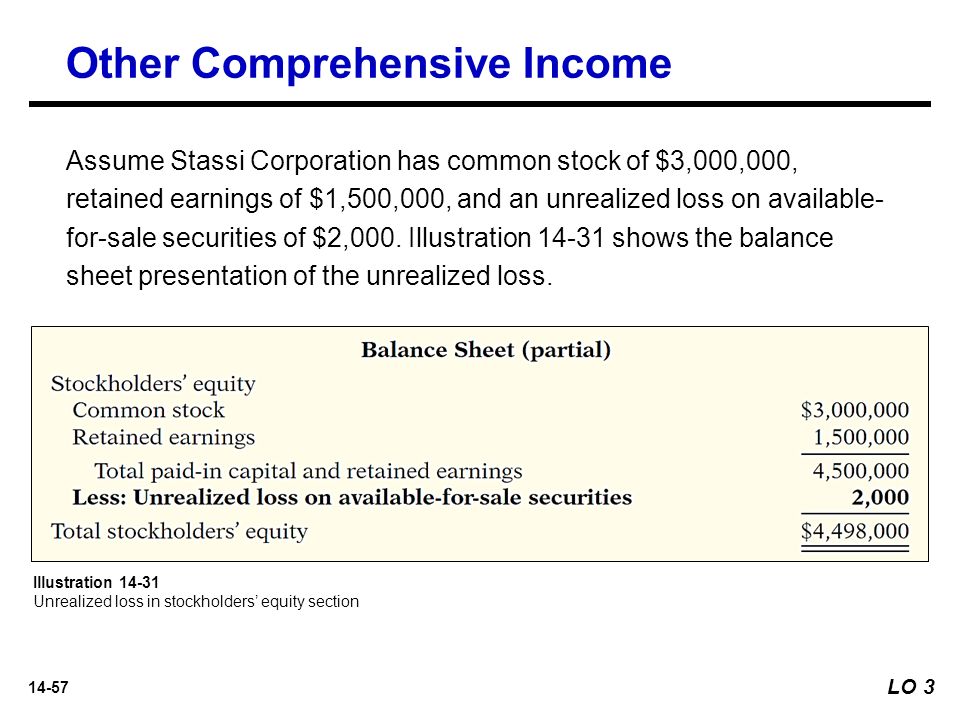

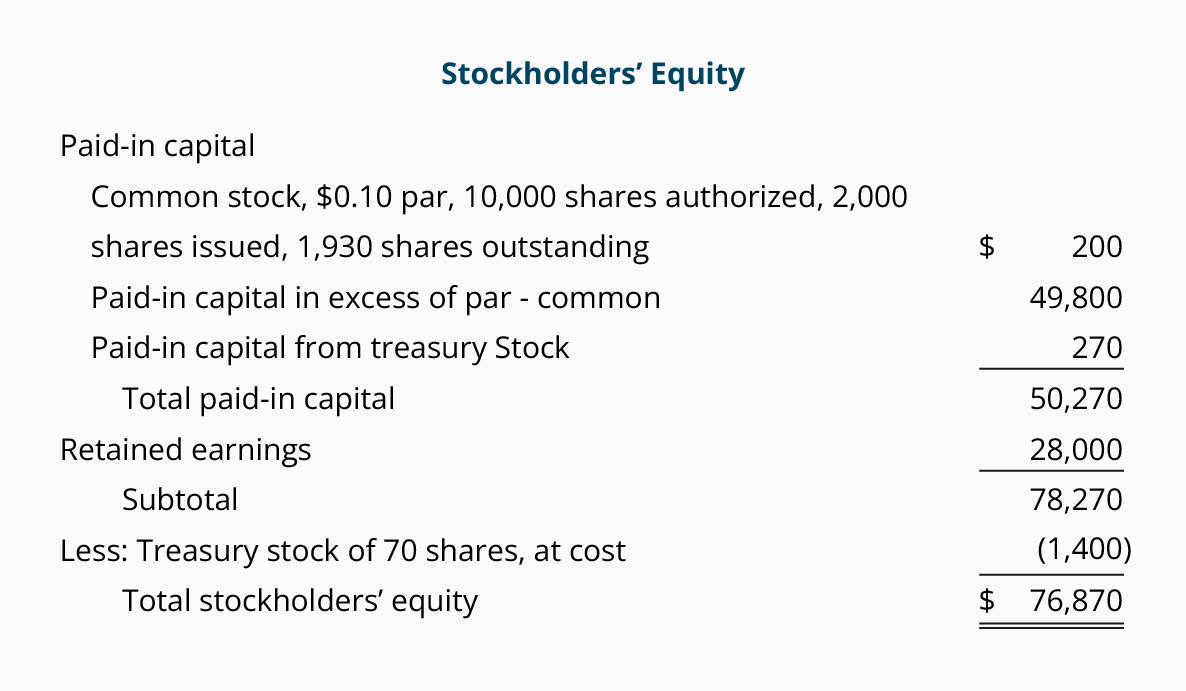

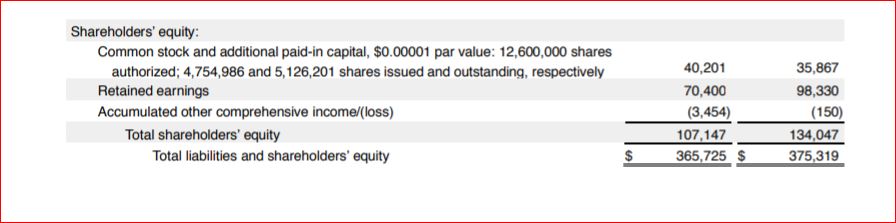

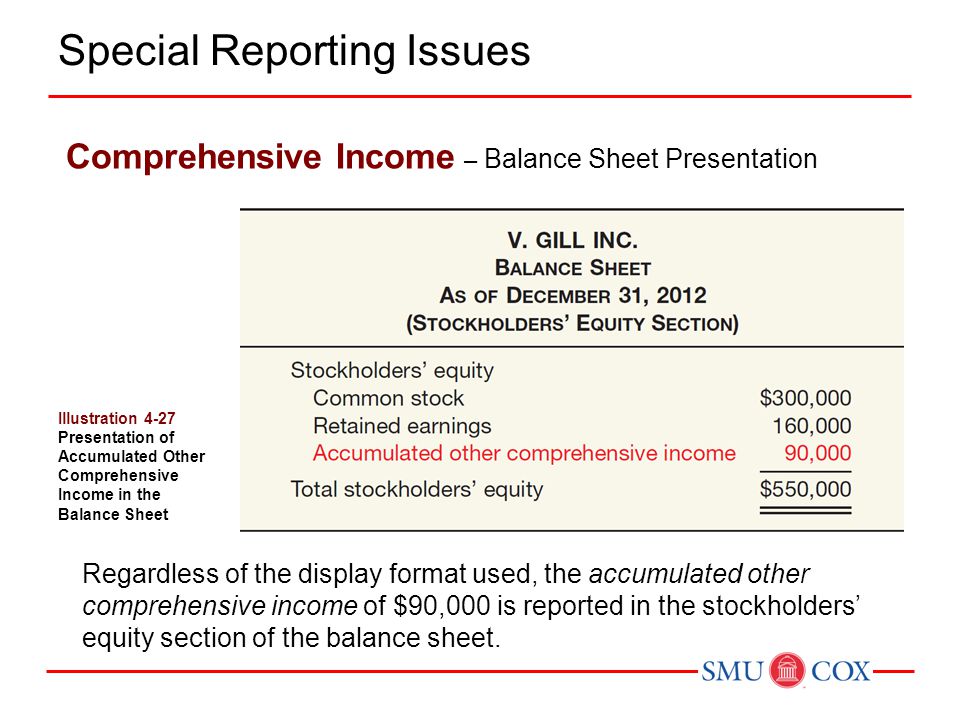

Comprehensive income is often listed on the financial statements to include all other revenues expenses gains and losses that affected stockholder s equity account during a period.

Why Isn T Comprehensive Income Comprehensible Strategic Finance

1 Income Statement

Statement Of Comprehensive Income Format Examples

14 Financial Statement Analysis Learning Objectives Ppt Download

Coming Soon To An Income Statement Near You Comprehensive Income Cfa Institute Market Integrity Insights

Treasury Stock And Accumulated Other Comprehensive Income Accountingcoach

How To Create A Statement Of Retained Earnings For A Financial Presentation

Chapter 28 Consolidated Statement Of Profit Or Loss And Other Comprehensive Income Ppt Video Online Download

Actg 6580 Chapters 4 And 5 Income Statement Statement Of Financial Position And Statement Of Cash Flows Ppt Video Online Download

Unusual Or Infrequently Occurring Items Course Hero

Ias 1 Presentation Of Financial Statements

Chapter 4 Continued Income Statement And Related Information Sommers Acct 3311 Chapter 1 Environment And Theoretical Structure Of Financial Accounting Ppt Download

Chapter 4 Income Statement Ppt Download