Fixed Income Yield To Worst

:max_bytes(150000):strip_icc()/dotdash_Final_Yield_to_Worst_YTW_Oct_2020-01-cabc0d0cf5b64ef0b4f72afb4888b3aa.jpg)

Yield To Worst Ytw Definition

Why Own Bonds When Yields Are So Low Charles Schwab In 2020 Corporate Bonds Investing Bond

Bond Yields Nominal And Current Yield Yield To Maturity Ytm With Formulas And Examples

Debt And Government Bond Yield Google Search Government Bonds Lendingtree Filing Taxes

Equity Yields Vs Corporate Bond Yields Corporate Bonds Equity Interest Rate Chart

Us Bond Investors Are Not Fighting The Fed Marketing Income Finance

The illegal practice of underwriters marking up the prices on bonds for the purpose of reducing the yield on the bond.

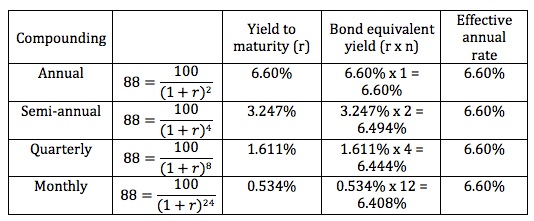

Fixed income yield to worst. Calculating yield for fixed income securities and. Calculating the yield for a portfolio. Yield and spread analysis for a specific general electric bond issue fixed income cheats fixed income corporates fixed income agencies credit default swaps previous. This practice referred to as burning the yield is done.

The spread to worst. Corp help last updated. 2 calculating yield to call ytc calculating ytc the same way we calculated ytm but by inputting n 2 since the bond is callable in two years ytc 4 93. Yield to call yield to worst fixed income coupon rate reference rate quoted.

Same as yield to call but when the bond holder has the option to sell the bond back to the issuer at a fixed price on specified date. Therefore the worst case scenario is that the company will call the bond in two years and you will realize a yield of 4 93 instead of 5 43. The following terms are explained. Understanding yield types and terms.

Yield to put ytp. Zero coupon or strip bonds and. Yield to worst ytw. Ytw helps investors manage risks and ensure that specific income.

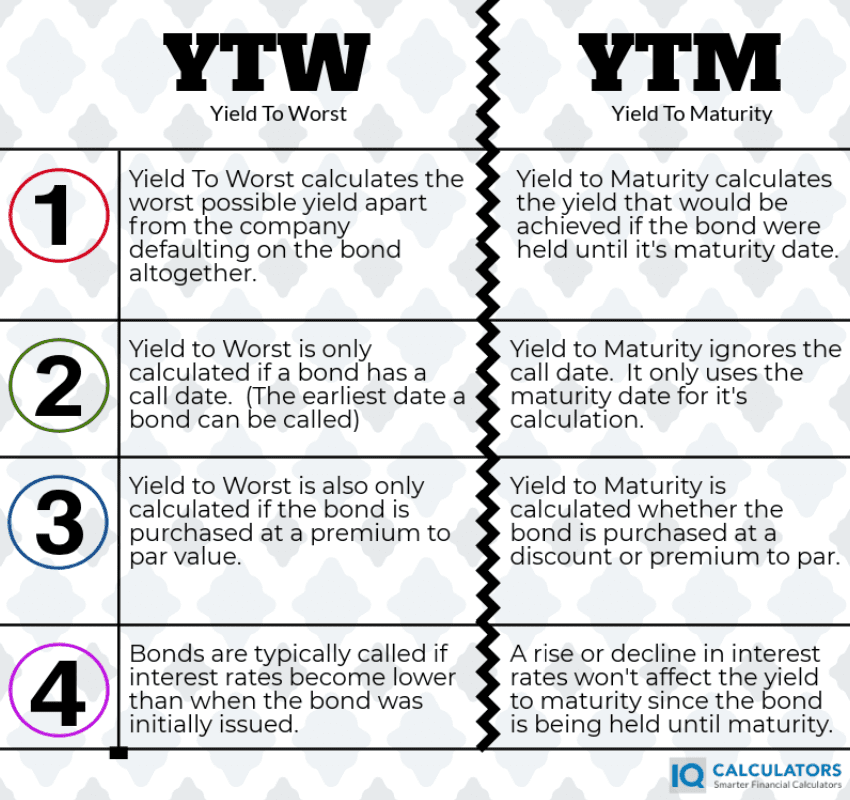

The yield to worst metric is used to evaluate the worst case scenario for yield at the earliest allowable retirement date. When a bond is callable puttable exchangeable or has other features the yield to worst is the lowest yield of yield to maturity yield to call yield to put and others. The difference in overall returns between two different classes of securities or returns from the same class but different representative securities.

Stocks Are A Screaming Buy Maybe Finance Stock Market Dividend

2020 Cfa Level I Exam Cfa Study Preparation

Bloomberg Business Bloomberg Business Bond Bloomberg

The Worst May Not Be Over For Chinese Corporate Bonds Corporate Bonds Bond Corporate

Yield To Worst What It Is And Why It S Important

High Yield Bond Issuers Remain On Sidelines Better Rated Leveraged Loans Eye Market Loan Bond Emergency

Vanguard Vanguard Experts Parse The Decline In Global Bond Yields

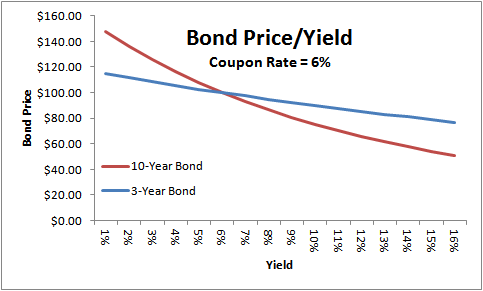

Bond Prices Rates And Yields Fidelity

Pin On Et S Top Stories

Infographic Why Markets Are Worried About The Yield Curve Yield Curve Curve Investment App

The Fed Makes Mortgage Bonds Trade Through Treasuries In Yield Mortgage Concentration Presidents

Bond Prices Rates And Yields

Low Bond Returns Are Nothing New A Wealth Of Common Sense In 2020 Bond Government Bonds Return

/Convexity22-0370dbde8e1c4a958bff8b670bf8bf5c.png)