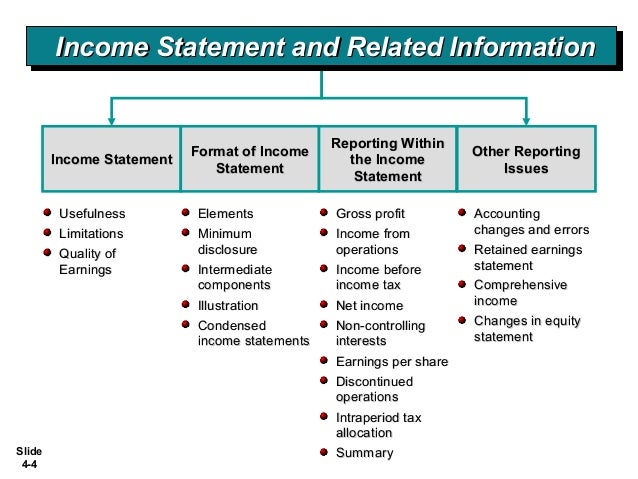

Statement Of Comprehensive Income Components

Statement Of Comprehensive Income Overview Components And Uses

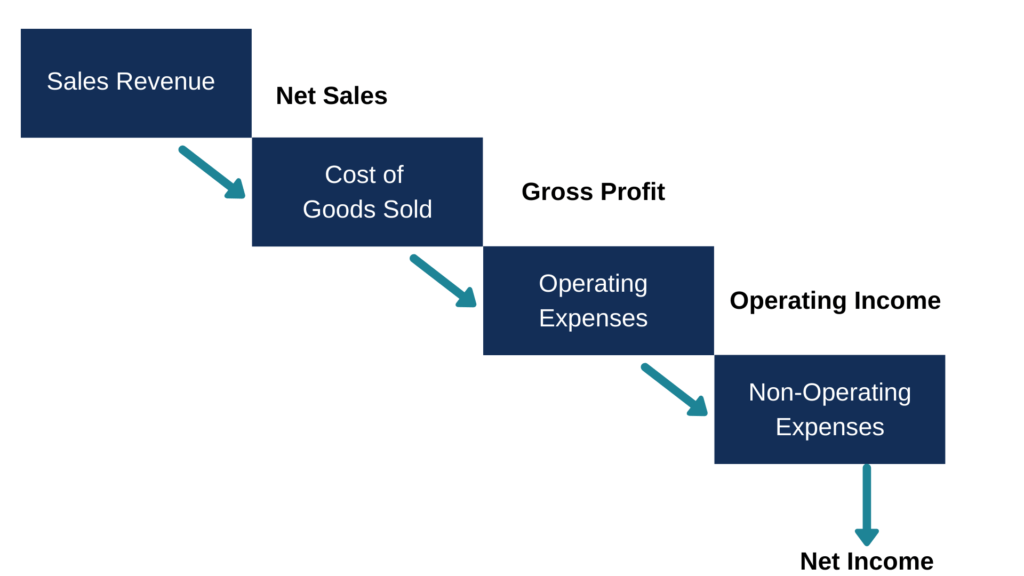

The Elements Of An Income Statement Dummies

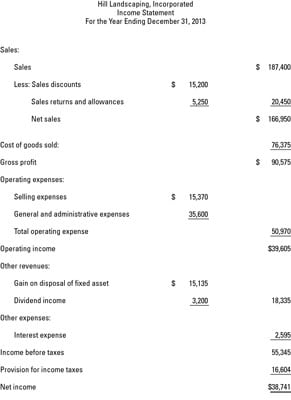

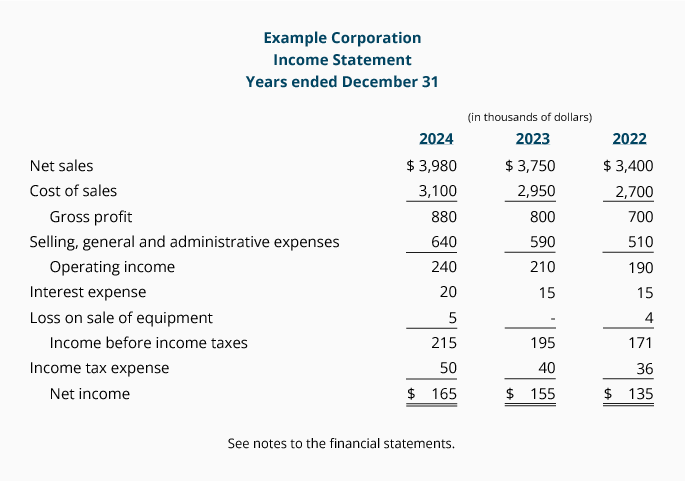

Multiple Step Income Statement Accountingcoach

Income Statement Introduction Business Tutor2u

1 Income Statement

Other Comprehensive Income Statement Meaning Example

Concept of comprehensive income 2.

Statement of comprehensive income components. It is also referred to as the top line because revenues are reported at the top of the income statement. Components of other comprehensive income that will not be reclassified to profit or loss net of tax. Other terms frequently used for revenue are sales net sales or sale revenue. But don t depend solely on it.

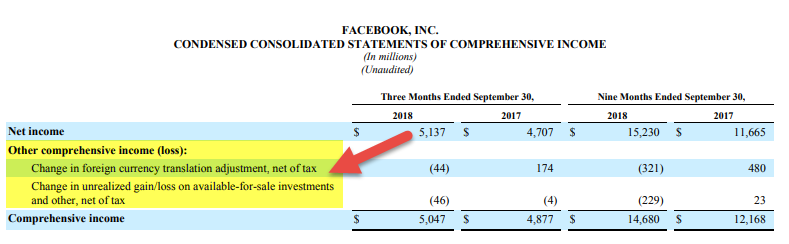

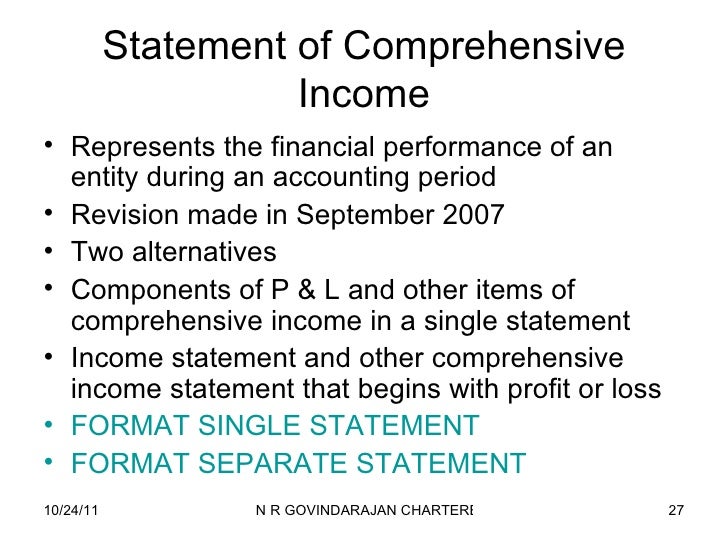

A statement of comprehensive income that begins with profit or loss bottom line of the income statement and displays the items of other comprehensive income for the reporting period ias 1 p 81. As per the gaap and ifrs standards these items are not included in the income statement and must be shown separately on the equity side of the balance sheet. Statement of comprehensive income oci components presented net of tax statement of comprehensive income year 2020. Components of comprehensive income 3.

Components of the income statement alternative presentation. Other comprehensive income oci includes all those revenues expenses gains and losses that affect a company s equity side of the balance sheet and have not yet been realized. Other comprehensive income net of tax gains losses from investments in equity. A statement of comprehensive income is the overall income statement that consolidates standard income statement which gives details about the repetitive operations of the company and other comprehensive income which gives details about the non operational transactions such as the sale of assets patents etc.

It is used to provide a summary of all the sources of revenue and expenses including payable taxes and interest charges interest expense interest expense arises out of a company that finances through debt or capital leases. One of the most important components of the statement of comprehensive income is the income statement. Comprehensive income also known as all inclusive concept of income is the change in equity net assets of an entity during a period from transactions and other events and circumstances from non owner sources. Identification of methods for presenting the components of other comprehensive income in the statement of changes in equity in the reporting practices of public companies in poland and.

Under both ifrs and us gaap the income statement may be presented as a separate statement followed by a statement of comprehensive income which begins with the profit or loss from the income statement or alternatively as a section of a single statement of comprehensive income. Income statement components revenue. Profit loss other comprehensive income.

Ifrs Vs Gaap Accounting Amt Training

:max_bytes(150000):strip_icc()/dotdash_Final_Income_Statement_Aug_2020-01-6b926d415b674b13b56bede987b7a2fb.jpg)

Income Statement Definition

How To Prepare An Income Statement A Simple 10 Step Business Guide

Reporting Unusual Items Income Statement Accountingcoach

Statement Of Comprehensive Income Format Examples

Best Accounting Flashcards Quizlet

Multi Step Income Statement Overview Components Pros

Income Statement Components Under Ias 1 Income Statement Personal Financial Statement Financial Statement

The Income Statement Boundless Business

Fundamentals Of Abm2 Statement Of Comprehensive Income Abm Specialize

Http File Heryan Web Id Pkn 20stan Bahan 20ajar 20kuliah D1 20pajak Semester 202 4 20pengantar 20akuntansi 20ii Kieso 203e Chapter 2014 20financial 20statement 20analysis 20 20financial 20accounting 20ifrs 203rd 20edition Pdf

Ias 1 Presentation Of Financial Statements

Multi Step Income Statement Format Examples How To Prepare